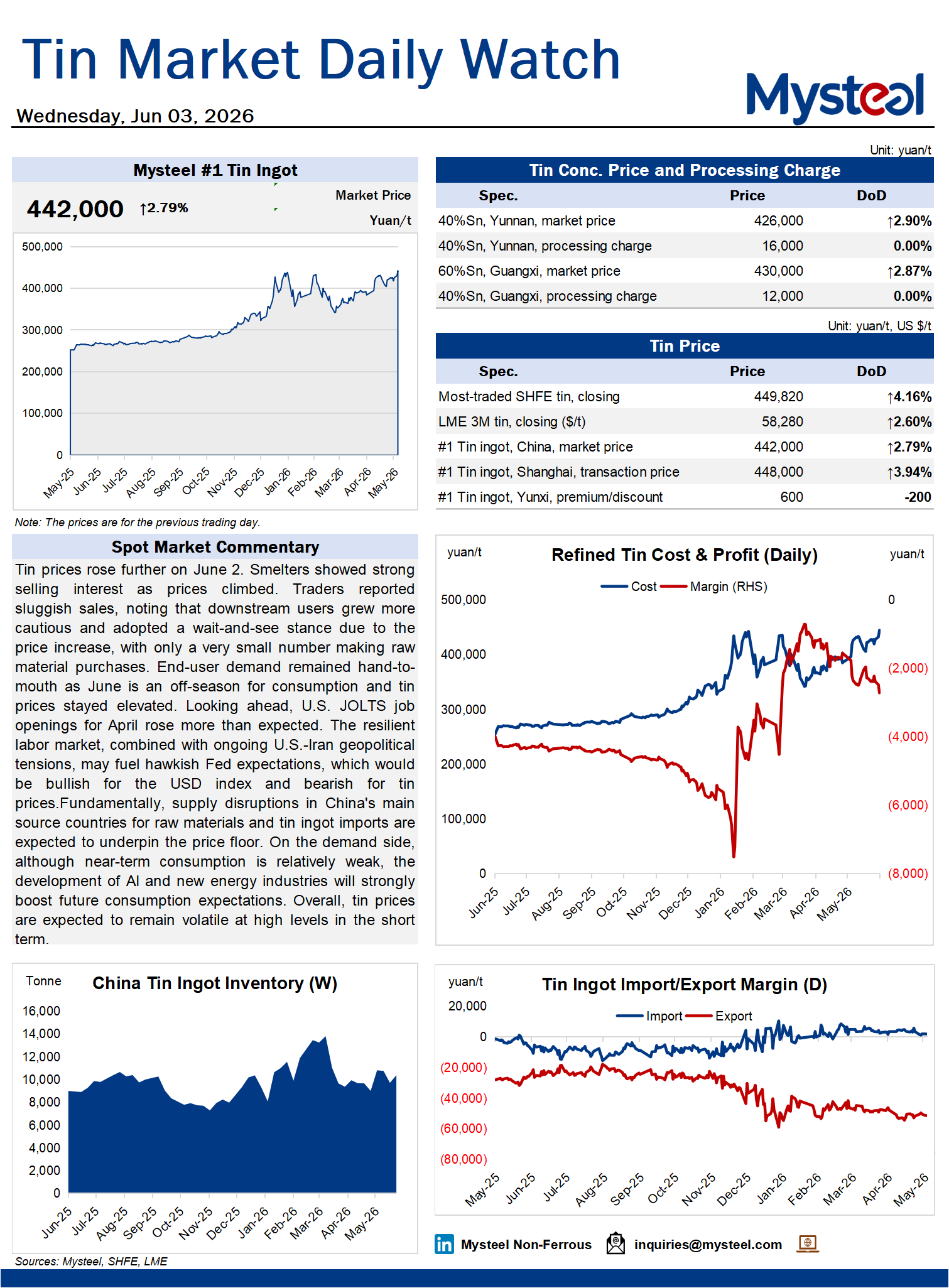

Tin prices rose further on June 2. Smelters showed strong selling interest as prices climbed. Traders reported sluggish sales, noting that downstream users grew more cautious and adopted a wait-and-see stance due to the price increase, with only a very small number making raw material purchases. End-user demand remained hand-to-mouth as June is an off-season for consumption and tin prices stayed elevated. Looking ahead, U.S. JOLTS job openings for April rose more than expected. The resilient labor market, combined with ongoing U.S.-Iran geopolitical tensions, may fuel hawkish Fed expectations, which would be bullish for the USD index and bearish for tin prices. Fundamentally, supply disruptions in China's main source countries for raw materials and tin ingot imports are expected to underpin the price floor. On the demand side, although near-term consumption is relatively weak, the development of AI and new energy industries will strongly boost future consumption expectations. Overall, tin prices are expected to remain volatile at high levels in the short term.