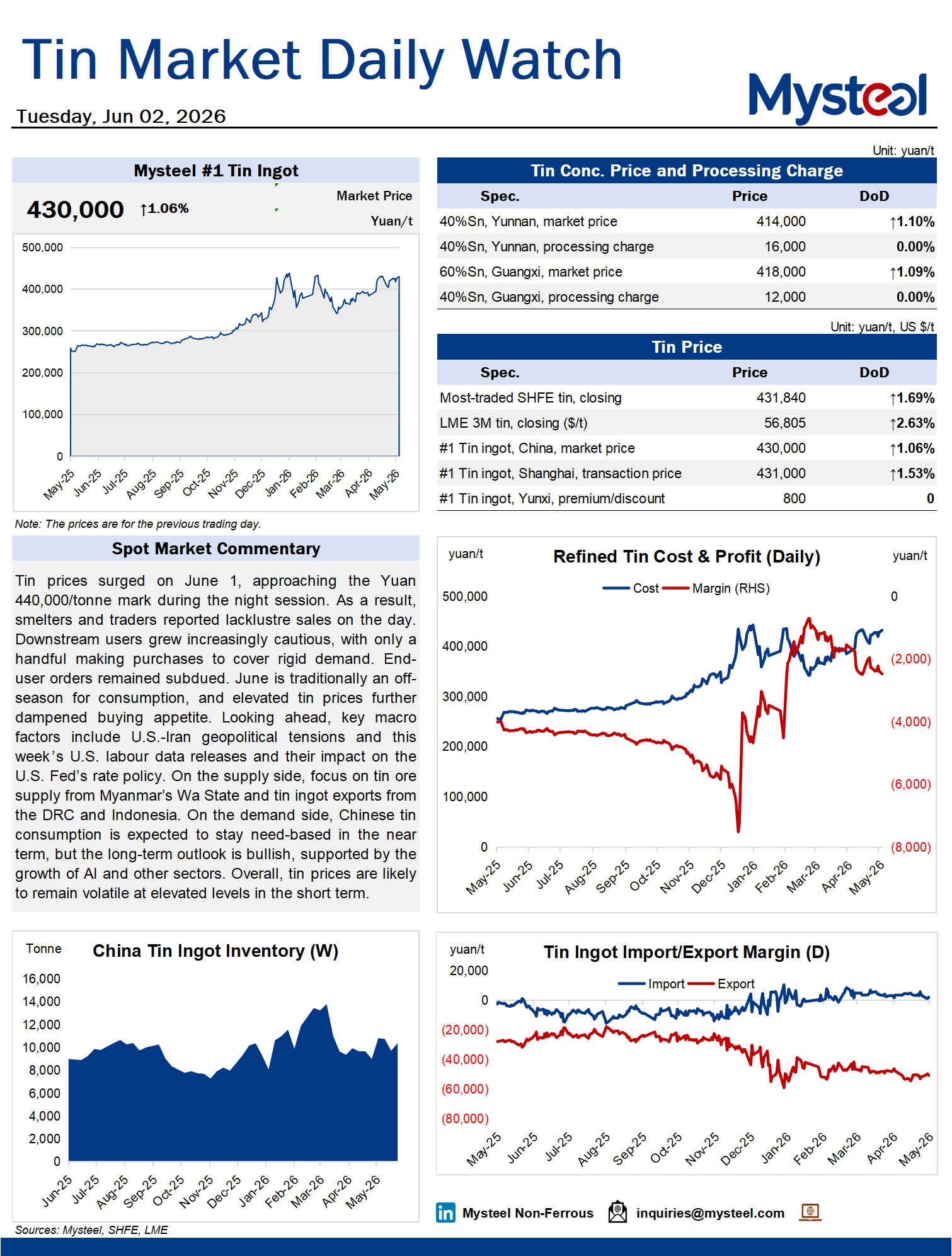

Tin prices surged on June 1, approaching the Yuan 440,000/tonne mark during the night session. As a result, smelters and traders reported lacklustre sales on the day. Downstream users grew increasingly cautious, with only a handful making purchases to cover rigid demand. End-user orders remained subdued. June is traditionally an off-season for consumption, and elevated tin prices further dampened buying appetite. Looking ahead, key macro factors include U.S.-Iran geopolitical tensions and this week's U.S. labour data releases and their impact on the U.S. Fed's rate policy. On the supply side, focus on tin ore supply from Myanmar's Wa State and tin ingot exports from the DRC and Indonesia. On the demand side, Chinese tin consumption is expected to stay need-based in the near term, but the long-term outlook is bullish, supported by the growth of AI and other sectors. Overall, tin prices are likely to remain volatile at elevated levels in the short term.