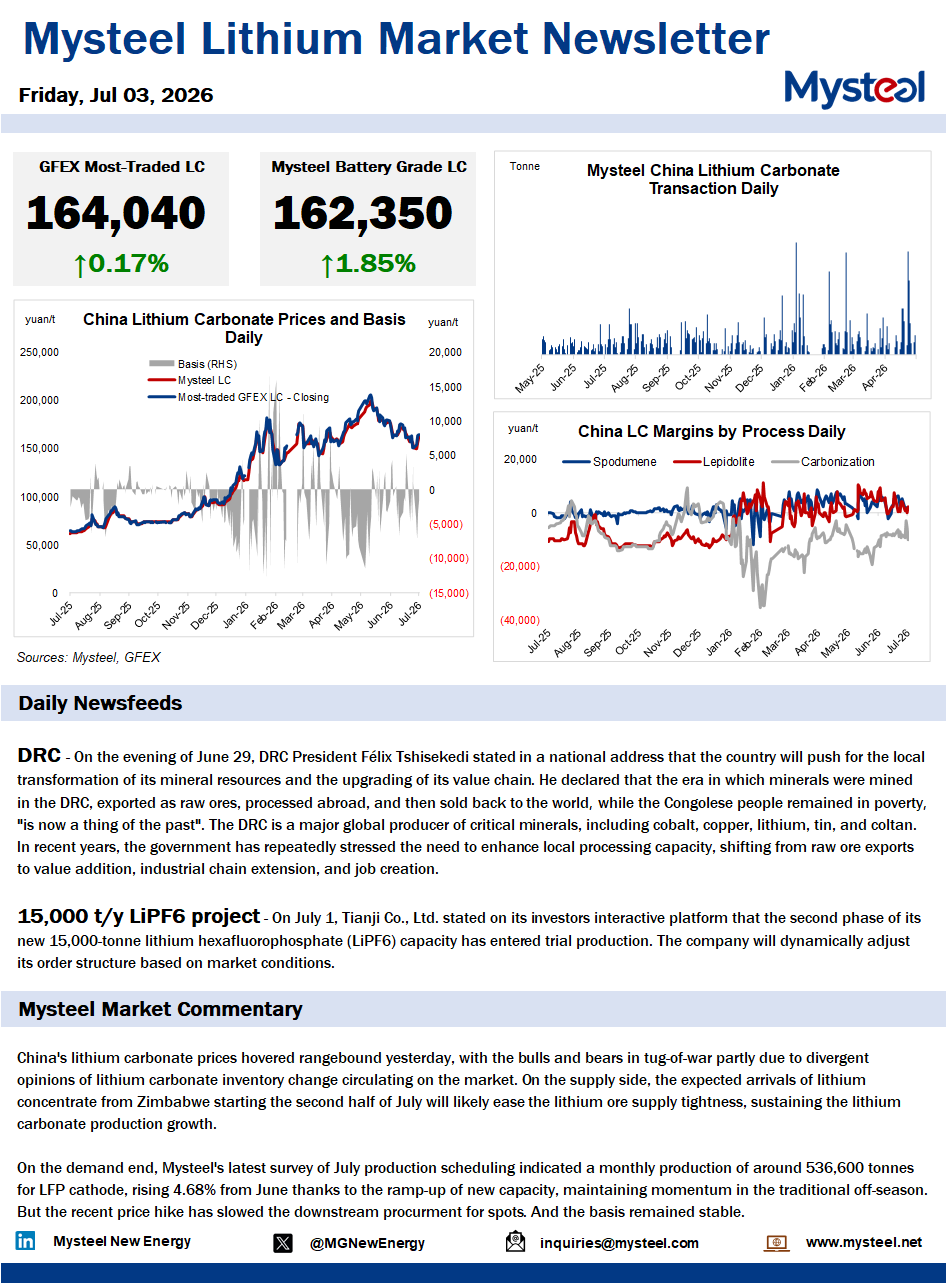

China's lithium carbonate prices hovered rangebound yesterday, with the bulls and bears in tug-of-war partly due to divergent opinions of lithium carbonate inventory change circulating on the market. On the supply side, the expected arrivals of lithium concentrate from Zimbabwe starting the second half of July will likely ease the lithium ore supply tightness, sustaining the lithium carbonate production growth.

On the demand end, Mysteel's latest survey of July production scheduling indicated a monthly production of around 536,600 tonnes for LFP cathode, rising 4.68% from June thanks to the ramp-up of new capacity, maintaining momentum in the traditional off-season. But the recent price hike has slowed the downstream procurment for spots. And the basis remained stable.