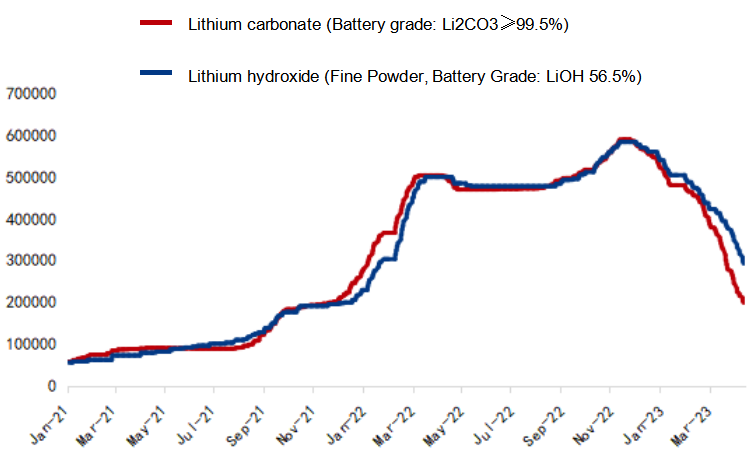

Chinese price of battery-grade lithium carbonate decreased by Yuan 22,500/tonne or 10.47% week on week to Yuan 192,500/t over the survey week of April 10-14, plunging a total of 66.3% since reaching its peak, while that of battery-grade lithium hydroxide also fell by Yuan 42,500/t or 13.47% week on week to Yuan 273,000/t, down by 49.8% overall from its peak high.

Figure 1-1: Price trend of lithium carbonate and lithium hydroxide in China (Unit: Yuan/tonne)

Source: Mysteel

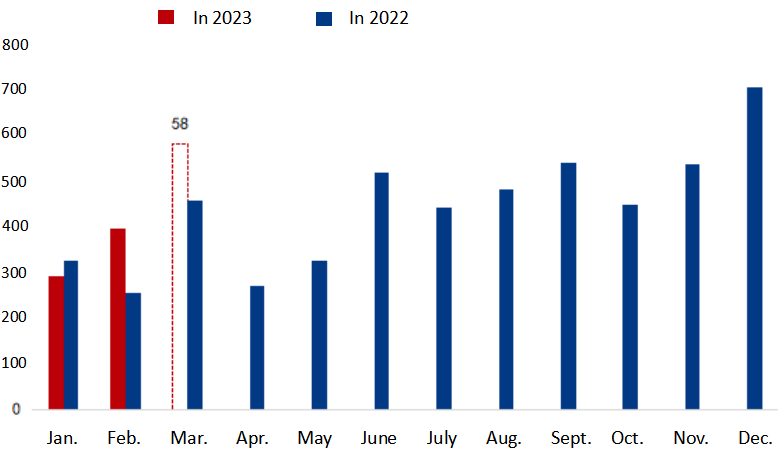

The insured new-energy passenger cars in China were expected to reach 580,000 units in March this year, up 27.19% year on year and jumping 47.21% from February. The tail-raising trend of insured new-energy passenger cars in the last two weeks of March suggested that the price cuts on traditional fuel vehicles have not hurt the demand for new-energy vehicles (NEVs).

Figure 1-2: New energy passenger vehicle sales in China (Unit: '000 units)

Source: Mysteel

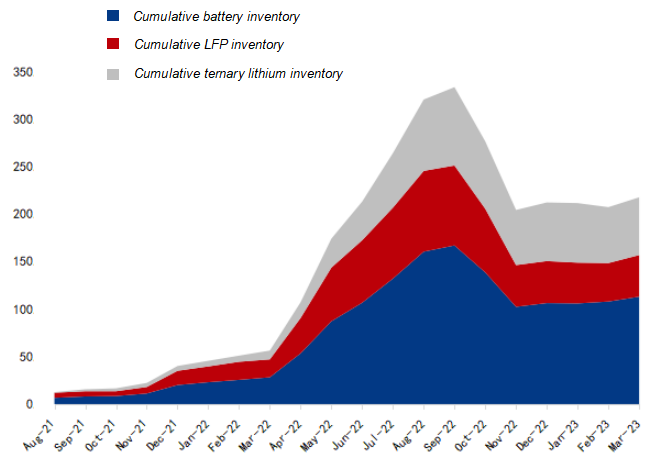

The inventories of power batteries in the downstream had climbed steadily since March 2022, and reached a high of 166.9 GWh in September last year. After that, downstream NEV producers have slowed their buying, and their power battery stocks hover at 113 GWh currently. Based on estimated monthly installations of 25-30 GWh, the battery inventory cycle for NEV makers is two to three months. The battery inventories include those on undelivered vehicles.

