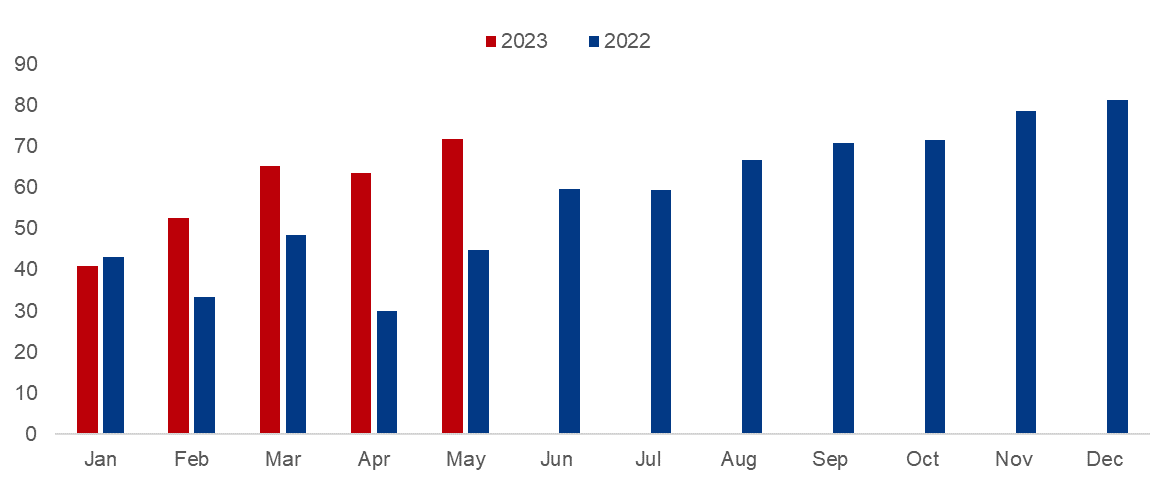

China's new energy vehicle (NEV) market achieved a MoM growth of 11.4% and 12.6% and a YoY surge of 53% and 60.2% respectively in May regarding the production and sales of NEVs at 713,000 and 717,000 units. The year-to-date (YTD) production and sales, meanwhile, amounted to approximately 3 million and 2.94 million units respectively, an increase of 45.1% and 46.8% YoY.

Figure 1-1. China's new energy vehicle sales (10,000 units)

Source: Mysteel

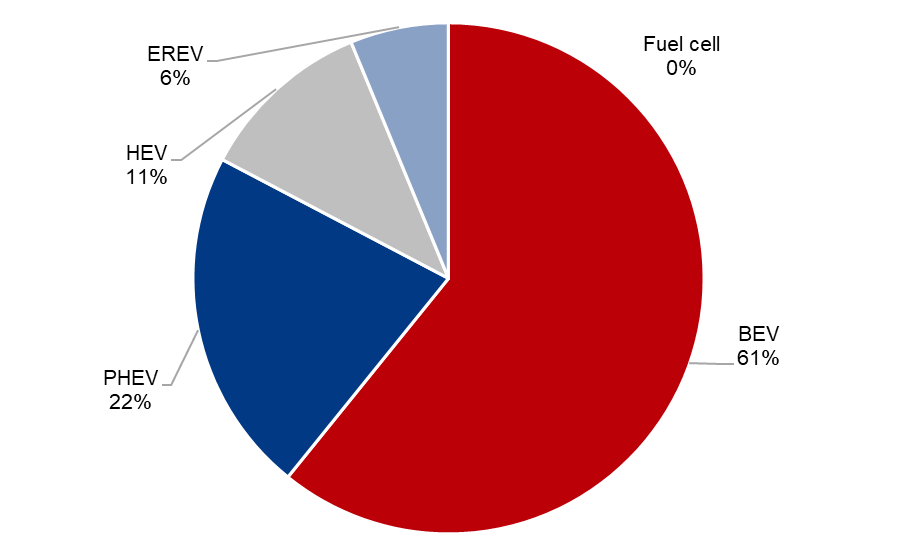

BEVs (battery-powered electric vehicles) championed the sales market by energy type with a market share of 61% in May, whose sales added 15.15% MoM, followed by PHEVs (plug-in hybrid electric vehicles) which took up 22% of the total sales, with a 10.51% increase in its monthly sales. HEVs (hybrid electric vehicles) and EREVs (extended-range electric vehicles) recorded a share of 11% and 6% respectively, and their sales rose 3.45% and 10.87% MoM. Among them, the market share of BEVs continued to climb with a monthly growth of 1.43 percentage points.

