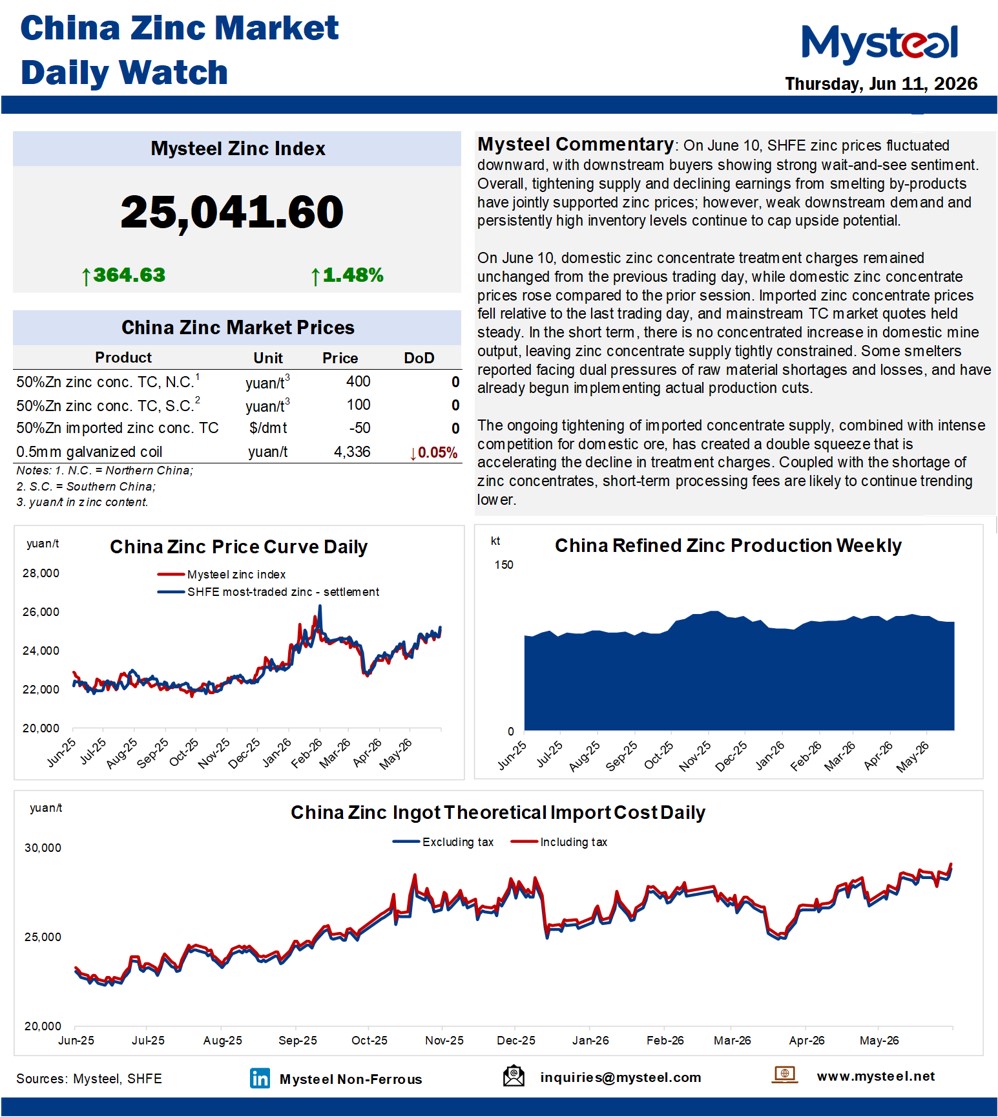

On June 10, SHFE zinc prices fluctuated downward, with downstream buyers showing strong wait-and-see sentiment. Overall, tightening supply and declining earnings from smelting by-products have jointly supported zinc prices; however, weak downstream demand and persistently high inventory levels continue to cap upside potential.

On June 10, domestic zinc concentrate treatment charges remained unchanged from the previous trading day, while domestic zinc concentrate prices rose compared to the prior session. Imported zinc concentrate prices fell relative to the last trading day, and mainstream TC market quotes held steady. In the short term, there is no concentrated increase in domestic mine output, leaving zinc concentrate supply tightly constrained. Some smelters reported facing dual pressures of raw material shortages and losses, and have already begun implementing actual production cuts.

The ongoing tightening of imported concentrate supply, combined with intense competition for domestic ore, has created a double squeeze that is accelerating the decline in treatment charges. Coupled with the shortage of zinc concentrates, short-term processing fees are likely to continue trending lower.