On April 24, 2026, the State Taxation Administration of China officially released the Positive and Negative List for Taxpayer Compliance Invoicing, establishing 44 compliance benchmarks and warning indicators to guide taxpayers in compliant invoicing and curb long-standing issues such as the "invoice economy" and fraudulent invoicing for tax rebates. However, business models commonly used in the copper industry often resemble characteristics associated with non-compliant invoicing, resulting in some normally operating copper traders having their invoicing restricted, affecting normal business operations.

Unlike in many Western countries, invoices in China serve not only as commercial documents but also as a key tax administration tool. The special value-added tax (VAT) invoice is the sole legal basis for input tax deductions, making invoice compliance particularly important. However, a phenomenon called invoice economy has occurred in recent years, as some localities attracted shell companies by improperly offering tax-linked fiscal rebates, and some enterprises inflated their sales volumes to facilitate financing, through circular invoicing among related parties. Such acts undermine fair market competition and prompted regulators to strengthen oversight across the entire invoicing chain.

Commodity trade is inherently capital-intensive, involving large individual transaction amounts and frequent transfers of ownership. In the copper industry, multi-party transactions, intermediary trade finance, and warehouse receipt swaps often result in the separation of goods, funds, and invoice flows. Moreover, many compliant commodity traders operate under asset-light models where goods are shipped directly from suppliers to downstream buyers, which can easily be mistaken for fraudulent invoicing. Consequently, if oversight relies excessively on the consistency of flows of contracts, invoices, funds, and goods, while ignores genuine title transfers and commercial logic, legitimate copper commercial circulation can easily be misjudged as fraudulent invoicing. This can disrupt physical trading activities and hinder access to trade financing, negatively affecting supply chain efficiency.

According to Mysteel, Shanghai's copper market has seen increasingly evident impact of cracking down the invoice economy since late April. Most traders experienced varying degrees of invoice quota restrictions, and business activities of some firms not engaged in physical trade have largely been suspended. Some traders reduced short-term trading volumes to avoid compliance risk, hindering market activity. In addition, some downstream enterprises, concerned about traders' invoicing capability and efficiency, tend to procure directly from smelters, which also constrained refined copper spot transactions.

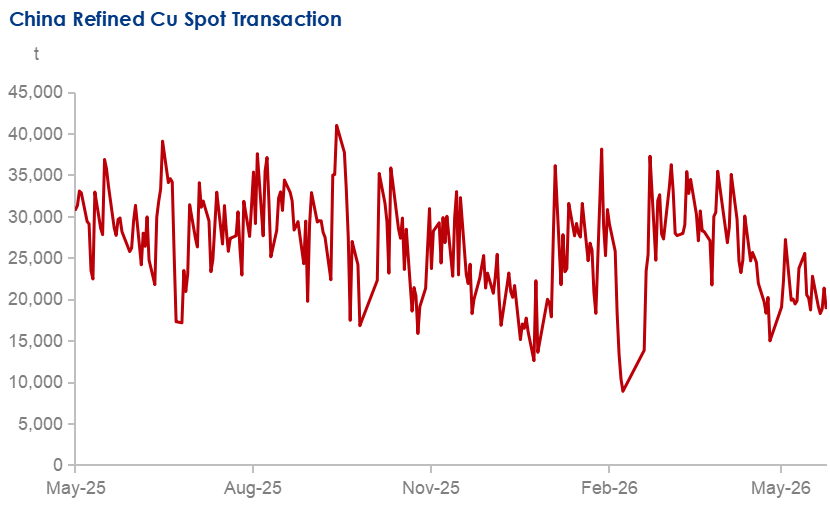

Mysteel's survey of 56 Chinese refined copper trading enterprises (including smelters, traders, and downstream processors) shows that their average daily refined copper transaction volume in May was 20,865 tonnes, down by 19.19% month on month from 25,821 tonnes in April and by 30.69% from May 2025. While higher copper prices remained the primary driver of weaker spot trading, tighter invoice management also contributed to the decline in market activity.

Data Source: Mysteel

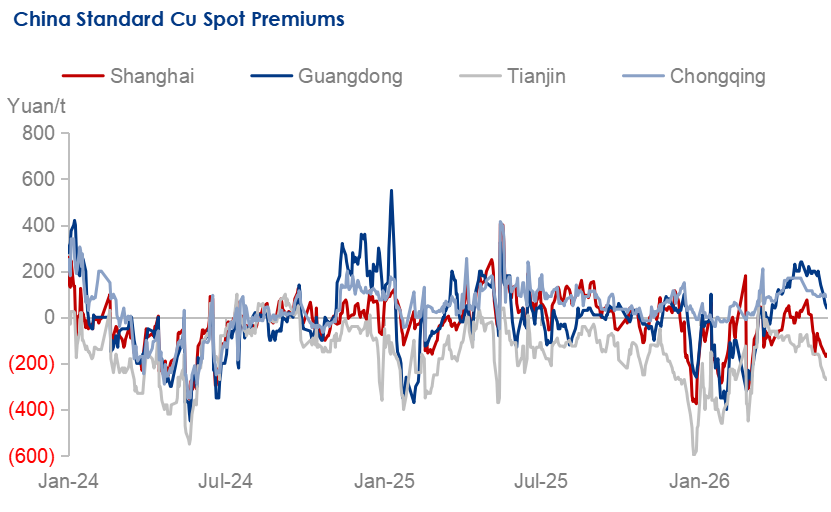

Overall, the most immediate impact of stricter invoice controls has been reduced spot market liquidity, which hampered trader's spot sales, exerting downward pressure on refined copper spot premiums. Mysteel's survey shows that the monthly average spot premium for standard refined copper (Cu>99.95%) in the Shanghai market was -Yuan 179/tonne in May, a decline of Yuan 80.12/tonne from the April average.

