Lithium carbonate prices up with supply cuts, despite slow demand

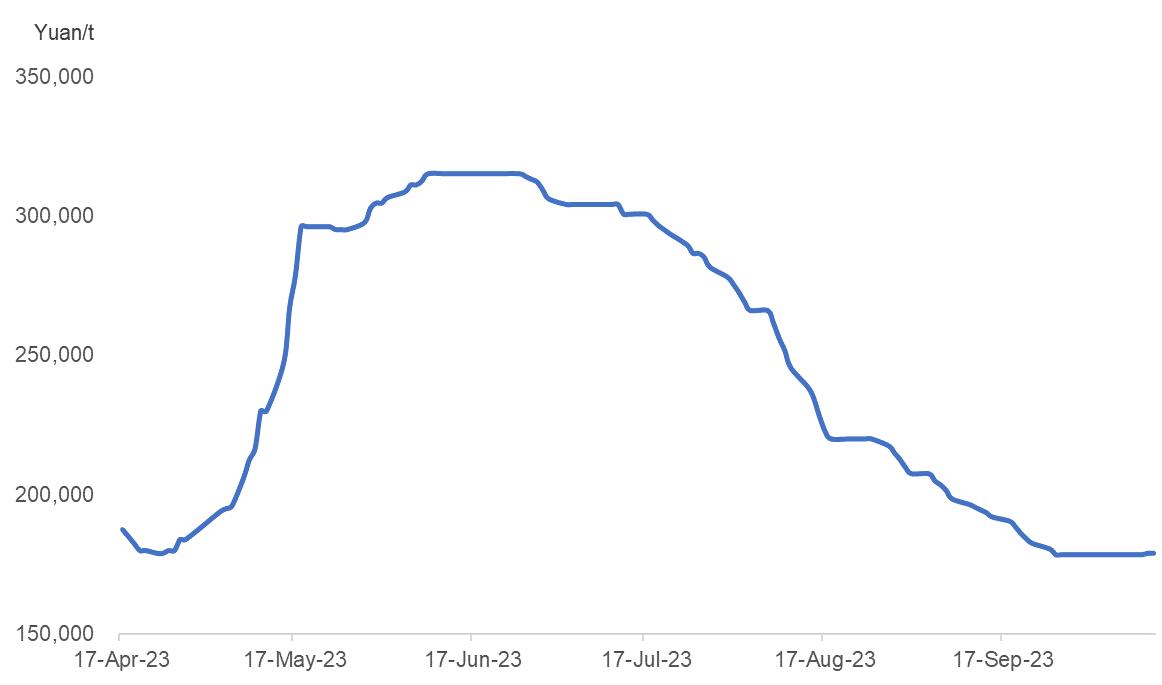

The market prices of battery grade lithium carbonate, which dropped from near-term high at Yuan 315,000/tonne around end-June to Yuan 173,500/t on October 11, have been falling since the last extensive stockpiling by battery manufacturers in June, per Mysteel tracking.

Nevertheless, the prices embarked on its first rebound post the National Day holiday. The fundamental drives still lie in the supply and demand balance.

Figure 1-1. China Battery Grade Lithium Carbonate Market Price

Source: Mysteel

I. Demand

New energy vehicle (NEV)

