Q2 2026 closed with the aluminum extrusion sector trapped in a classic supply-demand crunch. Capacity utilization plunged to a cyclical low of 37.05%, while equipment start-up rates stagnated at 55%-57%, exposing producers' proactive output cuts to avoid risk. Order backlogs shrank, compressing lead times from a peak of 10–15 days to just 8–10 days, as downstream buyers engaged in tentative inquiries amid aggressive price negotiations and a wait-and-see stance. The supply chain underwent passive destocking, and falling inventories reflected production cuts for loss mitigation, not demand recovery, while clogged aluminum scrap circulation forced a full pivot to primary aluminum ingot substitution. With weak domestic demand compounded by blocked export channels, a negative feedback loop is firmly in place.

Production side: diverging trends in start-ups and capacity utilization, overall operation remains weak

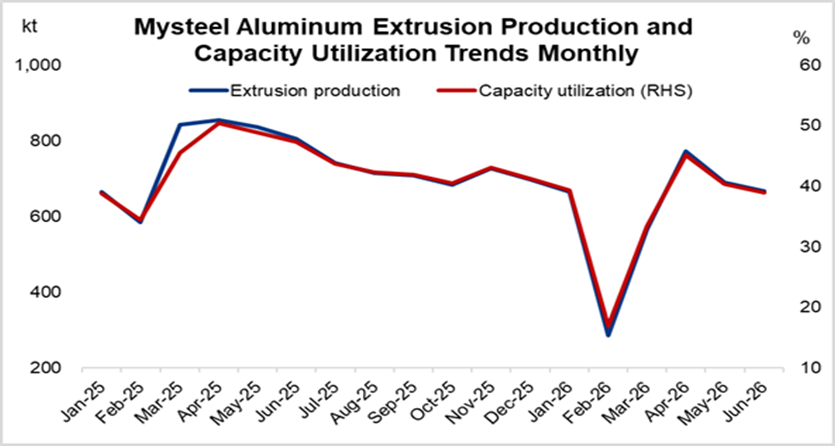

Based on weekly production and sales data from April to June 2026, the industry exhibited a clear inflection point characterized by an initial rise followed by a decline. April marked the peak of annual production; however, output weakened rapidly entering May. By late June, production across the sector experienced a significant downturn. Both building materials and industrial materials saw notable declines, with weekly capacity utilization plummeting to a cyclical low of 37.05%.

Source: Mysteel

Start-up rates showed distinct divergence. Equipment operating rates remained stable within the 55%-57% range, indicating no large-scale idling of existing equipment. However, the continuous decline in capacity utilization rate reflects enterprises' proactive measures to reduce production schedules and output, thereby lowering effective production.

According to market research in East China, amid current weak demand, some small aluminum extrusion factories have opted to suspend operations to avoid losses, refusing orders that would result in deficits. Specifically, the decline in demand for architectural building extrusions is significantly steeper than that for industrial extrusions.

Orders and scheduling: orders peak and fall, downstream procurement willingness persists in declining

Order data directly reflects the sluggish terminal demand. In April, unfinished orders held by the extrusion companies reached a cyclical peak, with average comprehensive scheduling periods extending up to 10-15 days, indicating ample downstream orders at the time. Since May, the volume of orders on hand has trended downward amidst fluctuations, and the scheduling cycle has shortened correspondingly. The subsequent average comprehensive scheduling period narrowed to merely 8-10 days, signaling a simultaneous contraction in both order reserves and delivery timelines.

Regional market transactions further corroborate the weak demand. In Anyi, Jiangxi, inquiries for Re-melted Aluminum Bars (A-1250) were only tentative even when aluminum prices hovered around Yuan 22,750/tonne. Buyers continued to aggressively drive down prices amid strong wait-and-see sentiment. Most inquiries remained purely formal business exchanges, with no substantial bulk purchases materializing.

Inventory side: synchronized drawdowns in raw materials and finished goods, not driven by demand recovery

Inventory data shows a synchronized destocking trend; however, this constitutes a passive destocking driven by production cuts rather than an improvement in terminal demand.

