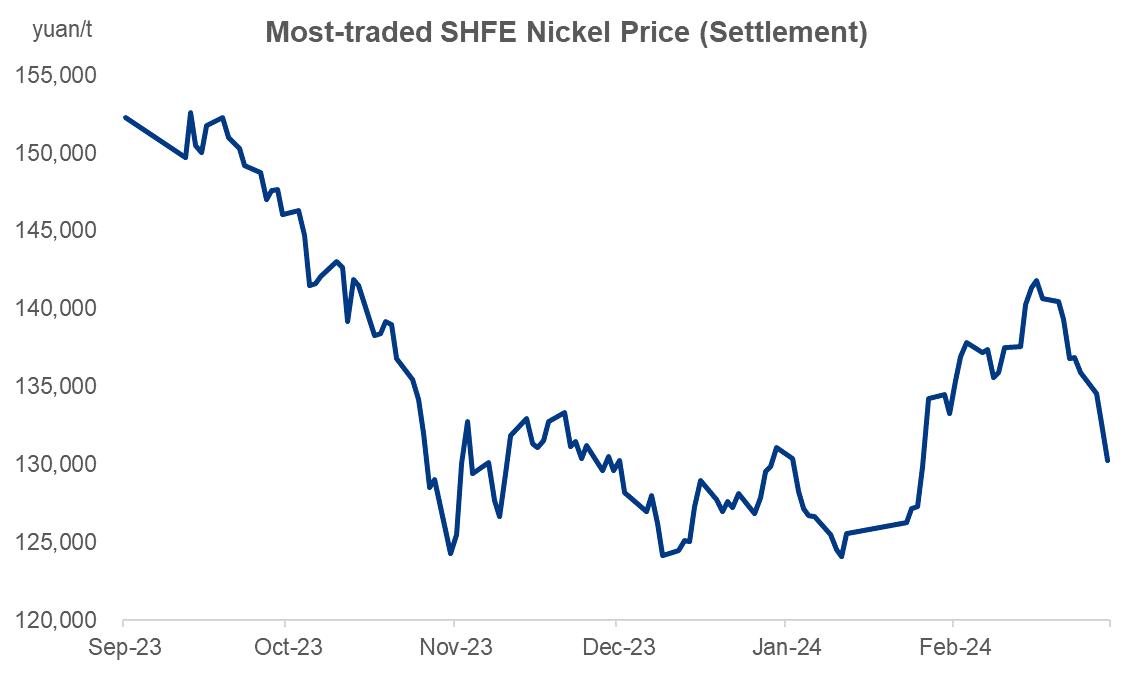

The most-traded SHFE nickel price has been on the downward track after hitting a near-term high of above Yuan 140,000/tonne on March 14, primarily because the contract was overvalued by strong expectations that the supply would keep rising on lucrative profits. Nevertheless, the slow recovery of the end-market demand put a cap on the momentum.

