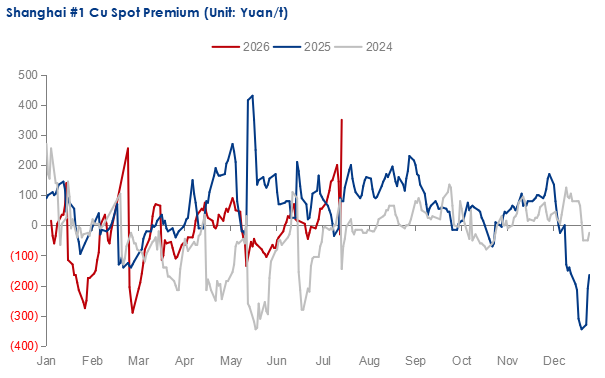

China's refined copper spot premiums and nearby futures spreads have been strengthening recently despite the current demand off-season, primarily reflecting tightening available spot supply. Coinciding with the contract rollover, Shanghai's #1 refined copper spot premium reached Yuan 350/dmt on July 16, the highest level entering 2026, while the SHFE copper futures curve from July through December has fully shifted into backwardation.

Data Source: Mysteel

A widening backwardation indicates that buyers are willing to pay a higher price for immediate delivery than for future supply, reflecting increasingly scarce prompt material. Intensified smelter maintenance, persistent shortages of smelting raw materials, constrained import arrivals and rapid inventory declines have collectively tightened spot refined copper availability.

Refined copper output shrinks due to maintenance and raw material tightness

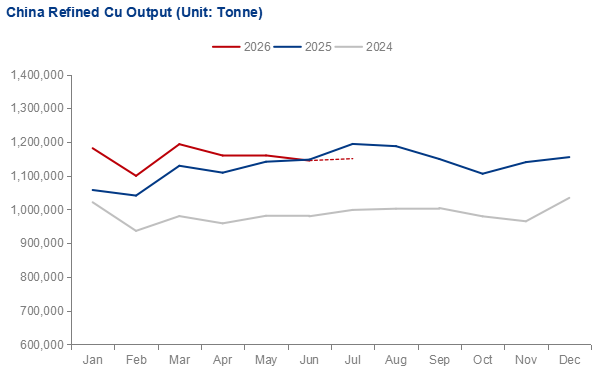

According to Mysteel's survey, China's refined copper output declined month on month in June, also marking the first year-on-year decrease in 2026. The decline was primarily driven by an intensive round of smelter maintenance, as eleven smelters conducted maintenance during the month, reducing refined copper output by approximately 76,000 tonnes, marking the largest monthly production impact so far this year.

Data Source: Mysteel

Meanwhile, concentrated maintenance has coincided with the persistent squeeze in smelting raw material availability. Imported copper concentrate treatment charges (TCs) continued to fall to historically low levels, with Mysteel's TC index dropping to -$134/dmt as of July 10, indicating severe supply tightness, caused mainly by disruptions at overseas mines and slow mining capacity growth. In addition, copper scrap supply in China also stayed tight, as invoice-related issues have not been effectively settled, and recent copper scrap imports also dropped. Consequently, copper anode production has been impacted and further tightened raw material supply.

With smelter maintenance persisting in July and raw material availability unlikely to recover in the near term, China's refined copper production is therefore hard to notably rebound. Mysteel's survey indicates that six smelters are scheduled for maintenance in July, including two plants extending maintenance from June, with an estimated production impact of around 38,000 tonnes. Domestic refined copper output is expected to reach 1.1508 million tonnes in July, up only 0.5% month on month and still down 3.65% year on year, suggesting supply growth remains constrained despite a modest monthly recovery.

Spot copper circulation tightens faster than production

While lower production has reduced overall supply, spot availability has tightened even more sharply.

An increasing proportion of refined copper has been traded directly between smelters and downstream enterprises, according to Mysteel, reducing the volume of material entering the spot market. Meanwhile, some smelters have temporarily oversold cargoes, limiting their ability to deliver branded copper into warehouses. As a result, the availability of registered domestic brands in the spot market has become increasingly scarce. Therefore, the reduction in spot circulation significantly strengthened sellers' pricing power and supporting higher spot premiums.