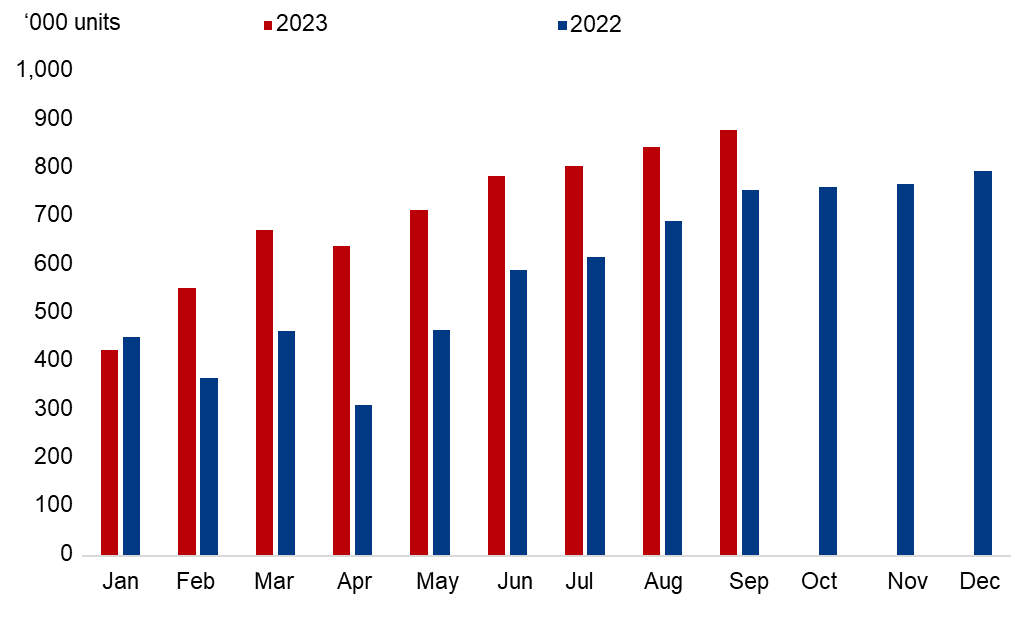

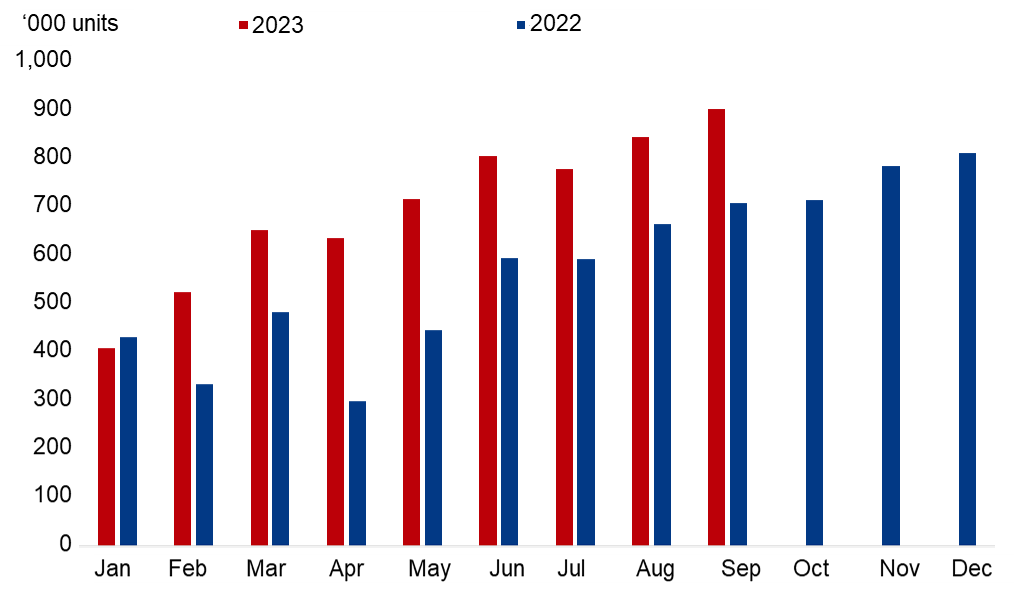

According to China Association of Automobile Manufacturers (CAAM), China's NEVs production and sales were 879,000 units and 904,000 units respectively in September, marking a monthly growth of 4.3% and 6.9%, against an annual gain of 16.4% and 27.7% respectively.