Source: SHFE

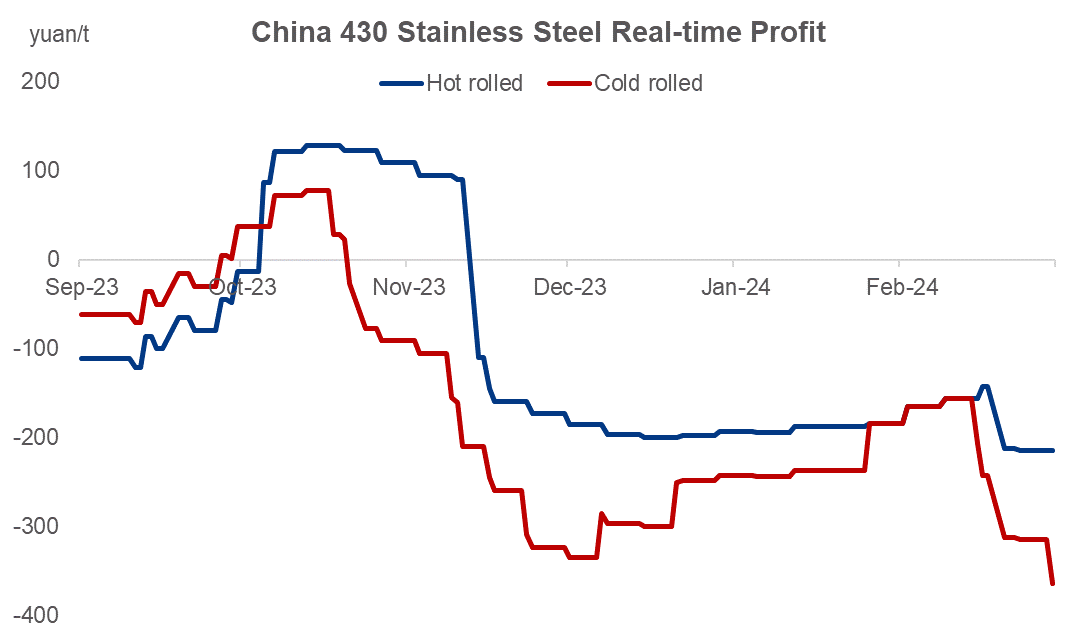

First of all, it is widely believed that some stainless steel mills will curtail the production in April for serious losses, and more mills are expected to join in May, leading to less demand for nickel raw materials.

Source: Mysteel

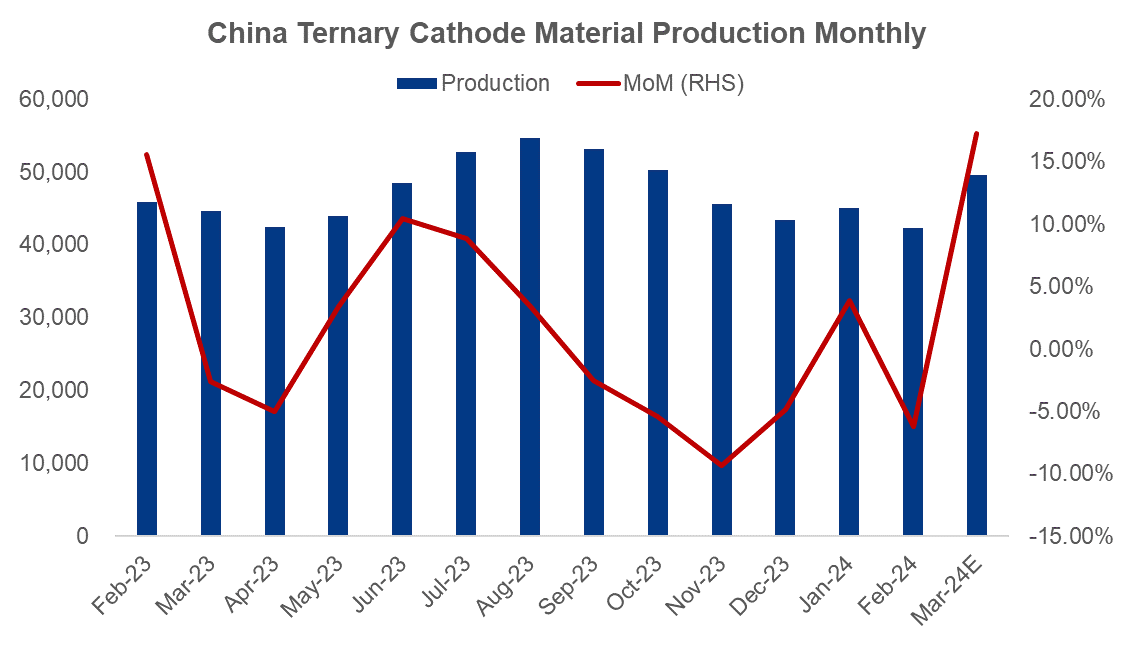

Concerning the power battery sector, though the top-tier ternary battery cell plants have ramped up the production scheduling in March, the growth was basically flat over that in 2023. And the intensive competition among the ternary precursor suppliers caused further losses to themselves, except for the integrated ones with certain cost advantages.

Source: Mysteel

Currently, the nickel sulfate price hike was prompted by the firm cost support when the spot supply of MHP remained tight. Since more nickel mines in Indonesia have passed the RKAB approval, the nickel raw materials supply is projected to rebound, potentially weighing on the prices.

According to Mysteel refined nickel cost model, the cash cost of laterite nickel ore - nickel matte - refined nickel integrated nickel smelters was around Yuan 120,000/tonne, which was an extensively recognized marginal cost support by the market players.

Nevertheless, the slowly recovering power battery production and firming NPI cost support in Indonesia are projected to lift the nickel price support to around Yuan 125,000/tonne.

Written by Aggie Hu, huchenying@mysteel.com