Raw material inventory decreased by 15.68% from late April to late June. Aluminum processing enterprises proactively scaled back raw material stockpiling to hedge against inventory devaluation losses caused by falling prices.

Finished goods inventory slide by 14.86% from its April peak to late June. The core reason is factory production cuts coupled with insufficient downstream uptake. Manufacturers aimed to reduce the massive capital tie-up caused by goods piling up, while active replenishment and digestion of inventory through terminal channels remained limited.

Significant substitution shifts emerged in the raw material structure. Aluminum scrap circulation was sluggish and supply was tight. In Hubei, the purchase price of scrap stood at Yuan 19,300 /tonne, pushing the feedstock cost of downstream aluminum extrusions to Yuan 19,600-19,700 /tonne. After deducting costs for smelting, labor, and energy consumption, the processing segment yielded no profit.

Concurrently, as aluminum extrusion output fell, the volume of finished goods inventory also dropped, which to some extent reduced the output of aluminum scarp. Unwilling to sell aluminum scrap at a loss, extrusion plants caused the difficulty of sourcing aluminum scrap to surge dramatically. As aluminum prices plummeted to lows, profits for re-melted bar factories shrank or turned into losses, forcing them to reduce inventory and cut production.

Meanwhile, the market faced a shortage of tax invoices; the purchase price of tax-inclusive re-melted bars was even far higher than that of molten aluminum bars. This drove up processing fees for molten aluminum bars, and high prices made downstream buyers wary, reducing their raw material procurement.

As aluminum prices crashed, many aluminum extrusion plants switched to using primary aluminum ingots instead of scrap to organize the production of bars to lower manufacturing costs, further dampening their willingness to stockpile raw materials.

Market outlook

In the short term, the market weakness is expected to persist through July, characterized by low capacity utilization rates and thin trading volumes. Constraints on incremental exports of aluminum ingots and aluminum products are unlikely to ease soon, and the model of processing at a loss for aluminum scrap alongside the shift to primary aluminum ingot substitution will continue. Downstream wait-and-see sentiment is difficult to reverse; aluminum extrusion enterprises will maintain low capacity utilization rates, and the scope of shutdowns among small and medium-sized factories may expand further. Aluminum prices are prone to fall but hard to rise, keeping circulation across the industrial chain subdued.

The market widely pins hopes for recovery on August, anticipating a moderate pullback in aluminum prices to stimulate rigid demand from construction and industrial terminals through lower costs.

However, recovery hinges on a clear premise that it can only rely on domestic demand improvement, not export increments to shore up the bottom. If end-market orders fail to show a warming trend in August, the pressure of domestic oversupply will continue to suppress profits across the entire industrial chain, and the scale of losses in the industry will widen further.

Conclusion

In the latter part of Q2 2026, the aluminum extrusion industry has entered a cycle of dual weakness in supply and demand. The production side has proactively slashed output drastically, orders and scheduling continue to weaken, and regional market inquiries are numerous in intention but scarce in substance. Circulation of recycled aluminum raw materials is blocked, prompting a comprehensive shift in industry production feedstock towards primary aluminum ingots.

Domestic oversupply cannot be offset by foreign shortages with restrictions on aluminum ingot export policies and the fact that over 85% of domestic aluminum product demand relies entirely on the domestic construction and industrial end-markets. The end-market consumers continue to wait and see while driving down prices, prompting the extrusion companies to cut production and control output. Under the traditional off-season circumstances, production volume is set to decline further.

It is worth noting that although the automotive industry faces pressure from a high base back in 2025, it has confirmed entry into an upward channel from a long-cycle perspective, which may drive demand in the extrusion sector.

Conversely, the building materials industry continues to be suppressed by weak demand and high inventories, with its prosperity remaining at a low level. Moving forward, the inflection point for the industry highly depends on the repair of domestic terminal demand in August and September.

Written by Regina WANG

wangjiaqie@mysteel.com