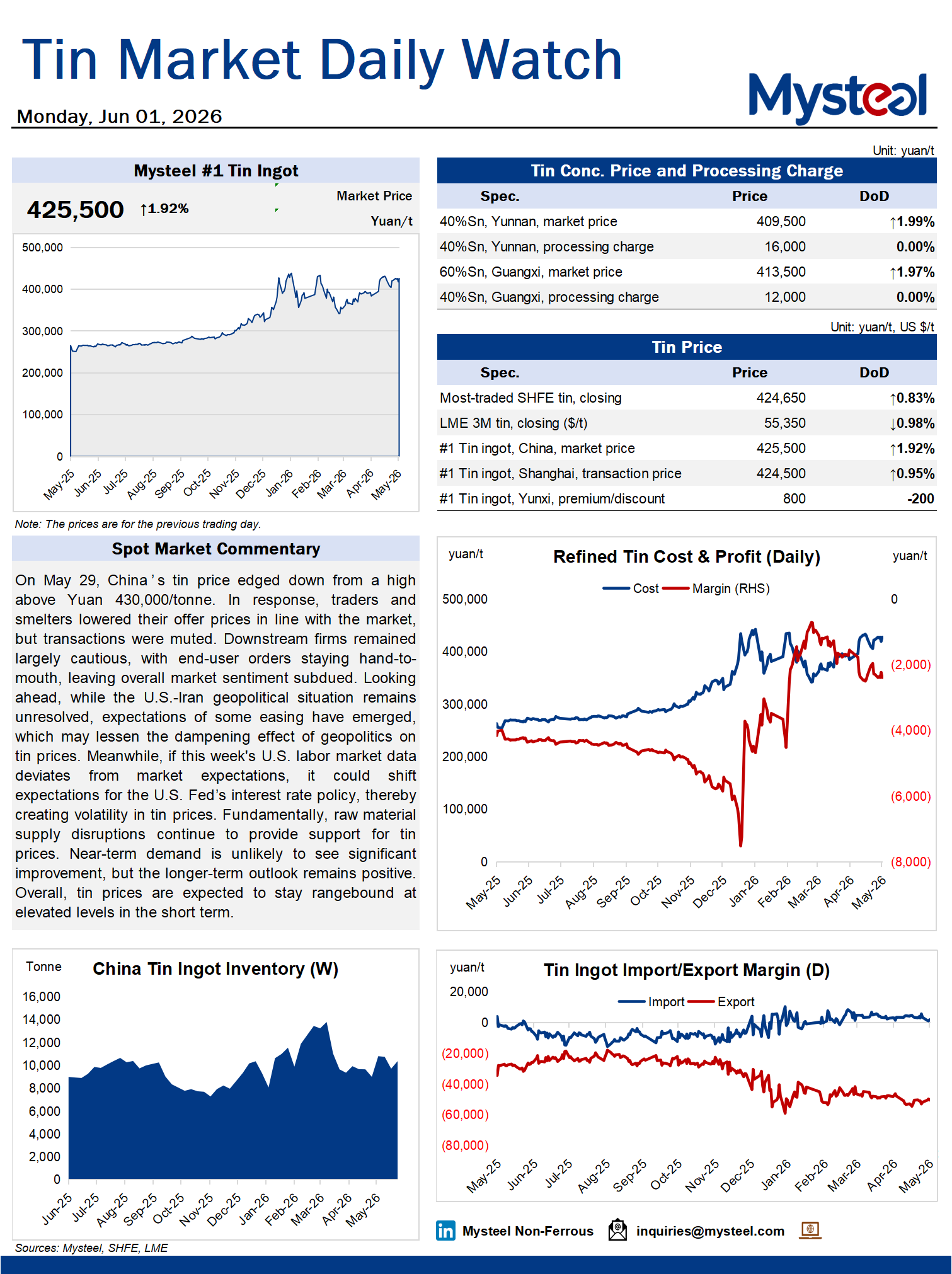

On May 29, China's tin price edged down from a high above Yuan 430,000/tonne. In response, traders and smelters lowered their offer prices in line with the market, but transactions were muted. Downstream firms remained largely cautious, with end-user orders staying hand-to-mouth, leaving overall market sentiment subdued. Looking ahead, while the U.S.-Iran geopolitical situation remains unresolved, expectations of some easing have emerged, which may lessen the dampening effect of geopolitics on tin prices. Meanwhile, if this week's U.S. labor market data deviates from market expectations, it could shift expectations for the U.S. Fed's interest rate policy, thereby creating volatility in tin prices. Fundamentally, raw material supply disruptions continue to provide support for tin prices. Near-term demand is unlikely to see significant improvement, but the longer-term outlook remains positive. Overall, tin prices are expected to stay rangebound at elevated levels in the short term.