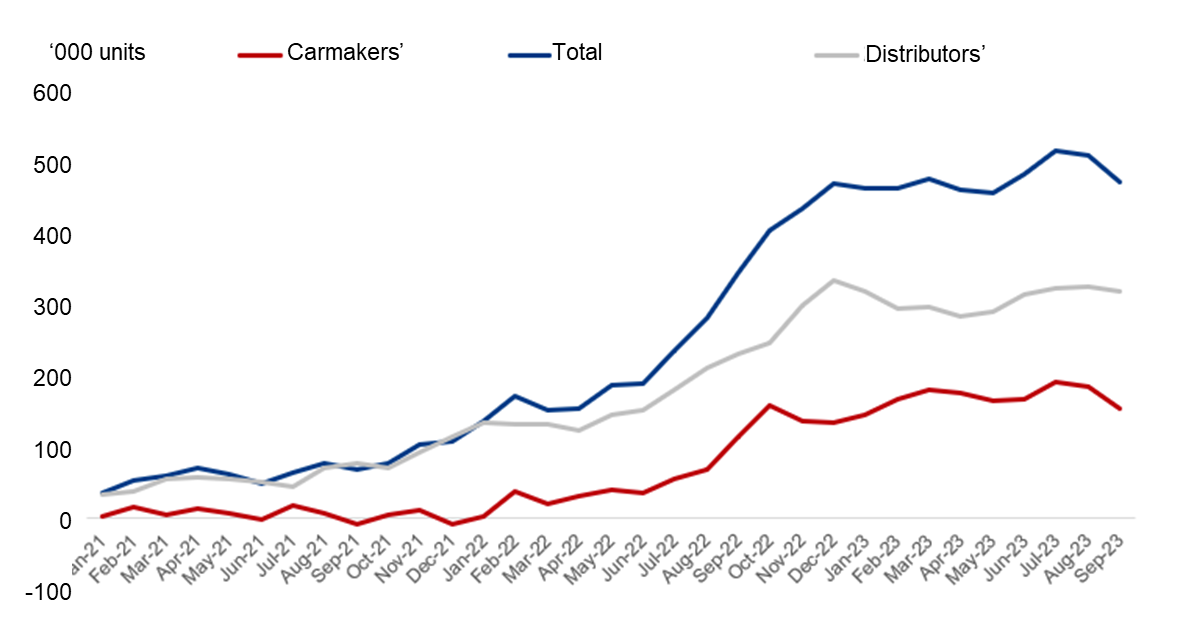

The NEVs sales performance was outstanding through September, resulting a fall in NEVs inventory, with carmakers' in-plant inventory falling 31,000 units at 155,000 units, and distributors' inventory dropping 7,000 units at 319,000 units.

Figure 1-2. China NEVs Production

Figure 1-3. China NEVs Sales Volume

Sources: CAAM, Mysteel

Taking carmaker's in-plant inventory and the distributors' inventory together, China's NEVs inventory declined around 25,000 units in September, evidencing resilient downstream consumption through the carmakers were generally cautious towards the end-market.

Figure 1-4. China NEVs Inventory

Source: Mysteel

Power battery

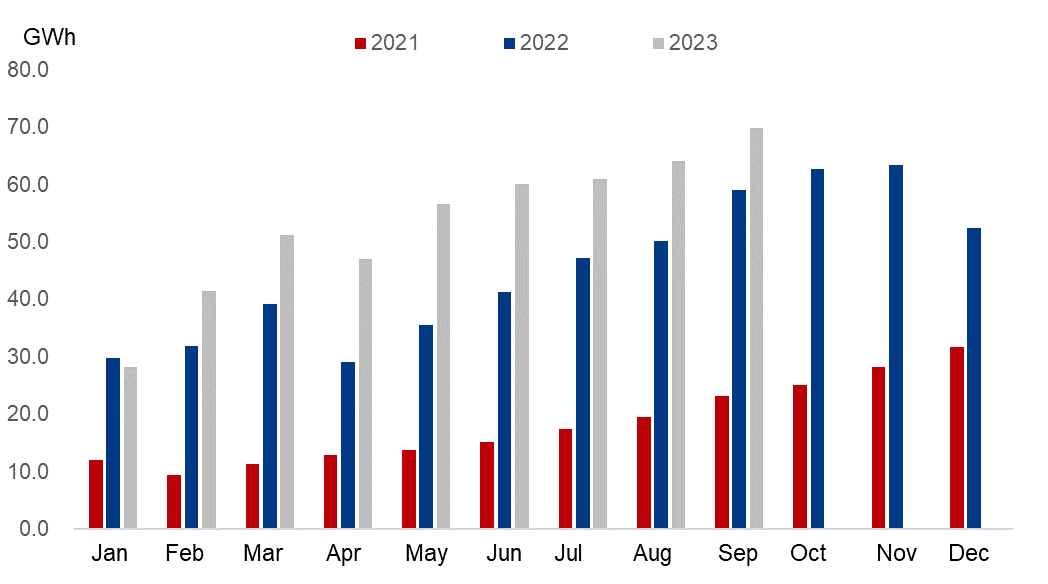

China's power battery production registered a monthly increase of 8.8% and an annual growth of 18.3% at 69.9 GWh in September, including 23 GWh ternary power battery and 46.9 GWh LFP power battery, rising 12.8% and 7% month on month (MoM) respectively, and -5.2% and 34.7% year on year (YoY).