Import copper fails to effectively compensate for spot supply

Recent typhoon-related weather disruptions have delayed the arrival of some imported copper cargoes, while spot availability in the bonded market has remained limited. Meanwhile, the U.S. refined copper import tariff policy has been uncertain, promoting continuous inflows of copper into the U.S and therefore tightening non-U.S. copper supply. Yangshan copper premiums have continued to rise, indicating tightening overseas supply and increasing costs for immediate imports.

Consequently, imported copper has been unable to compensate for reduced domestic deliveries. The combination of constrained domestic shipments and limited import arrivals has further reduced prompt spot availability, encouraging sellers to hold firm on offers and contributing to the continued rise in spot premiums.

Resilient demand accelerates inventory declines

Although China has entered the traditional consumption off-season, downstream demand has proven relatively resilient. Downstream and end-user enterprises have gradually accepted elevated price levels, increasing rigid procurement and stockpiling during occasional price declines.

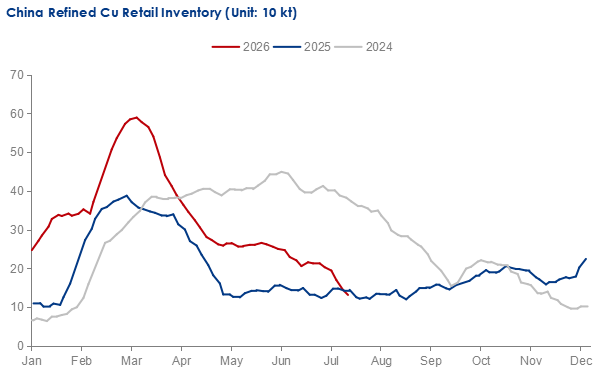

The imbalance between limited arrivals and relatively stable consumption has been clearly reflected in inventory movements. As of July 16, China's refined copper retail inventory stood at 131,400 tonnes, falling sharply from 212,800 tonnes at the end of June, marking the lowest inventory level this year. Rapid inventory depletion further reinforced market expectations of tightening spot supply, and holders have become increasingly reluctant to sell, allowing spot premiums to rise further while reinforcing the nearby SHFE backwardation structure.

Data Source: Mysteel

Refined copper available spot supply expected to stay tight and support premiums

Looking ahead, factors underpinning the current supply tightness are unlikely to ease quickly.

On the supply side, several smelters will remain under relatively long maintenance schedules, while the third quarter is expected to enter another concentrated maintenance period. More importantly, copper concentrate availability continues to deteriorate, with TCs remaining at historical lows and no meaningful improvement expected in the near term. Even though elevated sulfuric acid prices will support smelters' profits, raw material shortage will begin to actually impact refined copper output. Meanwhile, tight scrap supply and ongoing invoice-related disruptions are also likely to continue constraining anode copper production and refined copper smelting raw material availability.

Imports are likewise expected to remain constrained. According to Mysteel, long-term import contracts signed for 2026 declined compared with previous years due to high premiums, while geopolitical uncertainties and shipping disruptions could continue to affect overseas arrivals. In addition, a relatively high proportion of China's imported copper consists of non-registered or non-standard material, limiting the volume of deliverable brands available to the domestic spot market.

Taken together, these factors suggest that spot liquidity will remain constrained through the third quarter in China. Under this scenario, nearby SHFE backwardation is expected to remain elevated, while Shanghai's refined copper spot premiums are likely to stay firm, with premiums of Yuan 400-500/tonne achievable during possible periods of particularly tight spot availability.

Don't miss Mysteel's H1 2026 Copper Market FREE Webinar! Check the link below to learn more, and register to secure your spots:

H1 2026 Saw Intertwined Contradictions in China's Copper Market - What's Next for H2?

Written by Mingyuan Wang, wangmingyuan@mysteel.com