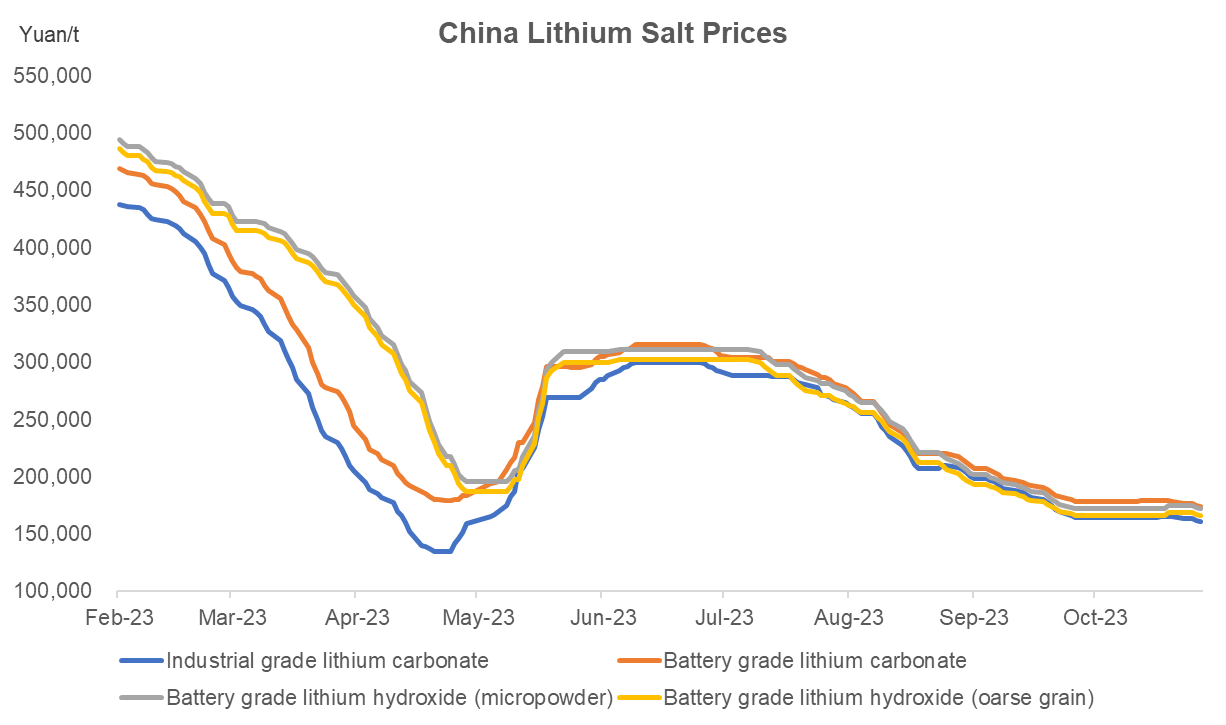

China's lithium carbonate market failed the traditional seasonal high in September and October, and kept falling except for a short rally in early October. The prices are expected to stabilize in November when the cathode active material factories start to stockpile.

On the spot market, the lithium carbonate smelters mostly quoted Yuan 180,000/tonne due to high cost, but the traders' offers were around Yuan 160,000-165,000/t.

Source: Mysteel

On the raw material front, China's spodumene imports recorded 499,000 tonnes in September, an increase of 93.2% from August, according to the General Administration of Customs of the People's Republic of China (GACC) and Mysteel calculation.

Among them, the imports from Australia took up 80% of China's total imports, or 45,000-50,000 tonnes LCE, an increase of 131% compared with August. The significant monthly growth was primarily due to port maintenance-induced shipment delay.

The average import price of Australia spodumene was $3,252/t, and the cost of producing lithium carbonate with Australia spodumene purchased in the spot market was approximately Yuan 250,000/t, meaning that the salt smelters suffered significant losses at present.

The September imports will power the production in October or November, hence the Australia spodumene inventory is projected to remain relatively high in October.

The imports from Africa rose 17% month on month (MoM) at around 100,000 t in September, but most of which were DSO (direct shipping ore), leading to low LCE amount. Nevertheless, the low prices, which averaged $1,447/t in September, allowed relatively high profits of smelters.

The inventory of Africa spodumene is expected to be consumed quickly due to low grade, but the ore supply has been ramping up following the end of rainy season in the country.

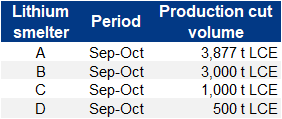

On the supply side, China's lithium carbonate production is estimated to fall 8,500 t in October according to the smelters' production cut announcements. But it is worth mentioning that most smelters in Jiangxi and Sichuan Province have resumed the production by end-October.

Meanwhile, China's lithium carbonate imports from Chile, a major supplier, are likely to fall in October trailing the export cuts in Chile in September.

Taken together, China's lithium carbonate supply is estimated at 42,000 t in October.

Table 1-1. China Smelters Production Cuts

Source: Mysteel

Regarding lithium carbonate inventory, the smelters in Qinghai each held around 1,000 t lithium carbonate inventory. Those with sufficient supply would destock regularly on the 25th of each month, while others carried out maintenance for lack of resources.

Elsewhere, a large smelter in Sichuan held 5,000 t lithium carbonate and 300,000 t Australia spodumene concentrate but was not planning to sell because the lithium carbonate spot prices were low.

Generally, the smelters' lithium carbonate inventory was low, hence was rather firm to the prices.

The consumption of lithium carbonate is estimated at 54,000 t in September, down slightly 0.6% from August. The demand is likely to stay flat in October despite minimal decreases.

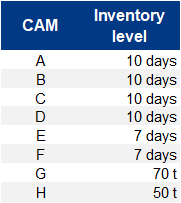

At present, the downstream players' lithium carbonate inventory was also low, with LFP cathode material factories holding 7-10 days of lithium carbonate inventory on average. The finished products inventory of material factories were 15-30 days.

Table 1-2. Cathode Material Factories' Lithium Carbonate Inventory

Source: Mysteel

In summary, the spot supply of lithium carbonate has started to tighten with smelters reducing the production on losses and keeping the in-plant inventory low. While the cathode material factories report low raw material and finished products inventory, the demand for lithium carbonate may pick up when the battery cell manufacturers demand the material factories to deliver the orders.

It is expected that lithium carbonate prices would stabilize between Yuan 165,000-175,000/t with material factories stockpiling in November.

Written by Aggie Hu, huchenying@mysteel.com