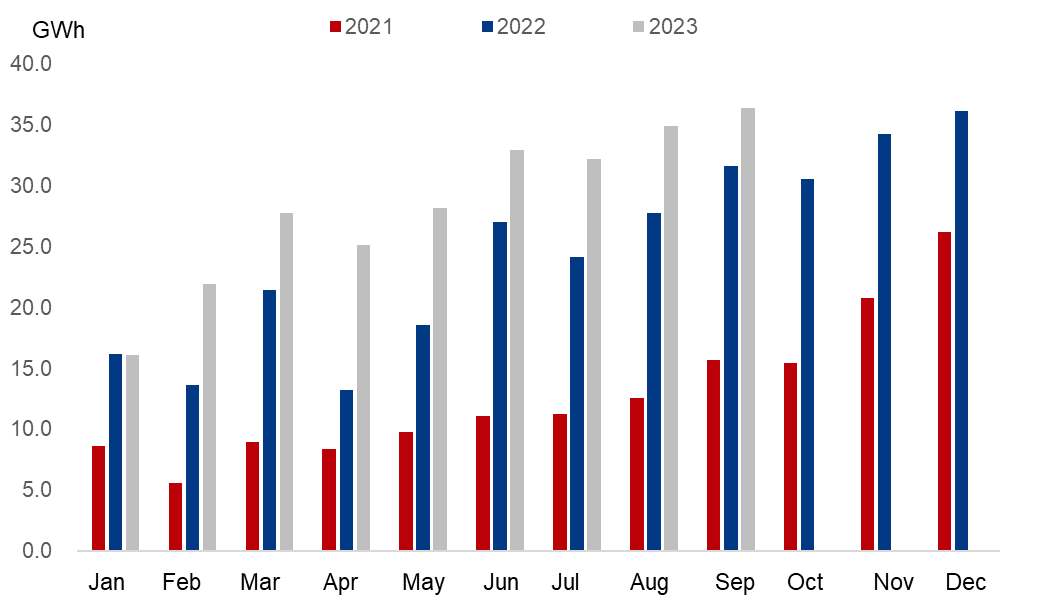

The installed capacity of ternary and LFP power battery was 12.2 GWh and 24.2 GWh respectively in September, up 13% and 0.4% MoM respectively, and 8.9% and 18.6% YoY.

Figure 1-5. China Power Battery Production

Figure 1-6. China Power Battery Installed Capacity

Sources: China Automotive Power Battery Industry Innovation Alliance, Mysteel

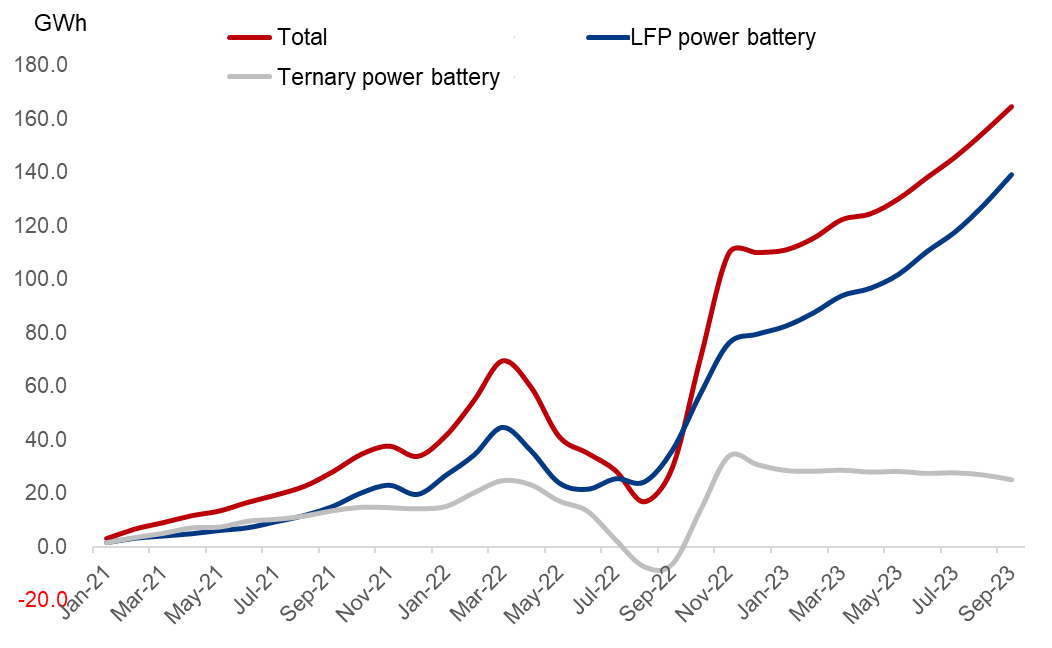

The battery manufacturers' in-plant power battery inventory was still on the rise, which recorded 164.5 GWh by end-September, including 73.5 GWh LFP power battery and 82.9 GWh ternary power battery, as a result of over optimism among battery manufacturers towards September demand, which actively ramped up the production. Meanwhile, the carmakers were still cautious towards the end-market, hence did not place large orders for power batteries.

