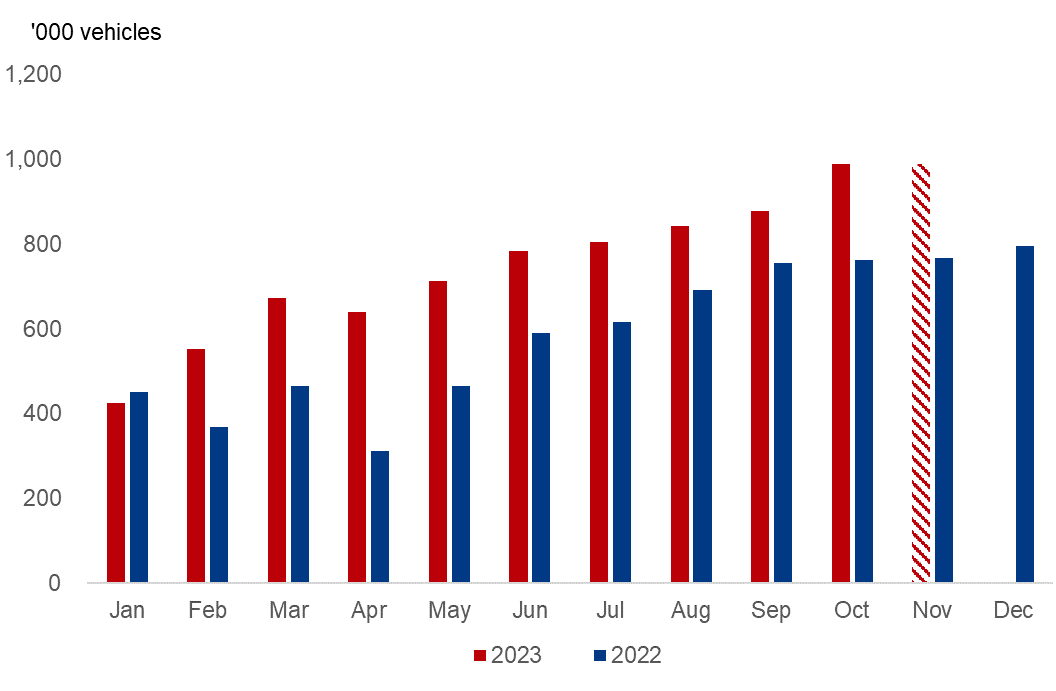

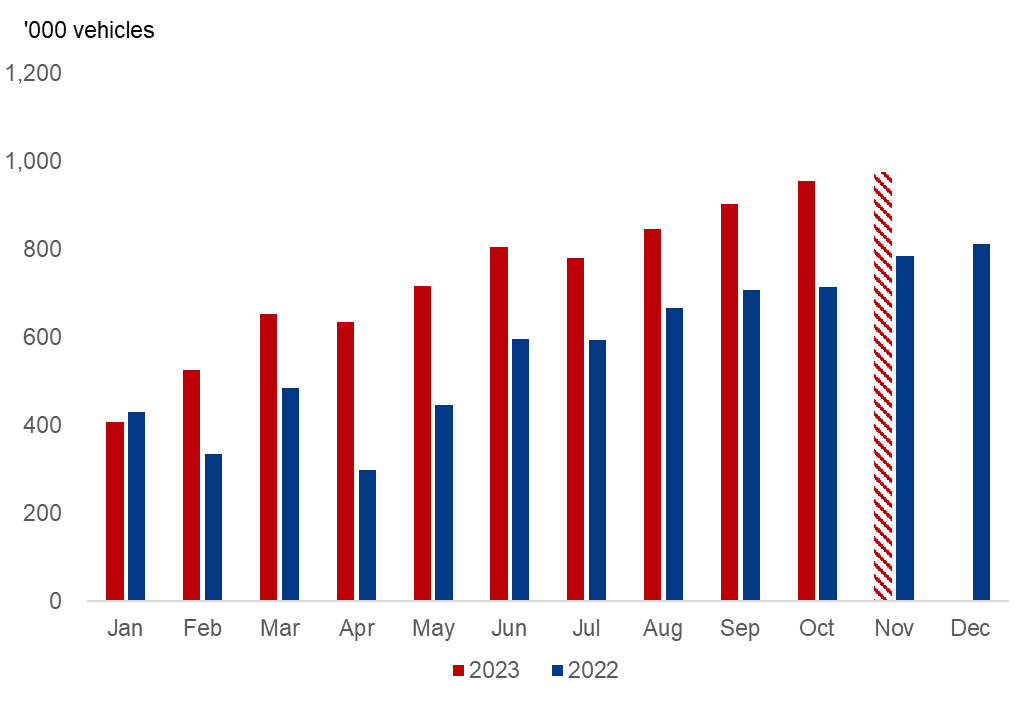

China's production and sales volume of electric vehicles (EVs) stood at 989,000 units and 956,000 units respectively in October, an increase of 12.5% and 5.8% from September, and rising 29.8% and 33.9% from last year, according to China Association of Automobile Manufacturers (CAAM). The figures ramped up to 7.3 million units and 7.23 million units respectively over January-October, marking an annual growth of 33.32% and 37.16%.

