Analysis on China's power battery production and installed capacity

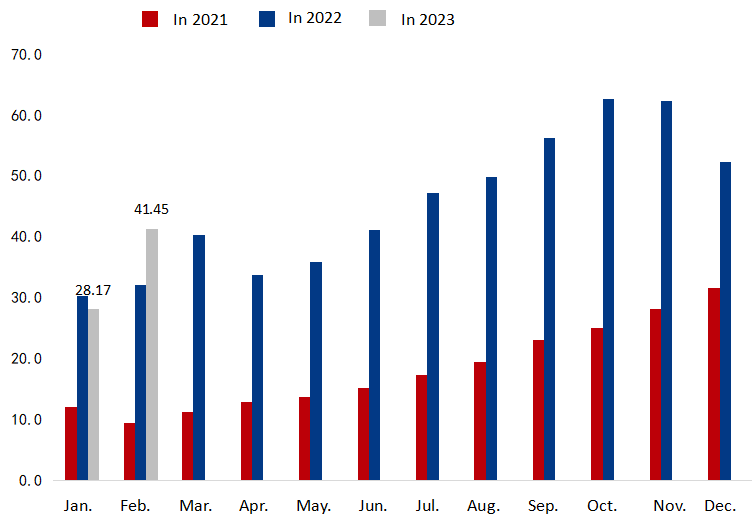

According to the data from China Automotive Battery Innovation Alliance, China's production of power batteries stood at 41.45 GWh in February 2023, rising by 47.1% month on month and 29.1% year on year respectively. Negating the impact of the Chinese New Year holiday, the combined production of power batteries over January-February reached 69.62 GWh, up by 11.3% from last year's 62.54 GWh. The country's power battery production slackened off considerably in response to the slowing year-on-year growth in new energy vehicle (NEV) sales, with the battery production in the month below the monthly average over July-December last year.

Figure 1-1: The production of power batteries in China (Unit: GWh)

