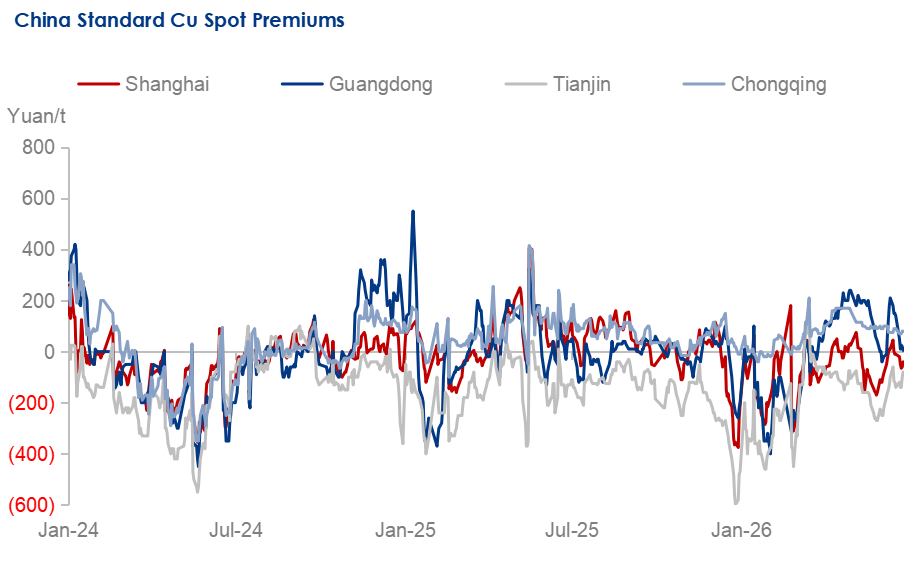

Premium: Refined copper spot premiums decline as holders offload

The average copper price fell week on week last week, with China's spot premiums also declining. In the spot market, arrivals of imported copper increased, but the overall supply improvement was limited due to limited shipments from smelters. Meanwhile, falling copper prices during the week spurred active restocking by downstream enterprises and lent support to spot premiums. However, as the half-year end approached, cash recovery needs among some holders triggered low-price selling to raise funds, weighing heavily on spot premiums. As a result, China's refined copper spot premiums dropped last week.

Looking ahead to this week, with the month-end approaching, some holders are expected to curtail sales, while copper prices are forecast to remain at recent low levels in the near term, leaving room for downstream purchases to increase further. In summary, given tighter supply and stronger demand, spot premiums are likely to stabilize with upside potential.

Data Source: Mysteel

Supply: China refined copper spot supply sees limited improvement

China's refined copper spot supply diverged across different markets last week. Although arrivals of imported copper increased in some markets thanks to earlier improvements in import ratios, and smelter shipments edged up slightly in Shanghai, Guangdong, and Chongqing after the Dragon Boat Festival holiday, overall spot supply remained relatively tight. In North China, a shortage of invoice quota at month-end also constrained spot supply. As a result, the improvement in China's refined copper spot supply was limited last week.

Looking ahead, the tightness in spot supply caused by smelter maintenance is expected to persist, and half-year end accounting settlements may lead companies to reduce shipments. Therefore, spot supply in China's refined copper market is expected to remain tight in the near term.

Demand: Copper price drop lifts spot market trading

China's refined copper spot trading volume rose week on week last week. Specifically, in Shanghai, downstream enterprises received more new orders after copper prices fell, which boosted their purchasing interest in refined copper. In Guangdong, although enterprises were under funding pressure at the half-year end, refined copper trading volume also rebounded week on week amid the continuous price decline. Meanwhile, in Tianjin and Chongqing, while downstream enterprises were slow to take delivery, there was a moderate pick-up in inquiries when prices dropped. Overall, refined copper spot trading in China improved last week.

Looking ahead, relatively low copper prices in the near term are expected to continue supporting downstream demand, making a sharp decline in China's spot refined copper trading unlikely.