Figure 1-1. China EVs Production

Figure 1-2. China EVs Sales Volume

Sources: CAAM, Mysteel

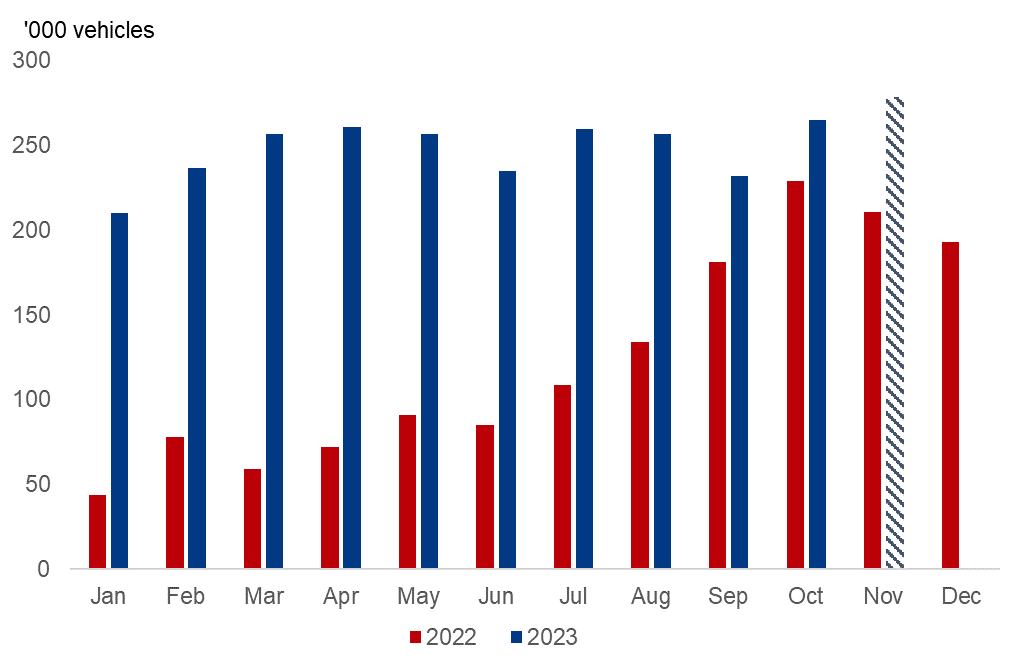

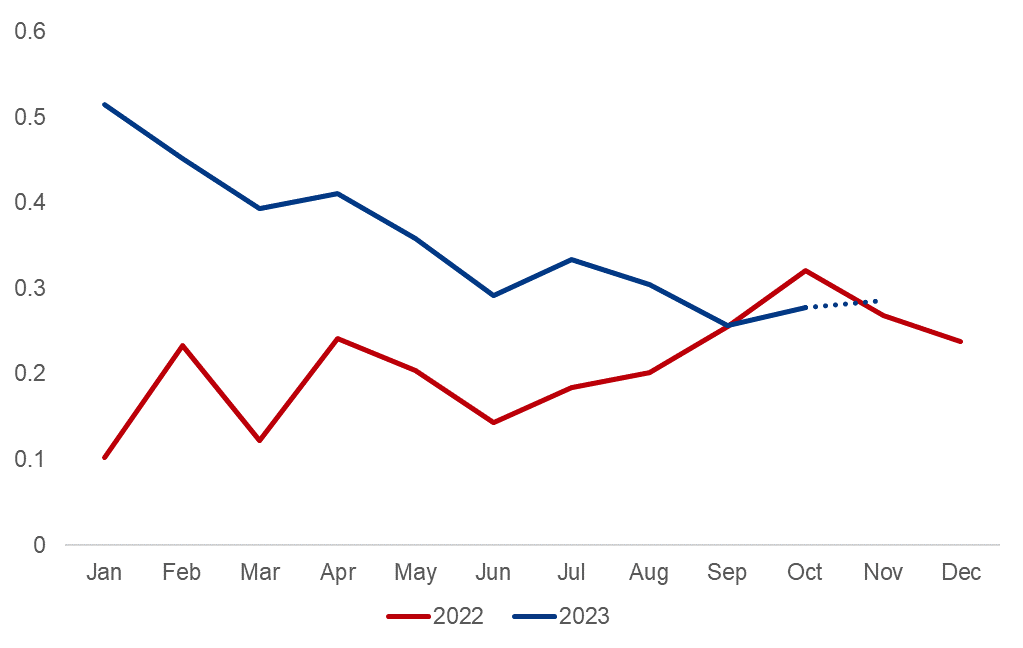

From the perspective of industrial inventory, the EVs reported a cumulative inventory of 265,000 units as of end-October, with the cumulative inventory-to-sales ratio recording 0.28, up 0.2 point from last month and down 0.4 point year on year. Generally, lower inventory-to-sales ratio indicates better sales situation.

The October EVs sales situation weakened compared with September because most carmakers would actively promote the sales around the end of the quarter, while the eight-day National Day holiday in early October reduced the days available for marketing.

It is expected that the EVs sales situation will be flat in November, with the sales volume projected to inch up 2% month on month.

Figure 1-3. China EVs Cumulative Inventory

Figure 1-4. China EVs Cumulative Inventory-to-sales Ratio

Sources: CAAM, Mysteel

On the battery end, China's production of power battery was 69.8 GWh in October, falling 0.1% MoM but rising 11.2% YoY.

In detail, the production of ternary power battery reported 23.6 GWh, an increase of 2.5% from September but down 2.5% YoY. The installed capacity jumped 0.8% MoM and 14% YoY at 12.3 GWh in October, taking up 31.4% of the total.

The production of LFP power battery was 46.2 GWh, down 1.4% from September but rising 19.7% from last year. The installed capacity stood at 26.8 GWh, rising 10.9% MoM and 36.4% YoY.