Sources: China Automotive Battery Innovation Alliance and Mysteel

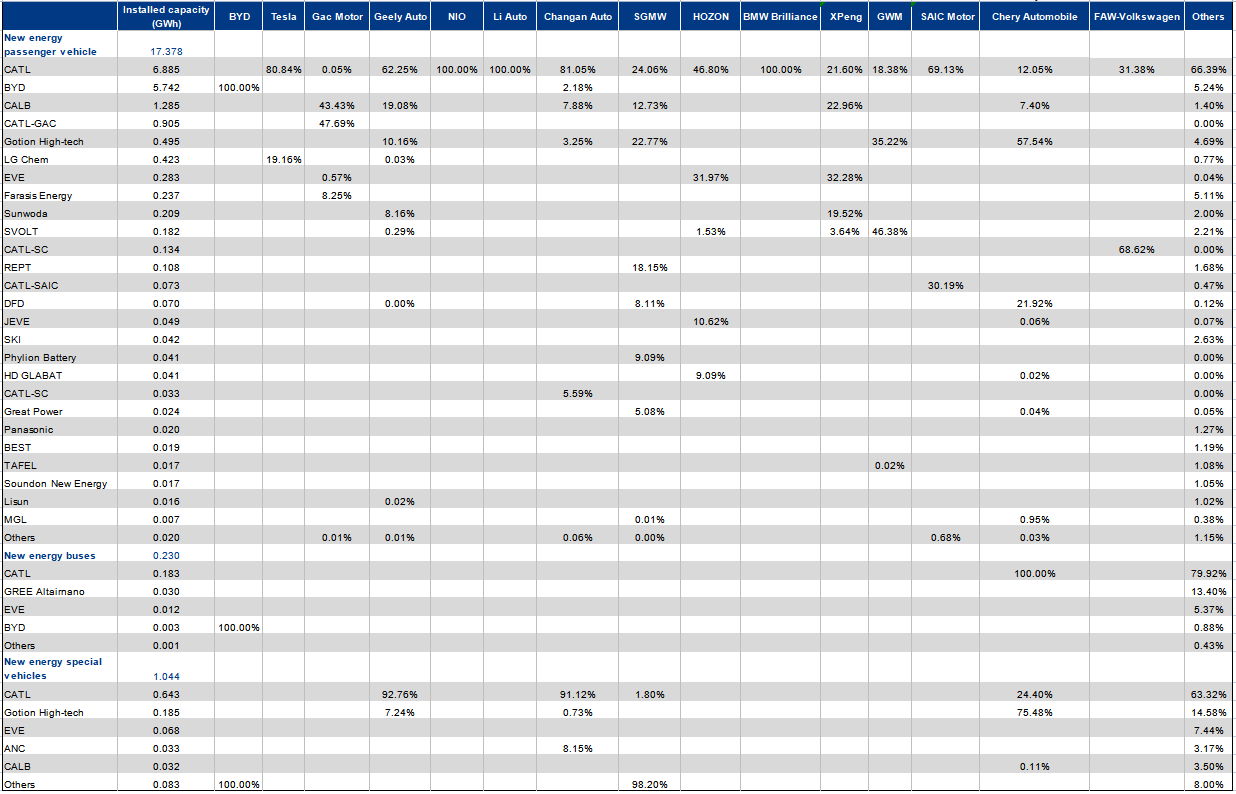

China's installed capacity of power batteries totaled 18.65 GWh in February this year, jumping by 37% from January and surging 73% year on year. Within the total, the installed capacity of power batteries for new energy passenger vehicles was about 17.38 GWh, rising by a large 74% year on year; that for new energy buses climbed 24% year on year to approximate 0.23 GWh; and that for new energy special vehicles was around 1.04 GWh, with a year-on-year increase of 63%. The combined installed capacity of power batteries over January-February reached 32.25 GWh.

In 2022, about 294.6 GWh of power batteries were installed on NEVs, while the total power battery sales were significantly higher at 460 GWh. Moreover, power battery inventories across the entire industry chain reached approximately 165 GWh for the year. Based on the recent production and installed capacity of power batteries, the domestic battery industry still sees inventory accumulation at the current stage. It is expected that the production gap between large and small battery plants will widen, and the overall operating rate of the battery industry may decline further.

Analysis on China's power battery sales by manufacturer

Top 10 automakers in terms of NEV sales installed about 14.45 GWh of power batteries in February, accounting for 77% of the total. Notably, power batteries from Contemporary Amperex Technology (CATL) and BYD separately made up 42% and 39% of the combined installed capacity among the top 10 NEV manufacturers.

Table 1-1: Battery supplies to new energy passenger vehicle makers in February (Based on insurance registration statistics)

Sources: Compulsory traffic insurance and Mysteel

With a dominant 41.4% market share, CATL makes more power batteries than any other company in China. Its biggest customer Tesla bought 22.4% of all the batteries CATL sold and had 80.8% of its installed batteries from CATL. Apart from Tesla, CATL's top five customers were NIO, Geely Auto, Li Auto, Changan Auto, and BMW Brilliance, with their installed batteries provided by CATL making up 13.9%, 9.9%, 9.1%, 6.8%, and 5.3% of the battery giant's total battery supply respectively. Also, the batteries installed on Li Auto, NIO and BMW Brilliance were all supplied by CATL.

BYD ranked second with a rapidly growing market share of 30.8% and it gradually closed the gap with CATL. BYD's subsidiary Fudi Battery supplied 93% of its batteries to BYD, also leaving a very small portion to supply FAW Group, Changan Auto and Changan Ford, etc. Besides, BYD mainly produces lithium iron phosphate (LFP) batteries, and it is expected that BYD's robust NEV sales in 2023 may support its installed capacity to increase further. CALB, CATL GAC, BYD and Gotion High-tech ranked third, fourth and fifth respectively in terms of battery market share in China. The combined power battery installations of the top five battery makers accounted for 87.73% of the total.

Among the top 10 battery manufacturers in terms of power battery installation and market share, the rankings of CATL GAC, LG Chem and Farasis Energy moved up in February as compared with January, while EVE and Sunwoda saw their rankings slip in the same month, indicating increasingly fierce competition among second-tier battery plants. The combined installed capacity of power batteries from the top 10 battery manufacturers reached 17.78 GWh in February, taking 95.32% of the domestic market, which suggested a further market concentration towards leading power battery plants.