Data Source: Mysteel

Recognizing these unintended effects, the State Taxation Administration issued additional guidance on May 15 requiring local tax authorities to adopt differentiated management measures based on enterprises' operational characteristics and risk profile. Authorities were instructed not to suspend invoicing privileges, reduce invoice quotas, or impose restrictions without proper verification. Since then, some trading companies have gradually restored invoice quotas by submitting supporting documentation, easing invoicing constraints and supporting a recovery in refined copper spot market activity.

Looking ahead, invoice quotas are expected to gradually normalize as tax authorities refine verification procedures and improve their understanding of complex commodity trading models. Improved circulation of invoices and goods will boost trading activity in the refined copper market, thereby alleviating the downward pressure on spot premiums. However, refined copper premiums and spot consumption will continue to face pressure from elevated copper prices and seasonal demand weakness. As for absolute copper prices, global macro factors, raw material supply, and demand growth expectations will remain the main determinants. Invoicing regulation mainly affects the efficiency and costs of trading rather than underlying supply-demand fundamentals.

Beyond the campaign against the invoice economy, China's implementation of the reverse invoicing policy in the recycling sector also warrants attention. The policy shifts invoicing responsibilities from individual collectors and small-scale sellers, who often lack invoicing capabilities, to purchasing enterprises that can issue compliant invoices, thereby making the entire transaction chain legally accountable. In essence, reverse invoicing addresses structural weaknesses in the transaction chain, while the crackdown on the invoice economy targets existing compliance violations.

In practice, the reverse invoicing policy also faces challenges. Taking the copper scrap market as an example, collectors are often individuals who have long been accustomed to cash transactions without invoices. They worry about bearing tax costs and are reluctant to provide personal identity information, resulting in low willingness to cooperate with invoicing. Moreover, reverse invoicing has an annual quota limit of Yuan 5 million per individual. Given the high value of copper scrap transactions, this limit can be reached quickly, creating situations where physical supply exists but compliant invoicing capacity does not.

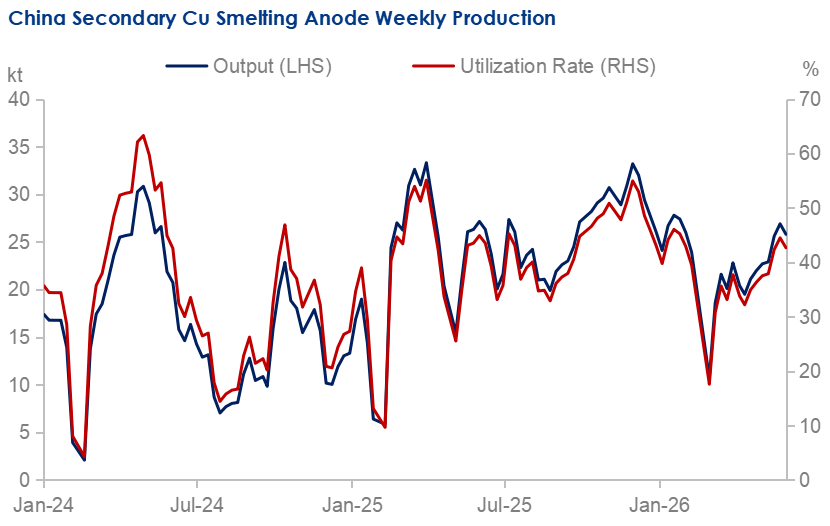

Due to obstacles to implementing reverse invoicing and the impact of tax inspections, downstream enterprises increasingly prefer to procure copper scrap with VAT invoices, leading to supply shortages and higher prices. Consequently, downstream producers of copper anodes using copper scrap face tighter raw material supply and lower production margins, with operating rates declining. According to Mysteel's survey on sample enterprises producing copper anodes from copper scrap (sample capacity coverage approximately 47.22%), the average operating rate of these sample enterprises as of June 1, 2026 was 37.74%, down by 3.37 percentage points from the 2025 average.

Data Source: Mysteel

The implications extend beyond the scrap market. According to Mysteel's research, due to shortages in copper concentrate supply, some Chinese refined copper smelters have increased the use of copper scrap as an alternative feedstock. Mysteel estimates that copper scrap accounted for approximately 26.9% of China's refined copper production feedstock in 2025. In the short term, policy uncertainty and invoice restrictions will remain key bottlenecks constraining China's copper scrap supply and anode output. Given the already tight copper concentrate supply, reduced copper anode production due to tax policy implementation issues could further tighten smelter feedstock availability and provide support to copper prices.

Overall, tighter invoice management has caused certain disruptions to China's copper market, specifically manifesting as hindered circulation of spot refined copper and a tightening of copper scrap supply. However, as the management measures continue to improve, such measures will drive China's copper industry chain toward greater transparency and healthier development in the long run.

Written by Zhaorui Cui, cuizhaorui@mysteel.com

Edited by Mingyuan Wang, wangmingyuan@mysteel.com