Specially, the inventory of ternary power battery dropped thanks to robust sales growth.

Figure 1-7. China Power Battery In-plant Inventory

Source: Mysteel

Battery raw materials

The production of LFP cathode materials reported 152,00 t in September, up 1.07% from August. But the production scheduling dropped 3% MoM in October per Mysteel survey. The production of ternary cathode materials lost 2.5% MoM at 53,900 t in September, with the production secluding falling 7.4% MoM in October.

The production of lithium carbonate is expected at 53,700 t in October based on the available production scheduling of cathode materials.

Contrary to the robust production growth of power batteries in September, the production of cathode materials was rather slow probably because the material factories focused on destocking at present on cautiousness over follow-up market.

II. Supply

Lithium carbonate supply is estimated to tighten in October for a combination of causes.

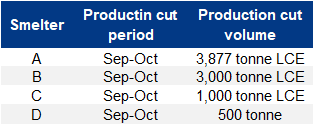

First, domestic lithium carbonate smelters in Xinjiang, Sichuan, and Jiangxi Province have been reducing the production or take tolling orders to control the cost on high lithium ore prices, especially when cheap African lithium ore is not available at present, while Australian ore prices remain high.

Specially, the smelters in Jiangxi Province are further restricted on environmental protection inspections.

The smelters in Qinghai Province are projected to lower the production seasonally by around 30% in October when the temperature becomes unfriendly to production, though the production cost is favorable, per Mysteel investigation.

Taken together, China's lithium carbonate production is projected to be 34,000 t in October.

Table 1-1. Production Cuts of Major Lithium Carbonate Smelters

Source: Mysteel

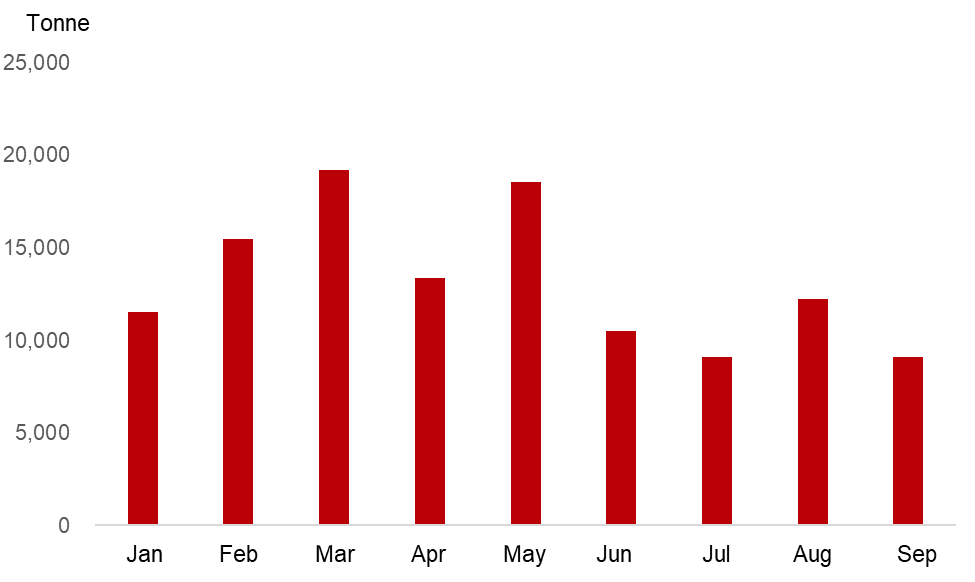

Meanwhile, China's lithium carbonate imports have been falling as well, mainly due to less supply from, Chile. While overseas lithium carbonate prices were firm at Yuan 230,000-240,000/t, lower domestic prices did not appeal the importers.

Figure 1-8. Lithium Carbonate Exports of Chile

Source: Chile Customs, Mysteel

III. Summary

Generally, though the demand growth is slow, the falling supply in China and from overseas has laid the ground for lithium carbonate price hike.

But it is worth noting that a large smelter looks set to release a large batch of lithium carbonate around end-October, which will probably cast great influence on lithium carbonate prices.

And when spot lithium carbonate prices rise to the expectation of the suppliers, the supply will rise.

Mysteel predicts that spot lithium carbonate prices will rebound to Yuan 180,000-190,000/t shortly in October.

Written by Aggie Hu, huchenying@mysteel.com