Figure 1-2. May NEV sales by energy type

Source: Mysteel

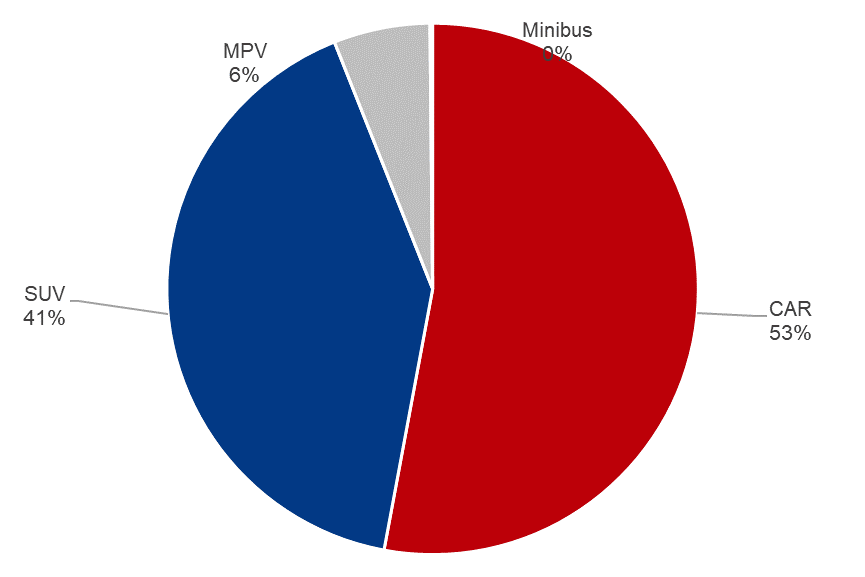

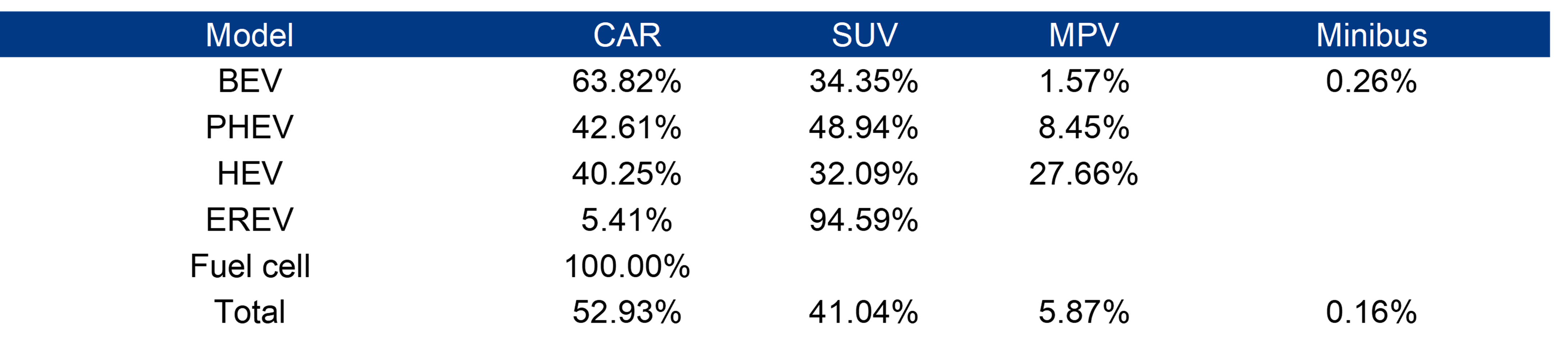

Alternatively, the NEV market could be segmented into CAR, SUV and MPV in the order of sales volume. In detail, the BEV market was largely taken by CARs, with a proportion of 63.82%, followed by SUVs at 34.35%. While SUVs led the EREV market with a share of 94.59%, the PHEV market saw a similar feature. Regarding the EREV market, apart from NETA and some Changan models that were CARs, LiAuto, Leap Motor, SERES, VOYAH and ENOVATE were basically SUVs.

Figure 1-3. May NEV sales by model

Source: Mysteel

Table 1-1. May NEV sales breakdown by model and energy type (proportion)

Source: Mysteel

In terms of vehicle class, Class A vehicles recorded the highest sales in May, trailing by Class B vehicles. The market share of Class A and A00 added 1.17 and 0.37 percentage points MoM respectively, with others all seeing a monthly drop.