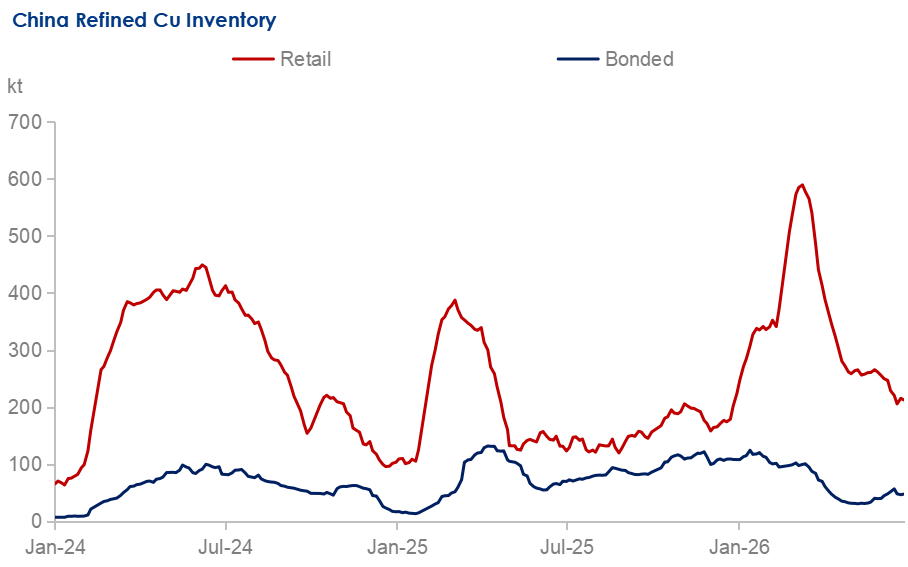

Inventory: China's refined copper retail and bonded inventories see limited change

China's refined copper retail inventory rose and then fell last week, with limited net movement. Specifically, retail inventory in Shanghai increased early in the week on higher arrivals of imported copper, but as copper prices declined, downstream purchasing demand picked up, and inventory subsequently edged down on stronger outflows. In contrast, retail inventory in Guangdong rose steadily throughout the week, primarily due to a modest increase in deliveries from smelters after the Dragon Boat Festival. However, as copper prices fell and downstream purchases strengthened, the pace of inventory growth Guangdong slowed. Overall, China's spot refined copper inventories posted a slight increase last week. Going forward, imported copper arrivals are still expected to rise, yet downstream procurement demand is likely to remain firm. As a result, China's refined copper retail inventory is expected to see only limited changes in the near term.

China's refined copper bonded inventory declined slightly week on week last week. Although domestic smelters' cargoes intended for export continued to flow into bonded zones, exports and customs clearance drew down overall inventory. Looking ahead, with the sustained improvement in import ratio, some bonded inventory is expected to be cleared and imported into China's domestic market. As a result, although smelter exports are still likely to arrive at the bonded zone, inflows are projected to be limited, and China's overall refined copper bonded inventory is expected to keep falling.

The weekly average spread between the main COMEX and LME copper contracts was down by $362.20/tonne week on week to $289.36/tonne last week. The average LME cash-3M copper contract settlement spread was -$50.7/tonne last week, up by $15.6/tonne week on week. As COMEX copper traded still at a premium and above $200/tonne, COMEX copper inventory remained increasing last week and LME copper inventory fell further. Looking ahead, as market expectations for the implementation of U.S. tariff policy draw closer, the COMEX copper premium is expected to persist in the near term, keeping its inventory on a modest upward trend. Meanwhile, LME inventory is forecast to continue decreasing.

Data Source: Mysteel

More regular analysis and comprehensive data on China's copper industry are available in Mysteel Copper Weekly, Mysteel Copper Monthly, and Mysteel Copper Database. Reach out to us via Mysteel's official website: Latest & Reliable Copper Market Price in China | Mysteel, and follow Mysteel Non-Ferrous for more insights!

Written by Zhaorui Cui, cuizhaorui@mysteel.com

Edited by Mingyuan Wang, wangmingyuan@mysteel.com