On June 2, copper prices grew in futures and spot markets, supported by tight raw material supply, firm long-term demand expectations, and uncertain U.S. tariff policies.

Refined copper trading in China declined on June 2, as rising prices suppressed downstream procurement. Spot premiums also dropped in China's major markets, with holders actively lowering prices to facilitate sales.

Regrading copper scrap, growing copper prices widened the refined-scrap copper price spread and led to active spot trading. However, downstream processors using scrap as raw materials purchased on basic daily needs, avoiding building inventory and indicating sluggish end-user demand.

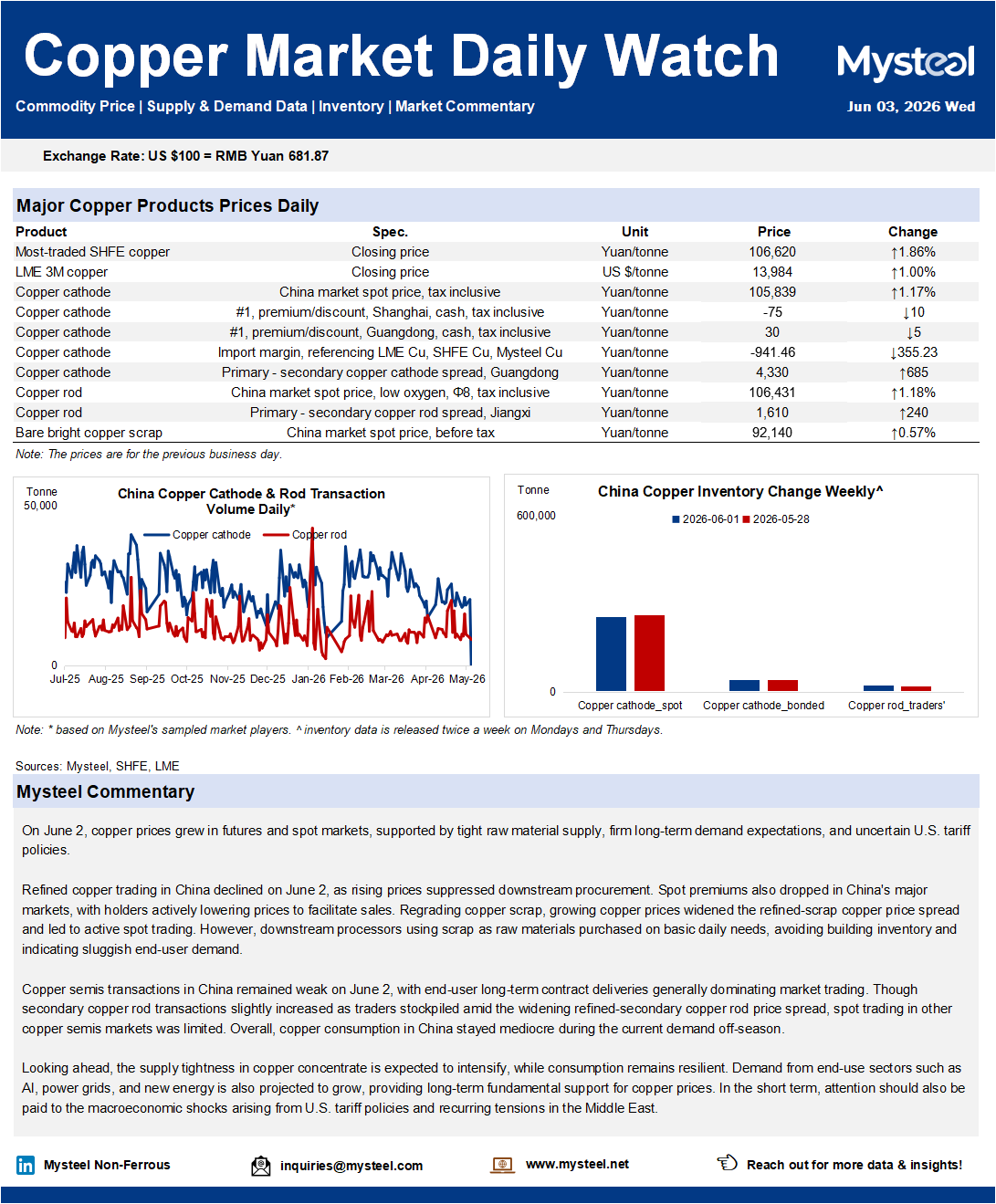

Copper semis transactions in China remained weak on June 2, with end-user long-term contract deliveries generally dominating market trading. Though secondary copper rod transactions slightly increased as traders stockpiled amid the widening refined-secondary copper rod price spread, spot trading in other copper semis markets was limited. Overall, copper consumption in China stayed mediocre during the current demand off-season.

Looking ahead, the supply tightness in copper concentrate is expected to intensify, while consumption remains resilient. Demand from end-use sectors such as AI, power grids, and new energy is also projected to grow, providing long-term fundamental support for copper prices. In the short term, attention should also be paid to the macroeconomic shocks arising from U.S. tariff policies and recurring tensions in the Middle East.