Global copper prices surged in the past year, with China's refined copper spot price rising by Yuan 28,316/tonne or 36.15% year on year, reaching Yuan 106,652/tonne on June 3, 2026, according to Mysteel. The rise in copper prices has been driven largely by copper stockpiling in the United States. According to Mysteel's estimates, this factor alone has increased copper prices by more than Yuan 10,000/tonne.

Copper prices are primarily driven by international markets, with LME and COMEX prices serving as global benchmarks. Although China is the world's largest copper consumer, it lacks significant pricing power, and domestic futures and spot prices largely track movements in international markets.

In February 2025, the U.S. launched a Section 232 investigation into copper, fueling expectations of potential import tariffs. As the U.S. is a net importer of refined copper, expectations of a substantial increase in domestic copper prices due to tariffs prompted market participants to stockpile refined copper. From August 1, 2025, the U.S. imposed a 50% tariff on semi-finished copper products. Although refined copper was temporarily exempted, the possibility of phased import tariffs of 15% in 2027 and 30% in 2028 remains. This prospect continues to encourage U.S. traders to build refined copper inventories.

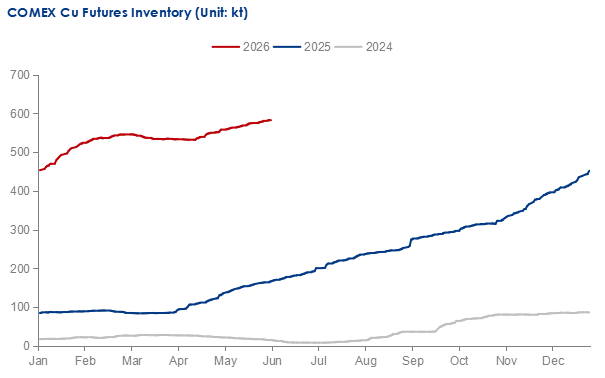

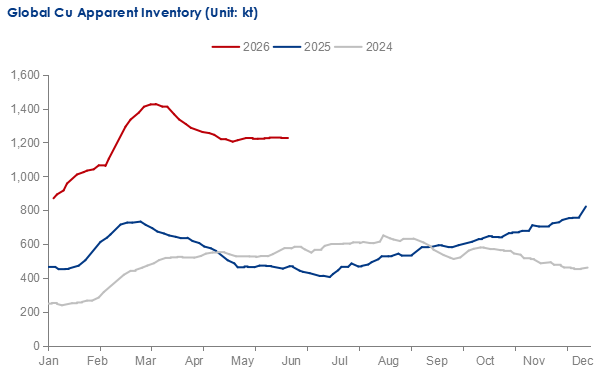

Over the past year, global apparent refined copper inventories, including China's spot inventories, LME inventories, and COMEX inventories, increased by approximately 600,000 tonnes, with COMEX inventories accounting for around 490,000 tonnes of the increase. After factoring in invisible inventories, it is estimated that the U.S. has stockpiled at least 600,000 tonnes of refined copper over the past year in anticipation of potential tariffs. Given the difficulty of accurately quantifying invisible inventories, this analysis evaluates the price impact under three U.S. stockpiling scenarios: 600,000 tonnes, 750,000 tonnes, and 900,000 tonnes, with 750,000 tonnes as the baseline scenario.

Data Source: COMEX

Data Source: COMEX, LME, Mysteel

Both copper supply and demand exhibit relatively low price elasticity, meaning that even a modest supply-demand imbalance requires a significant price adjustment to restore market equilibrium. On the supply side, copper mine production cannot respond quickly to price changes in the short term (one to two years). Based on Mysteel's assessment, a 10% increase in copper prices is estimated to boost annual global copper supply by only around 180,000 tonnes, mainly through copper scrap recovery.

On the demand side, the impact of higher copper prices differs between the short and long term. In the long term, demand is relatively more elastic, with a 10% increase in copper prices reducing annual global copper demand by approximately 840,000 tonnes, or about 3%. In the short term, demand is less responsive, with annual consumption estimated to decline by 280,000 tonnes or 1% in a low-elasticity scenario, to 560,000 tonnes or 2% in a high-elasticity scenario, according to Mysteel. This analysis adopts the midpoint estimate of 420,000 tonnes as the baseline scenario. Under this assumption, a 10% increase in copper prices would generate a combined supply-demand adjustment of approximately 600,000 tonnes, consisting of an increase in supply of 180,000 tonnes and a reduction in demand of 420,000 tonnes.

