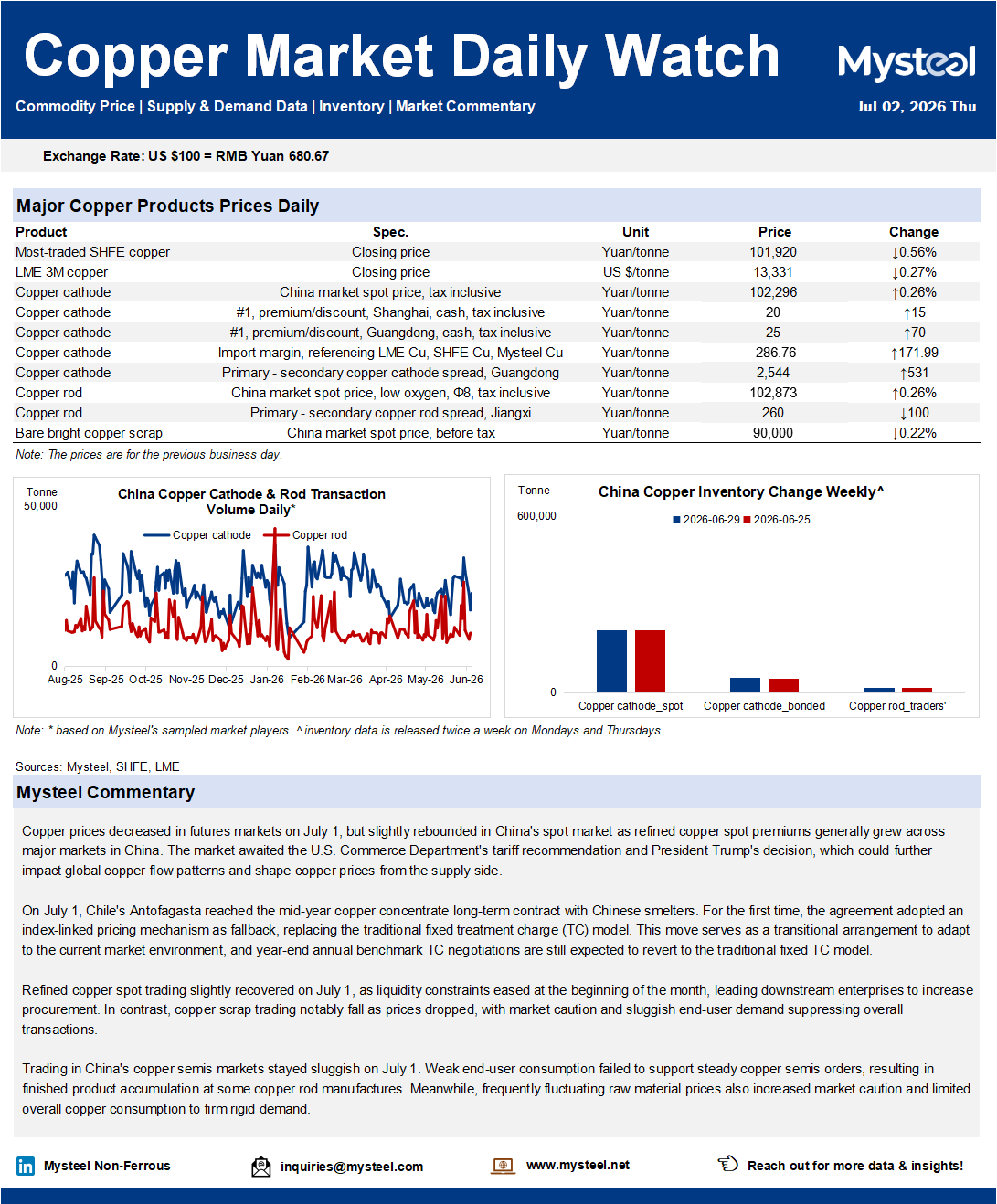

Copper prices decreased in futures markets on July 1, but slightly rebounded in China's spot market as refined copper spot premiums generally grew across major markets in China. The market awaited the U.S. Commerce Department's tariff recommendation and President Trump's decision, which could further impact global copper flow patterns and shape copper prices from the supply side.

On July 1, Chile's Antofagasta reached the mid-year 2026 copper concentrate long-term contract with Chinese smelters. For the first time, the agreement adopted an index-linked pricing mechanism as fallback, replacing the traditional fixed treatment charge (TC) model. This move serves as a transitional arrangement to adapt to the current market environment, and year-end annual benchmark TC negotiations are still expected to revert to the traditional fixed TC model.

Refined copper spot trading slightly recovered on July 1, as liquidity constraints eased at the beginning of the month, leading downstream enterprises to increase procurement. In contrast, copper scrap trading notably fall as prices dropped, with market caution and sluggish end-user demand suppressing overall transactions.

Trading in China's copper semis markets stayed sluggish on July 1. Weak end-user consumption failed to support steady copper semis orders, resulting in finished product accumulation at some copper rod manufactures. Meanwhile, frequently fluctuating raw material prices also increased market caution and limited overall copper consumption to firm rigid demand.