According to data released by the China Passenger Car Association (CPCA), the domestic auto market in June 2026 was characterized by overall pressure, sequential improvement, and extreme structural divergence. Against a backdrop of sharp contraction in internal combustion engine (ICE) vehicle demand, electric vehicles (EVs) have continued to consolidate their market dominance, with penetration rates staying at record highs and exports emerging as the key growth engine.

In detail, domestic passenger vehicle retail sales reached 1.602 million units in June, down 23.2% year-on-year but up 6.1% month-on-month. Cumulative retail sales for the first half stood at 8.701 million units, down 20.2% year-on-year, based on CPCA.

Within this, EV performance remained resilient. Retail sales of EVs totaled 1.007 million units in June, down 9.4% year-on-year but up 6.0% month-on-month, with a retail penetration rate of 62.8%. Wholesale NV sales reached 1.481 million units, up 19.2% year-on-year and 9.6% month-on-month, with a wholesale penetration rate of 62.8%.

The EV production stood at 1.439 million units, up 21.4% year-on-year and 3.0% month-on-month.

Exports were a standout, with EV passenger vehicle exports reaching 499,000 units, up 152.7% year-on-year and 17.6% month-on-month, accounting for 56.9% of total passenger vehicle exports.

With domestic retail sales declining year-on-year, the strong growth in production and wholesale was largely driven by exports, signaling a significant shift in the industry's growth engine.

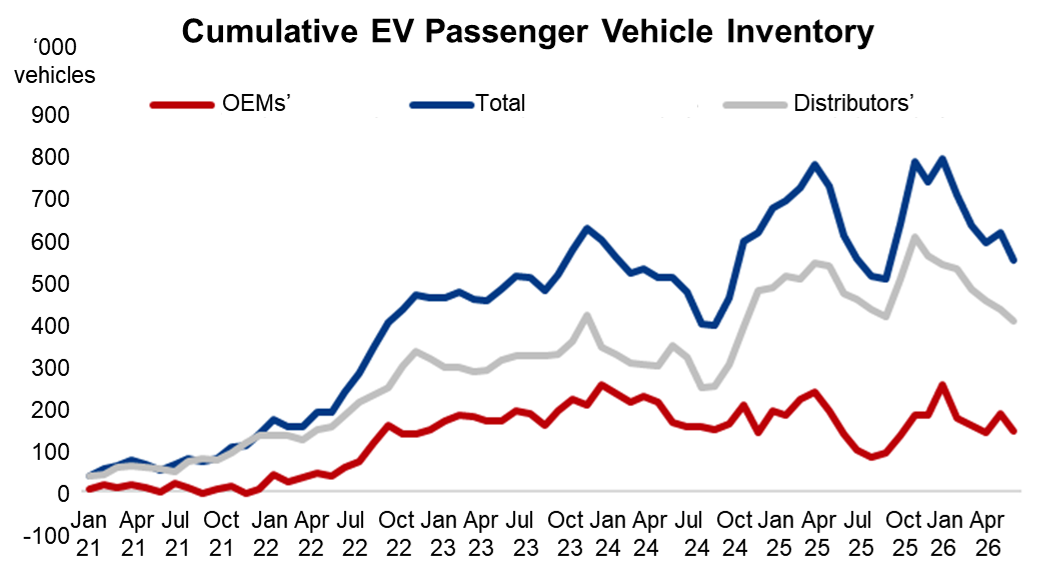

On the inventory front, as of end-June, OEMs' cumulative EV inventories stood at 144,000 units, and the distributors reported an EV inventory at 410,000 units, all modestly lower than the previous month, suggesting a transition from active to passive destocking. When converted to inventory days, the distributors' EV inventory days stood at 12.26 days, with OEMs at 3.29 days.

Source: Mysteel

Within this total, the OEMs' share in total inventory fell to 26% from 29.9% in May, but remained above the 22.3% level a year ago, reflecting a still cautious production buffer among OEMs.