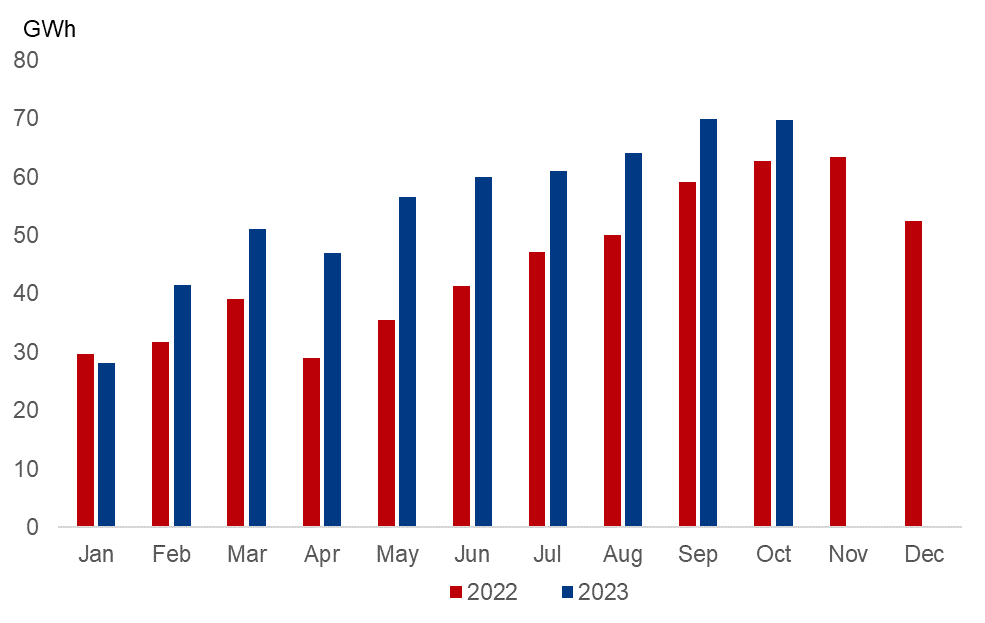

Figure 1-5. China Power Battery Production

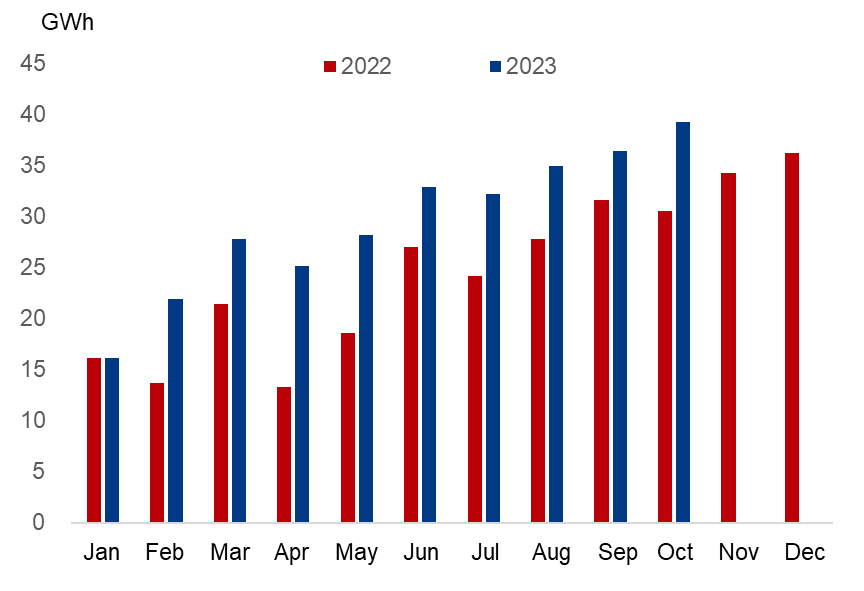

Figure 1-6. China Power Battery Installed Capacity

Sources: China Automotive Power Battery Industry Innovation Alliance, Mysteel

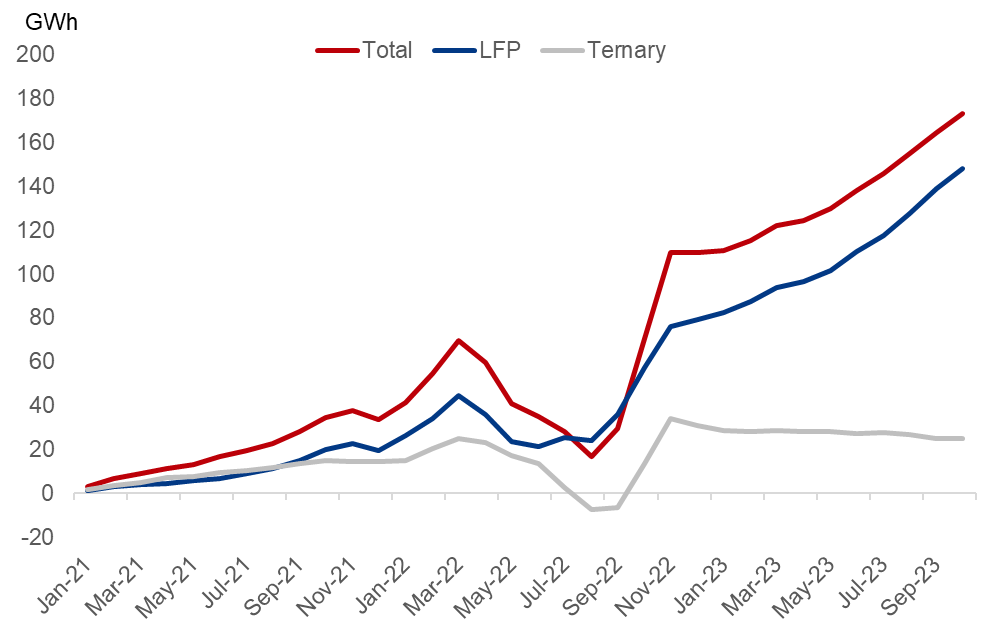

The battery cell manufacturers, on the other hand, held 173.4 GWh of finished battery inventory. Specially, the cumulative ternary battery inventory dropped to the annual low at 24.9 GWh, while LFP battery inventory further piled up, though the growth narrowed due to falling production and improving sales compared with September.

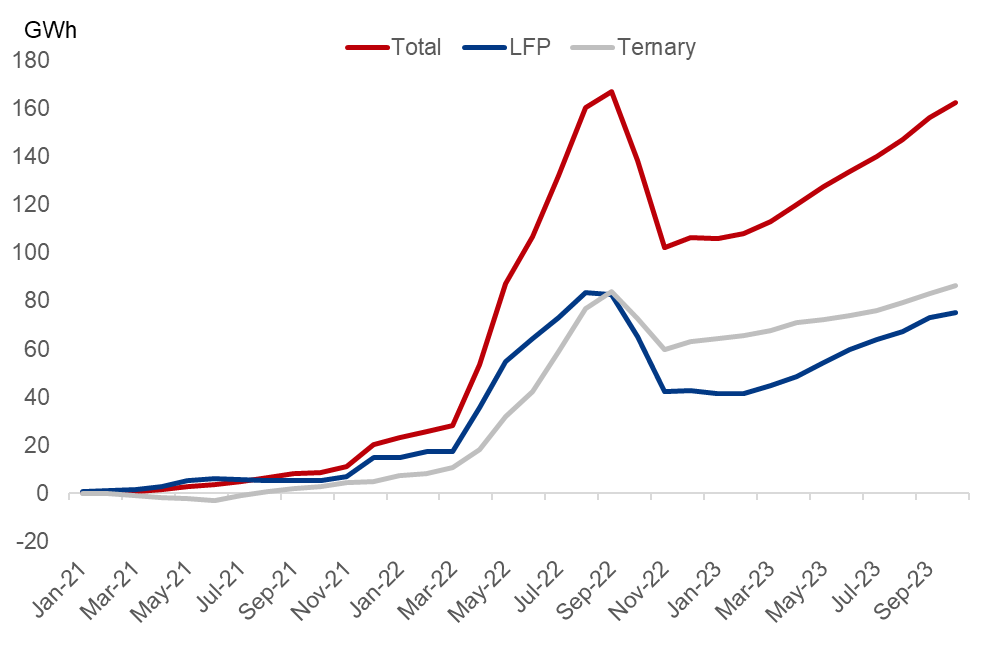

The downstream consumers' combined power battery inventory was 162.4 GWh, including 75.3 GWh LFP battery and 86.6 GWh ternary battery.

Figure 1-7. Battery Cell Factories In-plant Inventory

Figure 1-8. Downstream Consumers Battery Inventory

Sources: China Automotive Power Battery Industry Innovation Alliance, Mysteel

The inventory of both battery cell factories and downstream consumers piled up further, but the inventory of ternary battery dropped slightly as the sales volume slightly outnumbered the production amid sagging demand.

Looking ahead over November, the sales volume of EVs is estimated to jump boosted by the double 11 shopping festival. When the production is likely to be flat, the inventory-to-sales ratio will rise.

The production of LFP and ternary cathode active materials is projected to fall 0.96% and 0.44% respectively MoM in November based on available production scheduling. The falling LFP production is attributed to slowing demand in the energy storage sector.

On the inventory end, the smelters' lithium carbonate inventory recorded 19,600 tonnes as of end-October, and is likely to rise 14% MoM at 22,400 t in November, with the planned lithium carbonate production rising 7.6% MoM in November, and net imports likely to rise 76%.

