Nickel prices are expected to remain pressured in the fourth quarter of 2023 as the bears are more resilient on the backdrop of production growth in Indonesia.

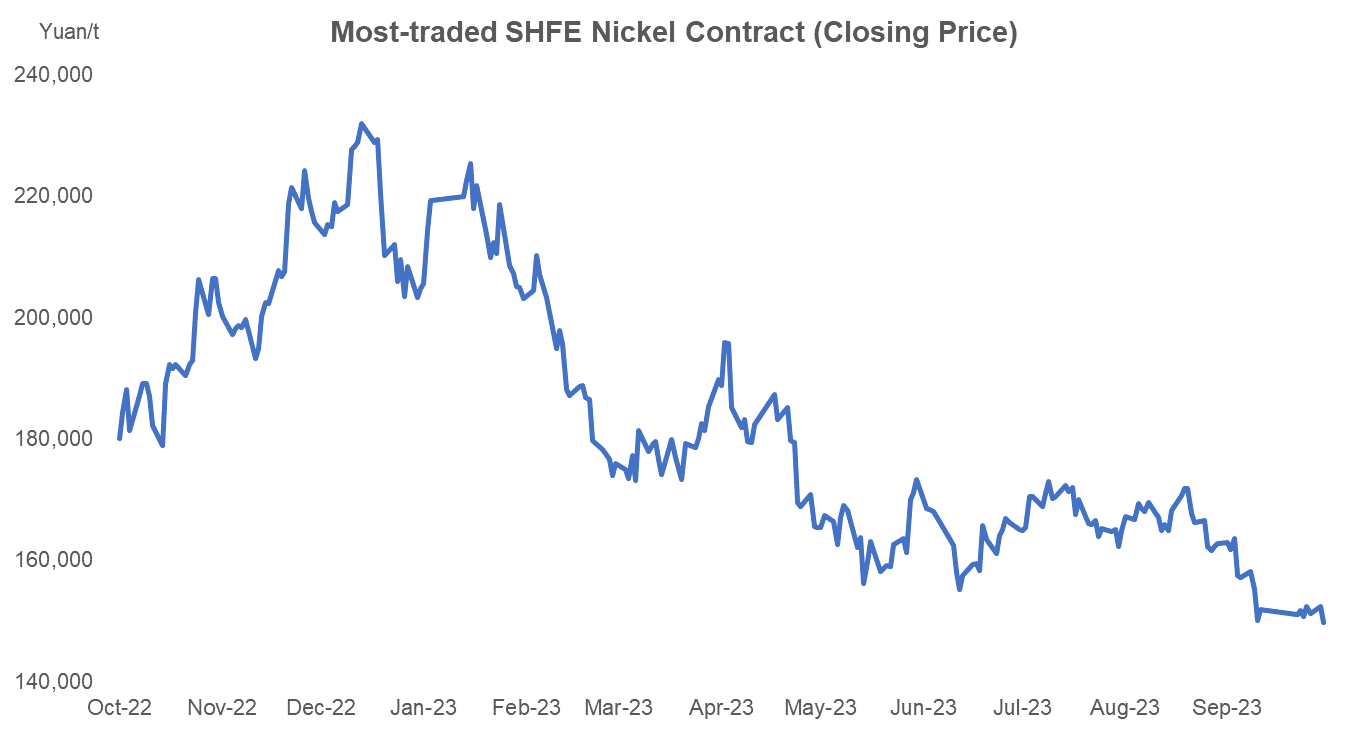

SHFE nickel saw its bull sector end on September 7 and started to fall before hitting the near-term low at Yuan 145,760/tonne on October 12. The prices then stabilized at around Yuan 150,000/t.