Table 1-2: Summary of power battery installations in February 2023 (Unit: GWh)

|

Battery manufacturers |

Installed capacity in Feb. |

Market share |

|

CATL |

7.71 |

41.35% |

|

BYD |

5.75 |

30.82% |

|

CALB |

1.32 |

7.06% |

|

CATL GAC |

0.90 |

4.85% |

|

Gotion High-tech |

0.68 |

3.64% |

|

LG Chem |

0.42 |

2.27% |

|

EVE |

0.36 |

1.95% |

|

Farasis Energy |

0.24 |

1.27% |

|

Sunwoda |

0.21 |

1.12% |

|

SVOLT |

0.18 |

0.98% |

|

CFBC |

0.13 |

0.72% |

|

REPT |

0.11 |

0.58% |

|

CATL-SAIC |

0.07 |

0.39% |

|

DFD |

0.07 |

0.37% |

|

JEVE |

0.05 |

0.26% |

|

Others |

0.44 |

2.35% |

Sources: Compulsory traffic insurance and Mysteel

Analysis on installations of ternary lithium batteries and LFP batteries

For China's new energy passenger vehicles, the proportion of installed LFP batteries increased to 63.5% in February 2023 and is expected to rise further. Also, LFP batteries have a more promising prospect than ternary lithium batteries in the market. The increase in the installed proportion of LFP batteries is mainly closely related to the insurance registrations of NEVs in February. The combined insurance registrations of BYD and Tesla alone logged a market share of 44.8% in February, which also made a significant contribution to the increase in the installation of LFP batteries.

Table 1-3: Battery supplies to new energy passenger vehicle makers in February (By battery type) (Based on insurance registration statistics)

Sources: Compulsory traffic insurance and Mysteel

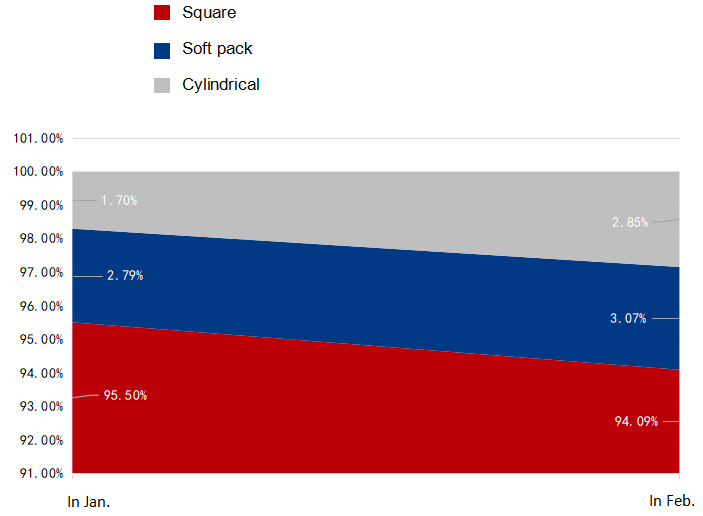

Analysis of power battery installations by packaging type

Among all installed power batteries in February, square batteries were mainstream with a dominant share of 94.09%, though down 1.48% from January; soft packs made up 3.07% of the total, up 9.72% from January; and cylindrical batteries took 2.85%, surging 67% month on month mainly due to a substantial increase in installed capacity of cylinder batteries LG Chem supplied to Tesla. The installed capacity of cylindrical batteries in Tesla was 0.41 GWh in February, soaring 152.73% compared to January's 0.16 GWh, while Chery Automobile recorded 0.05 GWh of installed cylindrical batteries from Gotion High-tech, making it the second-largest automaker after Tesla in terms of cylindrical battery installations.

Figure 1-2: Proportion of installed power batteries in January and February by packaging type

Sources: Compulsory traffic insurance and Mysteel

As more NEV models are introduced this year, the rivalry among NEV automakers has become increasingly intense. The price cuts initiated by leading NEV automakers can help increase their sales effectively. Meanwhile, the rapid decline in lithium carbonate prices is expected to pull down battery costs, giving NEV automakers more room to cut prices and thus driving up the insured volume in March. It is predicted that China may have 560,000 units of new energy passenger vehicles insured in March, with a month-on-month increase of 42% and a year-on-year increase of 21%, and the combined new energy passenger vehicles insured over January-March is likely to rise by 19.5% year on year. In addition, the market dominance of NEV automakers allows them to gradually gain pricing power in the entire NEV sector, thereby squeezing profit margins for NEV parts manufacturers and material plants in the upstream.

Written by Mysteel Nonferrous Metal & New Energy Research Center

Edited by Ruby Zhang, zhangjiajing@mysteel.com; Alyssa Ren, rentingting@mysteel.com