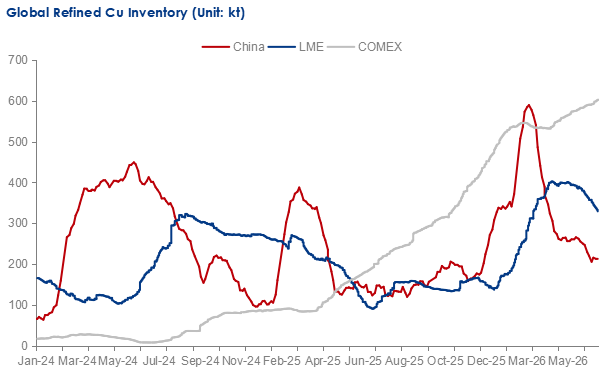

Global refined copper prices hovered around record highs throughout the first half (H1) of 2026, despite visible inventory remaining at historically elevated levels. By the end of June, combined visible inventory across China, the London Metal Exchange (LME) and the COMEX stood at around 1.2 million tonnes. More than half of refined copper, however, were concentrated in the U.S. market. The divergence reflected a large-scale redistribution of copper driven primarily by persistent U.S. tariff expectations, and was a key driver behind the price surge.

Inventory movements diverged sharply across the world's three major trading regions in H1 2026. China's inventory followed a typical seasonal cycle, surging after the Chinese New Year holiday (February 15-23) and falling sharply afterwards. LME inventory accumulated before tightening rapidly, while COMEX inventory maintained overall growth.

Source: COMEX, LME, Mysteel

Seasonal inventory decline in China worsened by tightening supply

China's combined refined copper retail and bonded inventory increased steadily during the first two months of 2026, before peaking at 689,100 tonnes in early March, the highest level recorded in the past decade. Inventory then declined sharply during March and April, fluctuated modestly in May, and fell further to 262,700 tonnes by the end of June.

Inventory accumulation during January and February was largely seasonal. Around the Chinese New Year holiday, most copper smelters maintained normal operating rates, while downstream fabricators and manufacturers suspended production. Logistics disruptions during the holiday further slowed deliveries, causing inventory to accumulate rapidly after the holiday period. As downstream manufacturers gradually resumed production and actively replenished raw materials throughout March and April, refined copper inventory fell notably. Entering the second quarter, China's traditional smelter maintenance season began. Maintenance outages reduced refined copper production and limited warehouse deliveries, accelerating inventory declines. However, record-high copper prices increasingly restrained downstream purchasing, causing inventory declines to slow during May and June despite reduced supply.

Source: Mysteel

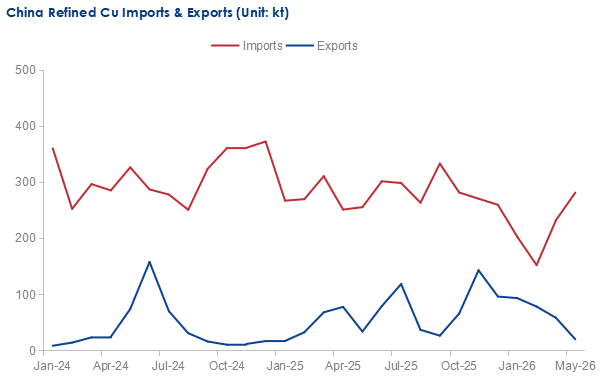

China's trade flows reinforced this inventory cycle. Refined copper imports weakened during the first two months of the year as record-high LME prices eroded import arbitrage, while ample domestic inventory also reduced import demand ahead of the Chinese New Year holiday. As downstream consumption improved and the import window intermittently reopened from March, imports gradually recovered. Exports remained relatively elevated despite trending lower throughout the first half of 2026, due to export arbitrage and the resulting smelters' increased export plans, also contributing to tightening inventory.