Table 1-2: May NEV sales breakdown by class (proportion)

Source: Mysteel

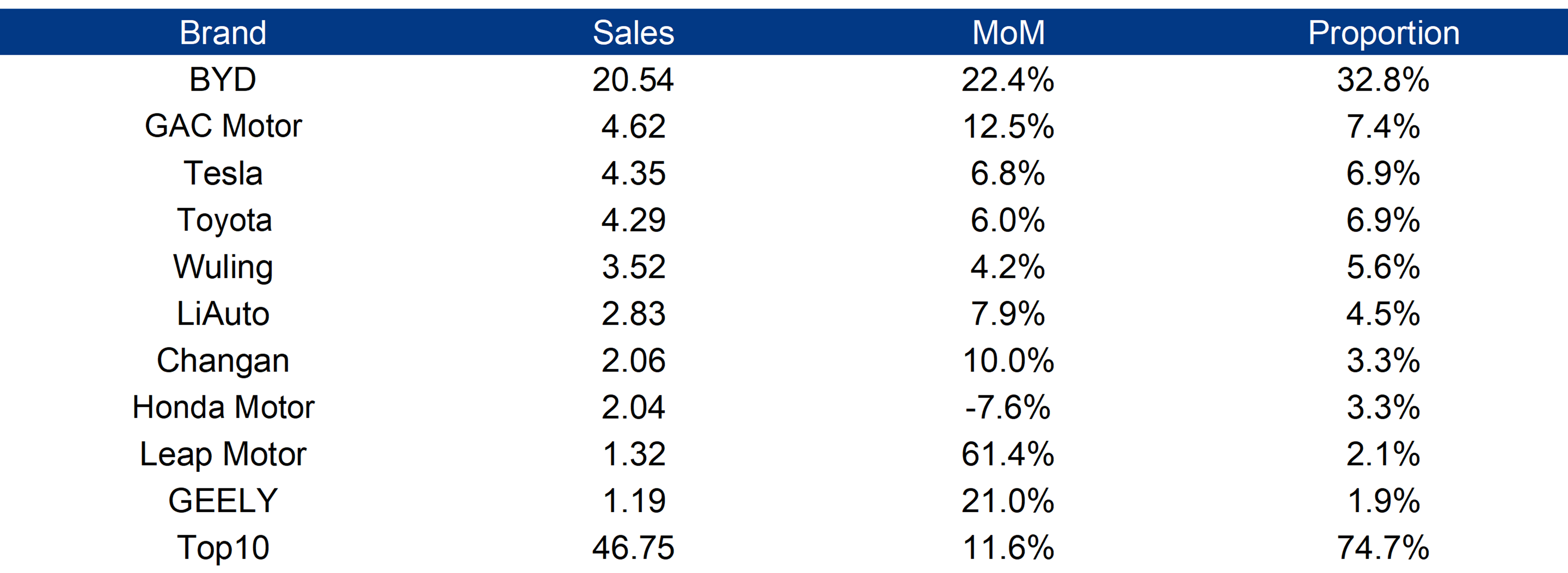

The performance of individual NEV brands was generally positive. In May, the CR10 stood at 74.7%, with a combined sales of 467,500 units, up 11.6% MoM, among which BYD, Leap Auto and GEELY set a monthly increase of over 20%. Specifically, Leap Auto was the brand with the highest monthly increase in sales, which helped it make into the Top 10 list. The Top 6 brands by sales were the same as in April.

Table 1-3. May NEV sales by brand (10,000 units)

Source: Mysteel

The BYD family remained the most popular car models in May, taking up 7 seats in the Top 15 list with BYD Qin PLUS topping the chart. Nevertheless, BYD Song PLUS was the model with the fastest growth thanks to the heavy subsidies, which was a method to clear up the inventory and make space for new BYD Song series.

Table 1-4. May NEV sales breakdown by brand model (10,000 units)

Source: Mysteel

Concerning the NEV sales with energy type, BEVs and EREVs still maintained momentum with a monthly gain of nearly 20% respectively. It is worth mentioning that though GAC Motor's PHEVs and Changan's HEVs demonstrated an astonishing MoM boost of 2,121.1% and 250% respectively in May, their actual sales volume was merely 500 units and 10 units, which had little influence on the entire market.

Table 1-5. May NEV sales breakdown by energy type and brand (MoM growth)

Source: Mysteel

Written by Aggie Hu, huchenying@mysteel.com