Over the past year, market participants have generally expected the U.S. to continue stockpiling copper, with little prospect of these inventories being released back into the market in the near term. As a result, U.S. stockpiling has effectively withdrawn a portion of refined copper supply from the global market, and provided significant support to copper prices. The estimated impact on copper prices under different stockpiling volumes and demand elasticity assumptions is shown in the table below:

| U.S. Copper Stockpiling's Boost to Prices | |||||||

| COMEX Inventory Build-up | 600 kt | 750kt | 900 kt | ||||

| Global Demand | Boost | Contribution | Boost | Contribution | Boost | Contribution | |

| High-elasticity scenario | 11,870 Yuan/t | 46% | 14,837 Yuan/t | 57% | 17,804 Yuan/t | 68% | |

| Baseline Senario | 9,100 Yuan/t | 35% | 11,375 Yuan/t | 44% | 13,650 Yuan/t | 53% | |

| Low-elasticity scenario | 7,378 Yuan/t | 28% | 9,223 Yuan/t | 35% | 11,068 Yuan/t | 43% | |

| Data Source: Mysteel | |||||||

Assuming U.S. copper stockpiling of 750,000 tonnes and a mid-range global copper demand elasticity, U.S. stockpiling is estimated to have increased China's copper prices by Yuan 11,375/tonne in the past year, indicating its significant impact on the market. The calculation is based on 750,000 tonnes of U.S. stockpiling divided by 600,000 tonnes of market adjustment capacity, comprising a 180,000-tonne increase in supply and a 420,000-tonne reduction in demand resulting from a 10% increase in copper prices, and multiplied by Yuan 9,100/tonne, equivalent to 10% of the average copper price between April 2025 and May 2026.

From an economic perspective, this implies that following the stockpiling of 750,000 tonnes of refined copper by the U.S., copper prices would need to rise by approximately Yuan 11,375/tonne to restore market equilibrium. At that price level, global copper demand would decline by 525,000 tonnes, while supply would increase by 225,000 tonnes, to offset the 750,000-tonne reduction in available market supply.

Comparing this estimated impact with the total increase in copper prices over the past year, U.S. copper stockpiling accounted for approximately 44% of the overall price gain under the baseline scenario. This indicates that U.S. stockpiling has been one of the key drivers of higher copper prices, with an impact comparable to the combined effects of copper mine supply disruptions, additional demand from the energy transition and artificial intelligence sectors, and monetary easing by the U.S. Federal Reserve.

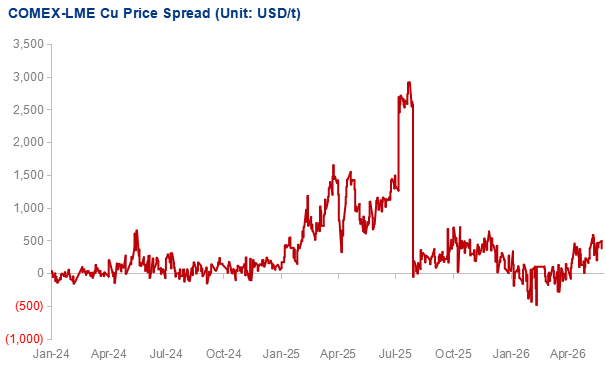

After May 2026, the COMEX-LME copper price spread widened, reaching $744/dmt on June 2. This reflected tightening copper supply driven by continued stockpiling and largely explains the recent upward shift in copper prices. Given the substantial support that U.S. copper stockpiling has provided to copper prices, the sustainability of this stockpiling trend is likely to be a key determinant of future copper price movements.

Data Source: COMEX, LME

By June 30, 2026, the U.S. Secretary of Commerce is required to submit an updated report on the domestic copper market to the President, including assessments of refining capacity and refined copper market conditions, to determine whether import tariffs on refined copper should be imposed from 2027 onward. If a decision is made not to impose tariffs, market participants should closely monitor whether any policy measures are introduced to retain the refined copper that has already been stockpiled. If tariffs are approved, attention will shift to whether the current pace of U.S. copper stockpiling can be sustained. Should the U.S. continue stockpiling copper through the end of the year, it would provide strong support for current elevated copper prices. Conversely, if the pace of stockpiling slows, stockpiling activity ceases, or existing inventories begin to be released back into the market, downside risks to copper prices would increase significantly.

Written by Mingyuan Wang, wangmingyuan@mysteel.com