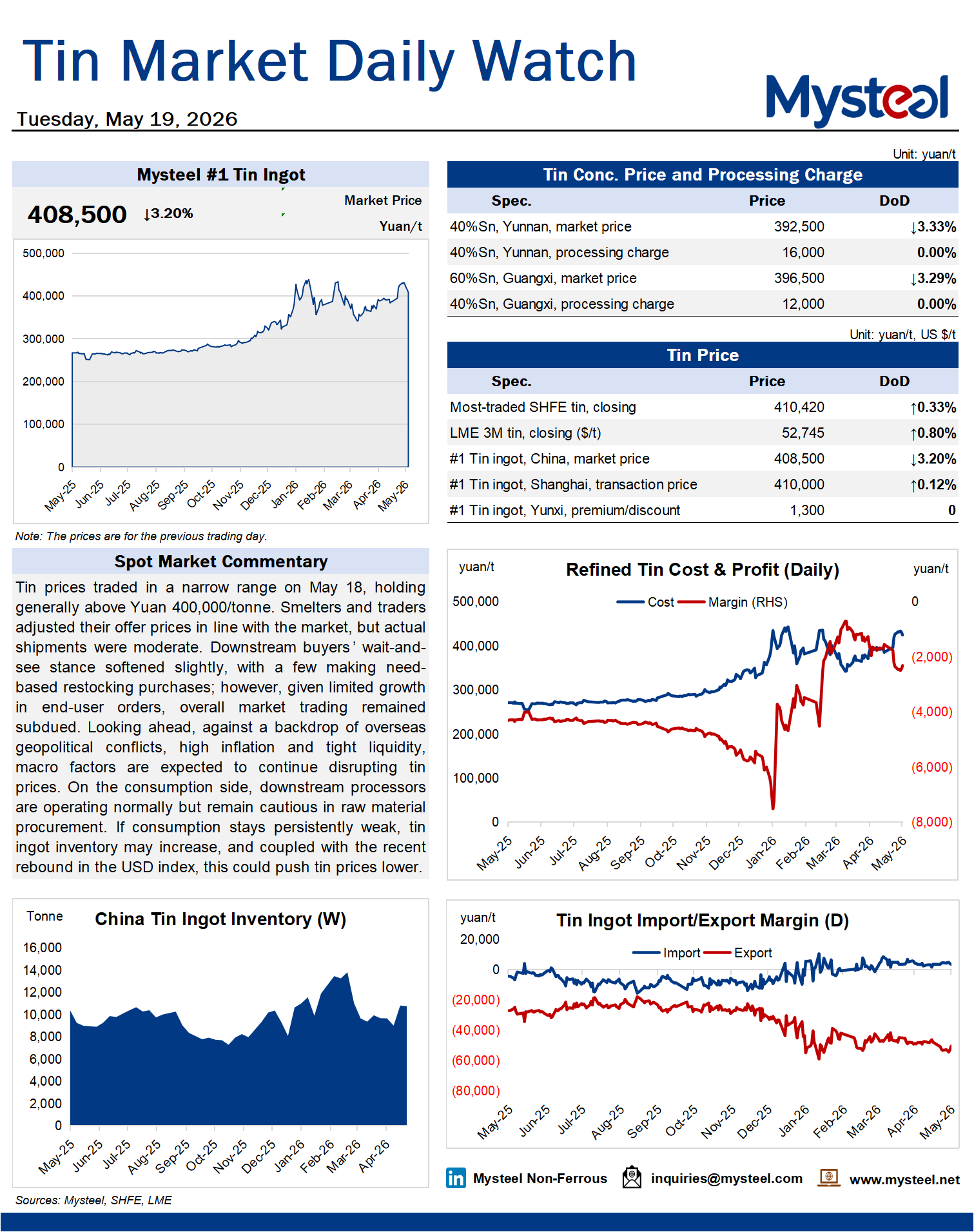

Tin prices traded in a narrow range on May 18, holding generally above Yuan 400,000/tonne. Smelters and traders adjusted their offer prices in line with the market, but actual shipments were moderate. Downstream buyers' wait-and-see stance softened slightly, with a few making need-based restocking purchases; however, given limited growth in end-user orders, overall market trading remained subdued. Looking ahead, against a backdrop of overseas geopolitical conflicts, high inflation and tight liquidity, macro factors are expected to continue disrupting tin prices. On the consumption side, downstream processors are operating normally but remain cautious in raw material procurement. If consumption stays persistently weak, tin ingot inventory may increase, and coupled with the recent rebound in the USD index, this could push tin prices lower.