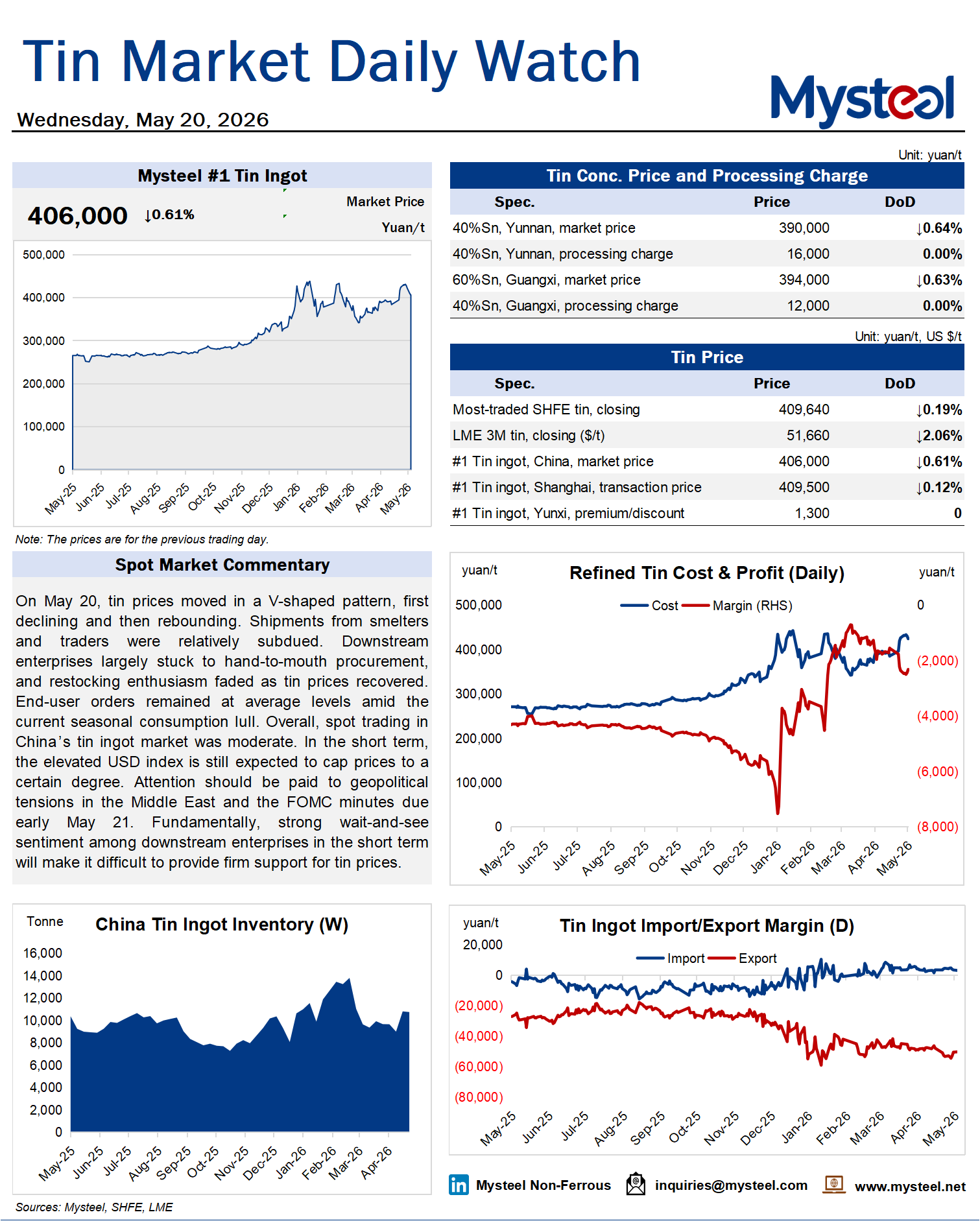

On May 20, tin prices moved in a V-shaped pattern, first declining and then rebounding. Shipments from smelters and traders were relatively subdued. Downstream enterprises largely stuck to hand-to-mouth procurement, and restocking enthusiasm faded as tin prices recovered. End-user orders remained at average levels amid the current seasonal consumption lull. Overall, spot trading in China's tin ingot market was moderate. In the short term, the elevated USD index is still expected to cap prices to a certain degree. Attention should be paid to geopolitical tensions in the Middle East and the FOMC minutes due early May 21. Fundamentally, strong wait-and-see sentiment among downstream enterprises in the short term will make it difficult to provide firm support for tin prices.