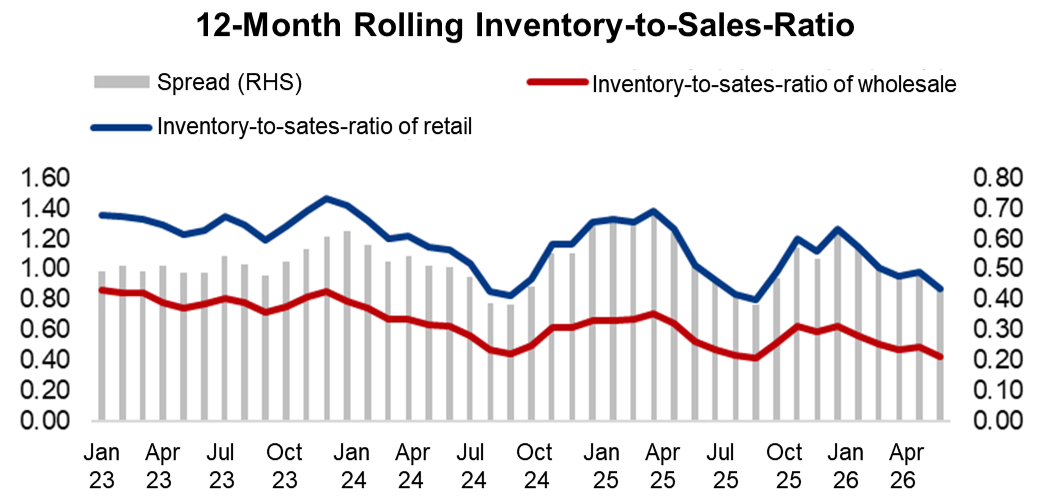

The difference between 12-month rolling inventory-to-sales-ratio in retail and wholesale markets has been narrowing month by month since January 2026. In June, exports as a share of wholesale rose slightly to 33.7%, compared with the H1 average of 33.2%.

Source: Mysteel

Looking more closely at the market structure, June saw a sharp contraction in ICE vehicle sales. Retail sales of conventional ICE passenger vehicles fell to just 600,000 units, down 39% year-on-year, with wholesale at 880,000 units, down 30% year-on-year. ICE vehicles' share shrank to 37.2%.

By contrast, conventional hybrids fared better, down 7% year-on-year but up 24% month-on-month. High oil prices and shifting consumer preferences continue to accelerate the oil-to-EV transition, with EVs now firmly the dominant force in the market.

On the other hand, when retail penetration of EVs stood at 62.8%, it means that more than six out of every ten passenger vehicles sold domestically are electric vehicles.

Penetration varies sharply by brand category. Local brands posted EV retail penetration of 81.8%, accounting for 63.2% of total EV retail, making them the clear leaders in electrification. Premium brands saw EV penetration of 39.6%, while mainstream joint ventures recorded only 11.9% EV penetration. While joint ventures saw a 45% year-on-year increase in EV sales, the base is extremely low, and they remain heavily dependent on ICE vehicles.

With domestic retail sales declining year-on-year, exports have become the key driver of wholesale and production growth.

Passenger vehicle exports reached a record 877,000 units in June, up 82.3% year-on-year, breaking into a higher range for the first time. EV exports accounted for 499,000 units, or 56.9% of total exports, a record share and a year-on-year increase of over 150%.

Local brands, leveraging their mature EV technology and cost advantages, are displacing ICE vehicles overseas and helping absorb domestic production capacity.

In terms of OEM rankings, June EV retail sales showed a clear pattern of one dominant leader, multiple strong followers, and rising EV start-ups.

BYD topped the list with 224,478 units, maintaining a commanding lead, though retail growth was weighed down by a high base. Geely followed with 107,951 units, staying at the forefront of the second tier, supported by its Galaxy series.

EV star-ups continued to gain ground. Leapmotor posted 72,376 units, up 61.1% year-on-year, one of the few strong positive growth brands among the top ten. Xiaomi Auto delivered 34,738 units, breaking through the 30,000-unit mark for the first time. NIO and Xpeng also held their ground, lifting the EV start-up segment's combined market share by 6.5 percentage points year-on-year. Tesla China sold 52,920 units, down 0.2% yearon-year, staying in the upper ranks but facing intense competition from domestic rivals.

By technology pathway, June wholesale volumes showed BEVs at 981,000 units, up 26.9% year-on-year, PHEVs at 406,000 units, up 18.1% year-on-year, and EREVs at 94,000 units, down 25.2% year-on-year.

The June data points to three medium-term trends as the first half of 2026 comes to a close.

First, with EV penetration above 60%, incremental growth has slowed, and the market has entered a phase of market-share fighting, with price wars and distributors' inventory pressure likely to persist.

Second, a dual-engine growth model has been established, with domestic demand driven by structural substitution of ICE vehicles and external demand relying on the high-growth trajectory of EV exports. The rising share of exports is reshaping OEM production planning and pricing logic.

Third, the urgency for joint venture electrification has increased, as EV penetration among joint ventures remains below 12%, widening the gap with local brands.

In summary, while domestic ICE demand remains the biggest drag, EV passenger vehicles are likely to continue a structural recovery amid volatility, supported by the implementation of new battery standards and improving overseas demand.

Written by Aggie Hu, huchenying@mysteel.com