Source: GACC, Mysteel

LME inventory drained under U.S. tariff expectations

LME inventory initially rose in early 2026, as copper shipments were disrupted by shifting trade expectations. Following the first proposal for U.S. copper tariffs in early 2025, traders increasingly redirected copper toward the U.S. before any tariffs took effect. However, when refined copper was ultimately excluded from the proposed 50% tariff measures announced in August 2025, part of the metal originally intended for the U.S. was temporarily redirected to, or remained within, LME warehouses. Weak Chinese imports and relatively strong exports further reinforced the build.

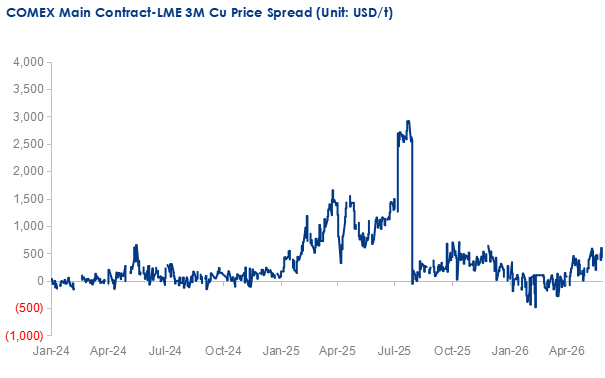

A major turning point came after the White House's tariff policy update on April 2, 2026. Although refined copper was still not directly subject to additional tariffs, the announcement reinforced market expectations that copper-related trade measures remained under consideration. The resulting widening COMEX-LME price spread created strong incentives to ship copper into the U.S., triggering sustained LME inventory withdrawals that continued through the second quarter.

Source: COMEX, LME

In addition, supply-side constraints reinforced the LME inventory decline. Tighter sulphur supplies linked to geopolitical tensions in the Middle East, together with China's sulfuric acid export restrictions implemented in May, constrained SX-EW copper production in Chile and Africa by tightening raw material sulfuric acid supply, further reducing available supply outside the U.S. market.

COMEX's copper stockpile continues to expand

COMEX inventory experienced short-term fluctuations but maintained a clear upward trend throughout the first half of 2026, extending the accumulation that began after U.S. tariff expectations emerged in 2025. Including off-exchange inventory, the U.S. is estimated to have accumulated at least 600,000 tonnes of refined copper over the past year in anticipation of potential import tariffs, based on Mysteel's assessment.

According to J.P. Morgan, the U.S. accounts for only around 6% of global refined copper consumption, yet over the past eighteen months it has imported copper at a pace consistent with a market representing roughly 9% of global demand. This unusually strong import intensity reflects precautionary stockpiling rather than underlying consumption growth. Meanwhile, elevated copper prices also discouraged immediate downstream consumption in the U.S., allowing imported copper to accumulate in warehouses rather than being absorbed by end users.

Structural inventory imbalance outweighs fundamental surplus

In April, the International Copper Study Group (ICSG) revised its market outlook, forecasting a 96,000-tonne refined copper surplus in 2026, reversing its earlier projection of a 150,000-tonne deficit. The organization also expects the surplus to widen further to 377,000 tonnes in 2027, reflecting slower demand growth and increasing refined output from recycled copper.

Nevertheless, copper prices continued to reach successive record highs throughout H1 2026. Although the global refined copper balance has shifted into surplus, inventory has become increasingly concentrated in the U.S. while availability elsewhere has tightened. This unprecedented geographical inventory imbalance has emerged as one of the key drivers supporting copper prices, alongside mine supply disruptions, structural demand growth from the energy transition and AI-related infrastructure investment, as well as supportive macroeconomic conditions.

Looking ahead, the direction of global copper prices in the second half of 2026 will depend less on the absolute volume of inventory than on where inventory remain, and how much is available. If U.S. stockpiling continues, whether driven by tariffs or policies aimed at retaining accumulated copper, the current regional tightness is likely to persist, keeping prices supported. Conversely, any slowdown in inventory accumulation or a release of U.S. stockpiles back into the global market could ease non-U.S. market tightness and expose copper prices to downside pressure.

Written by Mingyuan Wang, wangmingyuan@mysteel.com