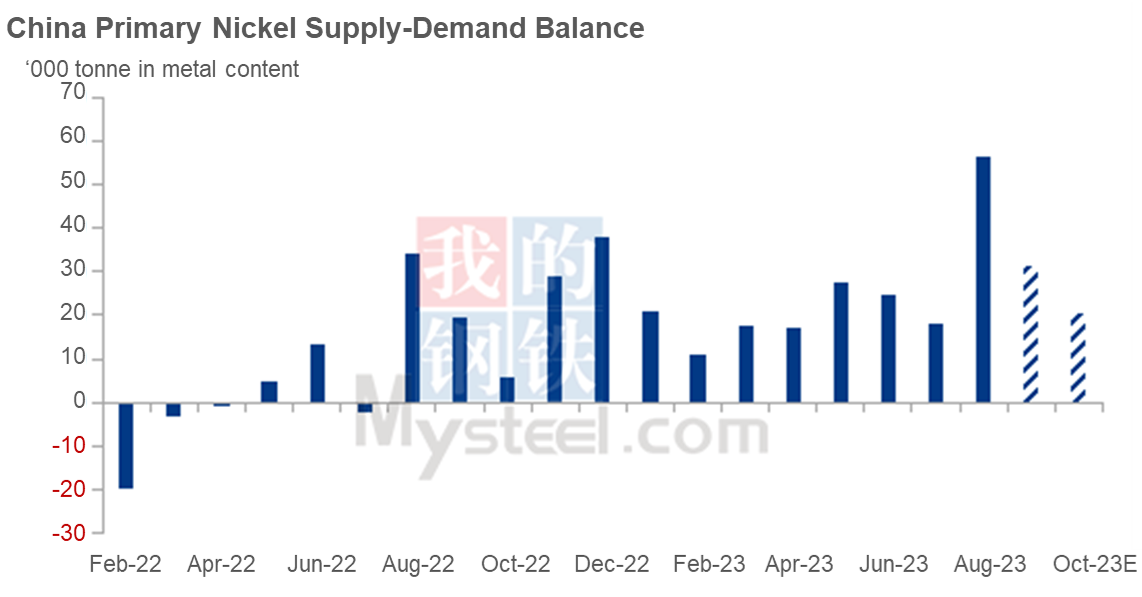

Source: Mysteel

Generally, the bears and bulls centering SHFE nickel have not changed much since the anti-corruption investigation was initiated towards the mining sector in Indonesia in August.

On the bull side, rising nickel ore prices following the anti-corruption investigation have pushed up the cost of a series of downstream products including NPI, MHP, and nickel sulfate. And strong US dollar also sustained China's import cost at a high level, supporting nickel prices.

For bears, the situation of overcapacity across the industry chain, combined with flat end-market demand, has capped nickel prices, which resulted in mounting nickel inventory on the backdrop of poor nickel sulfate demand from the battery sector.

Moreover, with the gradual settlement of Indonesia's anti-corruption investigation, the bears became even stronger.

The question now lies in whether nickel prices have hit the floor.

It is widely believed that producing electrowinning nickel using outsourced nickel sulfate is with a breakeven point of Yuan 150,000/t, around which SHFE nickel now hovers, while that for producing electrowinning nickel using outsourced MHP is Yuan 140,000/t, which is more like the bottom for SHFE nickel as few smelters in China use nickel sulfate as the raw material.

And it we go back to the fundamentals, the bull side lacks new engines though nickel ore prices are still high in Indonesia.

On the bear side, China's refined nickel supply is still on the rise, which is an increasingly favored alternative to imported nickel. In addition, with Indonesia's MHP flowing back to China, the refined nickel cost will drop further. In addition, the downstream demand weakens as the stainless steel mills have initiated a production cut on thinning profits. And the ternary material sector is unlikely to rebound, reducing the demand for nickel sulfate.

Source: Mysteel

Taken together, the bear side is more resilient at present, potentially weighing on nickel prices in the rest of 2023. But it remains to be seen if SHFE nickel falls below Yuan 150,000/t.

Written by Aggie Hu, huchenying@mysteel.com