Figure 1-3: Cumulative battery inventory of downstream manufacturers in China (Unit: GWh)

Source: Mysteel

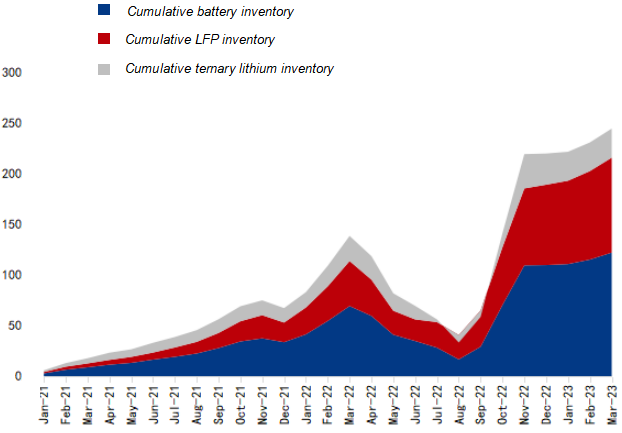

Due to the slowdown in downstream procurement, battery factories saw their in-plant stocks rise further to hit a new high of 122.3GWh in March, among which lithium iron phosphate (LFP) batteries reached 93.8 GWh, far exceeding the 28.7 GWh inventory of ternary batteries, and the inventory cycle of LFP batteries is two to three months, while that of ternary batteries is one to two months.

Figure 1-4: Battery inventory at battery plants in China (Unit: GWh)

Source: Mysteel

High battery inventories at battery factories also affected upstream material factories' production schedules in April. According to Mysteel's statistics, China's cathode material production increased slightly in March, with the production of ternary materials rising 4.91% month on month to 44,980 tonnes, and the LFP output up 4.94% month on month to 78,600 tonnes. However, factories' production plans for ternary materials in April showed a 6.24% month-on-month decrease, as some battery makers shifted to producing energy storage batteries in response to the slowdown in demand for power batteries and their high inventories of this product.

Table 1-1: The production and production schedules of cathode material and lithium compound (Unit: tonne)

|

|

Production in Mar. 2023 |

MoM (%) |

YoY (%) |

Production schedule in Apr. 2023 |

MoM (%) |

YoY (%) |

|

Ternary cathode material |

44,900 |

4.91% |

6.47% |

42,100 |

-6.24% |

15.12% |

|

LFP |

78,600 |

4.94% |

40.11% |

77,200 |

-1.78% |

34.73% |

Source: Mysteel

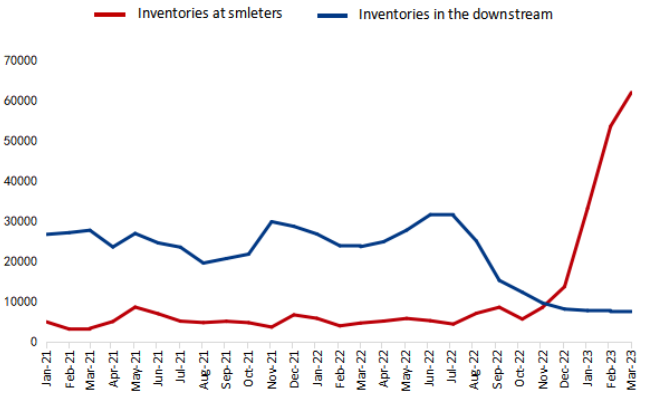

Since downstream industries are in the off-season and lithium prices have yet to stabilize, end-users opt to buy batteries in the spot market to meet immediate needs, which allow them to enjoy the lower retail prices for lithium carbonate as compared with long-term contract prices and avoid inventory write-downs as well. According to Mysteel's survey, cathode material factories' lithium compound inventories could only last them for two or three days, while for some LFP cathode factories, their stocks are just enough for half a day's use.

Figure 1-5: China's lithium carbonate inventories (Unit: tonne)

Source: Mysteel

On the supply side, companies that purchase lithium concentrates to produce LFP have largely stopped production. Some LFP producers in Jiangxi have reduced their output, particularly those with smaller capacity. However, leading LFP companies with low-cost advantages still maintain normal production despite high inventory levels. The production cuts and shutdowns are mainly due to cost factors, and there are significant differences in production costs among LFP companies given the raw materials used, material sources, and self-sufficiency rates.

At present, lithium carbonate inventories continue to climb, and the market supply remains relatively abundant. With the warming weather, the low-cost production of lithium extracted from salt lakes is steadily increasing, which will become an incremental source of supply for lithium carbonate. However, the overall lithium carbonate production may decrease due to cost reasons. According to Mysteel's statistics, the production of both lithium carbonate and lithium hydroxide will decrease month on month in April, with the volume reaching 28,500 tonnes and 21,400 tonnes, respectively.

Table 1-2: The production and production schedules of lithium carbonate and lithium hydroxide (Unit: tonne)

|

Product |

Production in Mar. 2023 |

MoM (%) |

YoY (%) |

Production schedule in Apr. 2023 |

MoM (%) |

YoY (%) |

|

lithium carbonate |

30,100 |

-15.69% |

36.85% |

28,500 |

-5.32% |

28.56% |

|

lithium hydroxide |

22,200 |

-2.63% |

51.54% |

21,400 |

-3.60% |

19.89% |

Source: Mysteel

Based on cathode material production schedules for April, the demand for lithium carbonate in the month is expected to reach 30,000-32,000 tonnes. Considering the supply side, the cost of lithium carbonate production from lithium mica mining in Jiangxi is seen as the marginal production cost, which is around Yuan 120,000-130,000/t. However, taking into account the inventories at smelters and the destocking cycle, it is expected that lithium compound prices will continue to decline in April, seeking cost support at around Yuan 150,000/t.

Written by Mysteel Nonferrous Metal & New Energy Research Center

Edited by Alyssa Ren, rentingting@mysteel.com; Ruby Zhang, zhangjiajing@mysteel.com