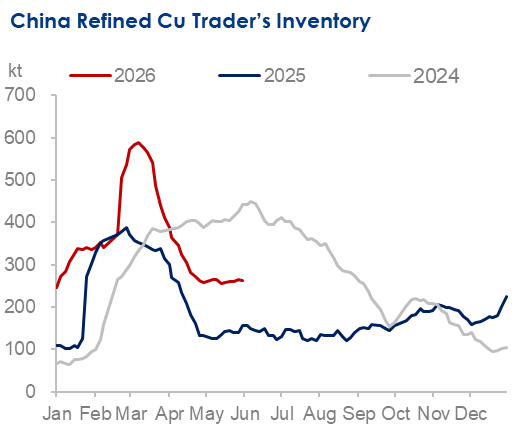

China's domestic copper inventories recorded continuous drawdowns in April and posted a modest buildup for most of May. Compared to the same period in previous years, overall inventory levels in 2026 remain at historically high levels. Yet, a mild inventory drawdown in expected in June 2026 amidst reductions in both supply and demand driven by a complexity of causes.

Firstly, domestic supply continues to tighten due to the tax authority's crackdown on the "invoice economy" and raw material shortages at the mining end. Secondly, imported copper arrivals are constrained by deteriorating arbitrage ratios and geopolitical risks. Furthermore, against the backdrop of persistently high absolute prices suppressing downstream consumption, a distinct pattern of weak supply and demand is evident in the market.

Source: Mysteel

Domestic Supply: Tax Disruptions and Raw Material Shortages Constrain Supply

At the beginning of 2026, the State Taxation Administration designated the "in-depth rectification of tax-related issues in illegal investment promotion and 'invoice economies'" as a key annual task. The so-called "invoice economy" primarily refers to enterprises engaging in circular invoicing or registering shell companies to inflate revenues and fraudulently obtain fiscal rebates without genuine business activities.

In the initial phase of this campaign, some local tax authorities adopted a "one-size-fits-all" approach, suspending or limiting invoicing capabilities and reducing credit limits for suspected enterprises without verifying the authenticity of their operations. This caused significant liquidity shocks to compliant non-ferrous metal trading enterprises. In response to concerns about collateral damage to compliant businesses, the State Taxation Administration issued corrective requirements in mid-May, stipulating that authorities cannot simply suspend invoicing or reduce quotas without actual investigation. Enterprises with legitimate trading backgrounds can apply to restore or increase their invoice quotas upon providing complete purchase/sales contracts, proof of title transfer, logistics records, and capital flow statements.

Against this background, some traders faced restrictions on invoice quotas and delays in quota issuance earlier, and some downstream enterprises also worried about obtaining sufficient input tax invoices in a timely manner. To mitigate tax compliance risks, downstream buyers chose to procure directly from smelters. Consequently, smelters had less incentive to sell to traders. Coupled with currently weak domestic spot premiums/discounts, this may stimulate some smelters to divert cargoes for export, making it difficult to increase the domestic spot availability.

Nevertheless, with the recent directive prohibiting of "one-size-fits-all" measures, some traders have gradually submitted materials to restore certain invoice quotas to meet normal business needs. Trading activity has improved compared to earlier periods, and the shortage of current-month invoices has alleviated somewhat.

Furthermore, according to Mysteel's research, nine domestic smelters are still scheduled for maintenance between June and July. Simultaneously, the full implementation of the "reverse invoicing" tax compliance policy has forced many non-compliant copper scrap recyclers out of the market, drastically reducing the supply of compliant, invoiced copper scrap. Coupled with the continuous decline in copper concentrate treatment charges (TC) and shortage of alternative feedstock like copper anode, domestic output is expected to further contract.

Import Replenishment: Unfavorable Arbitrage and Geopolitical Risks Suppress Arrivals

Poor domestic spot premiums performance has suppressed the traders' willingness to clear imports through customs. Reflecting this, Shanghai Bonded Zone inventories have recently shown signs of recovery. Meanwhile, as the COMEX-LME arbitrage spread has widened again, some traders continue to divert cargoes to the U.S. via re-exports.

Additionally, the volatility of U.S.-Iran negotiations has introduced uncertainty regarding shipping schedules for African cargoes. Compounded by the persistent tightness in sulfur supply, which continues to show no significant improvement, there are ongoing expectations of production curtailments at African local SX-EW smelters. Moreover, the imports are further constrained as fewer foreign trade long-term contracts have been signed for 2026, and some traders remain restricted by invoice quotas. Therefore, inbound inflows of imported copper are expected to have decreased in May.

High Copper Prices Limit Consumption Potential

China's domestic copper prices face near-term pressure due to weakening expectations for a Federal Reserve rate cut, or even expectations of a rate hike. However, overseas mine supply disruptions and expectations of smelter production cut support copper prices maintaining high-level fluctuations. Yet, June new orders from downstream enterprises have decreased at times. Entering the seasonal consumption off-season, the market is unlikely to see a significant increase in market demand.

Nevertheless, considering that leading enterprises still hold certain forward delivery orders, any significant price pullback could stimulate downstream enterprises' enthusiasm for bargain-hunting, which, however, will likely remain limited with copper prices remaining high overall.

In summary, although the crackdown on the "invoice economy" initially reduced market activity, the invoicing situation is expected to continue improving as more traders are expected to restore their quotas. Considering that many domestic smelters will still be undergoing maintenance and constrained by raw material shortages, domestic output is expected to decline further. Concurrently, imported copper arrivals are anticipated to decrease due to the widening COMEX-LME arbitrage spread. Thus, warehouse arrivals in the domestic market will remain low for most of June.

However, given that high copper prices significantly suppress market consumption, subsequent downstream procurement demand will remain sensitive to price movements. While a price drop may stimulate consumption, the potential for a continuous, substantial increase in outbound shipments is limited. Therefore, traders' inventories are expected to record a moderate destocking pace in June.

Written by Regina WANG, wangjiaqie@mysteel.com