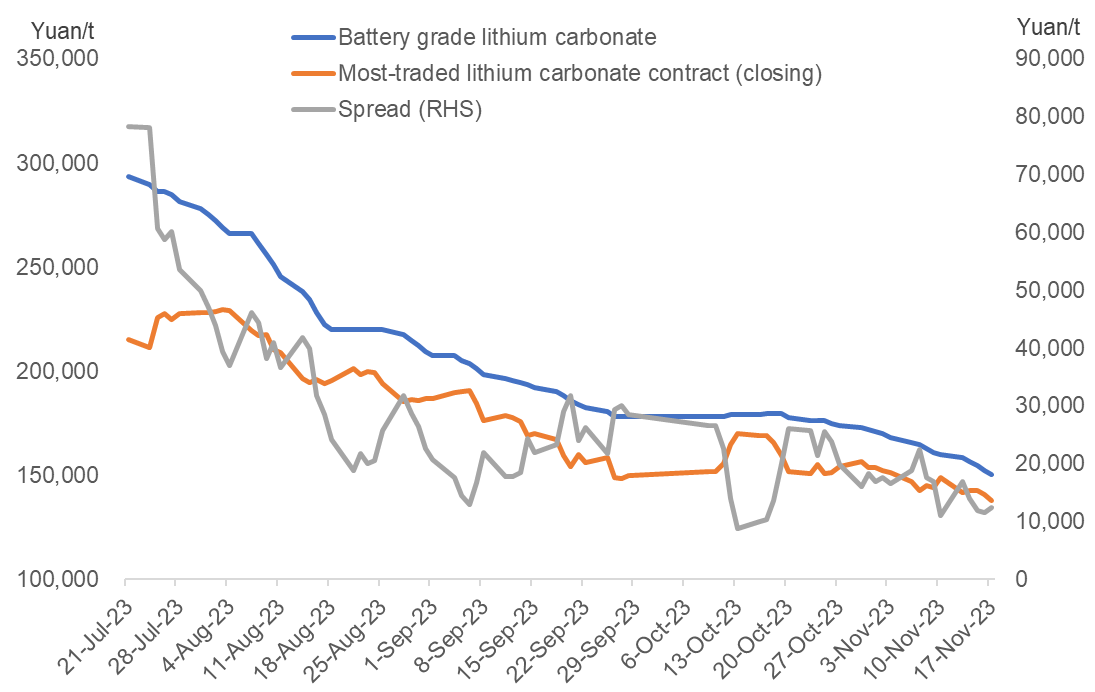

Another prominent feature is that the lithium carbonate spot-features spread has been wide at present. And there are generally two major influencing factors.

Figure 1-9. Lithium Carbonate Spot-Futures Spread

Source: Mysteel

The first is the current price level versus the cost level of new supplies. Mysteel believes that the lithium carbonate prices are poised to fall further with the supply ramping up and lithium mines adopting "M+1" pricing method, on the premise of aggravating oversupply in the long run. In this case, capacities with high cost will phase out amid oversupply, thus brining down the cost level.

The second is the strategy of futures market players. Will the closing of short positions trigger a rebound in futures prices? Will the registration of warrants hurt the circulation of spots?

On the backdrop of over 10,000 lots of open interest for near-month contract, the key lies in who will leave first when the speculators are highly likely to close the positions approaching the delivery date in December. On the spot market, the lithium carbonate prices are unlikely to rebound significantly should the demand fail to beat the expectations. Moreover, some traders which hold both spots and futures contracts settle the transactions using intraday futures prices. Therefore, the spot-futures spread will narrow approaching the delivery of front-month futures contract.

In summary, the lithium carbonate prices are likely to remain low until the emergence of two pivots.

The first is when the lithium salt smelters are unable to deliver long-term orders as they reduce the production constantly amidst falling lithium carbonate prices. The second is when the downstream demand picks up substantially and the consumers start to stockpile.

The port arrivals of lithium carbonate imports and the capacity utilization rates of smelters are worth attention.

Written by Aggie Hu, huchenying@mysteel.com