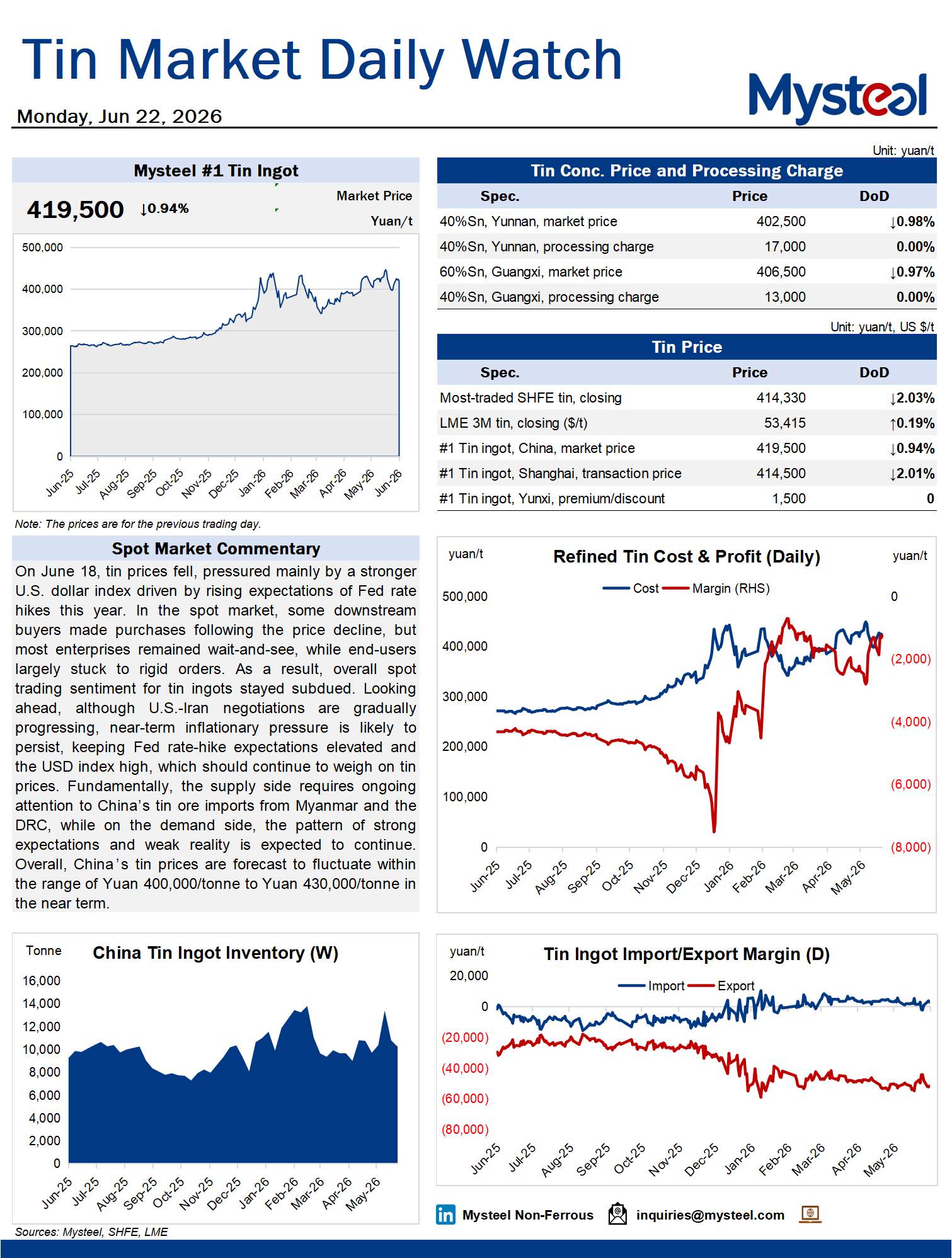

On June 18, tin prices fell, pressured mainly by a stronger U.S. dollar index driven by rising expectations of Fed rate hikes this year. In the spot market, some downstream buyers made purchases following the price decline, but most enterprises remained wait-and-see, while end-users largely stuck to rigid orders. As a result, overall spot trading sentiment for tin ingots stayed subdued. Looking ahead, although U.S.-Iran negotiations are gradually progressing, near-term inflationary pressure is likely to persist, keeping Fed rate-hike expectations elevated and the USD index high, which should continue to weigh on tin prices. Fundamentally, the supply side requires ongoing attention to China's tin ore imports from Myanmar and the DRC, while on the demand side, the pattern of strong expectations and weak reality is expected to continue. Overall, China's tin prices are forecast to fluctuate within the range of Yuan 400,000/tonne to Yuan 430,000/tonne in the near term.