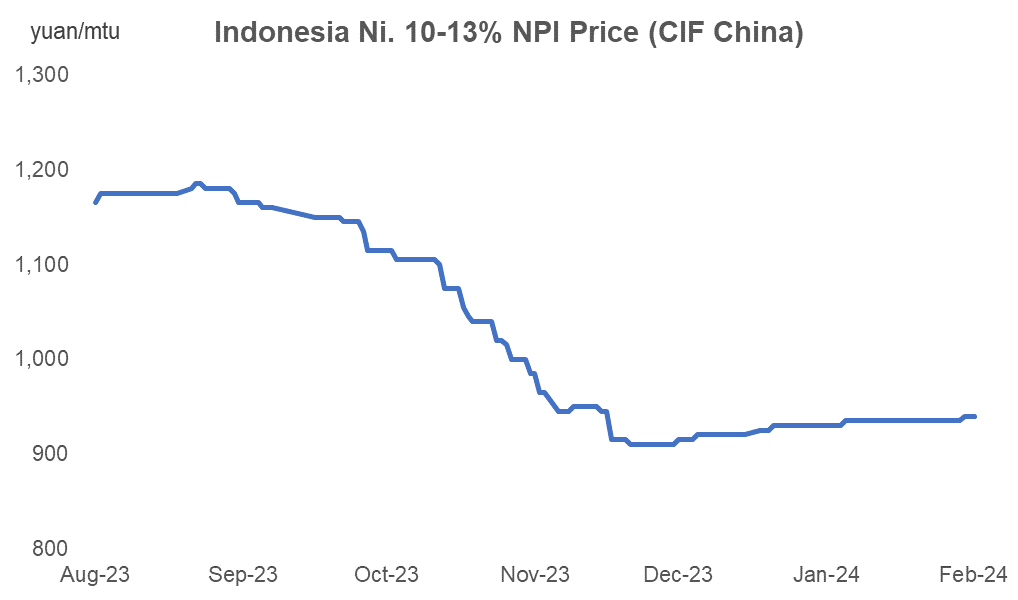

China's NPI prices have been on the rise since December 2023 fueled by the persistent RKAB approval disruption, and the latest market quotations have reached Yuan 960/mtu, though there have not been transactions at such a price level.

Source: Mysteel

As of the time of this writing, around 23 nickel mining spots have received the RKAB approval, a certificate compulsory to carry out normal mining activities in Indonesia, with over 250 spots waiting indefinitely based on historical data.

It is expected that the approval will return to normal after the newly elected Indonesia President is officially announced in the second half of March.

Though most Indonesia's NPI smelters have built nickel ore stocks as early as in November-December 2023 that were able to support the production in the first quarter of 2024, some small smelters have already reported nickel ore supply shortage and delaying shipment, weighing on the market sentiment.

In addition, some operating NPI projects in Indonesia reduced the production due to depleting nickel ore inventory with a curtailment of 5-20%, except for the newly commissioned projects.

Nevertheless, China's NPI market is projected to remain oversupplied with a surplus of roughly 10,000 tonnes in Ni. content.

In detail, China's 300-series stainless steel production is estimated to be down to around 1.4 million tonnes in February as a result of intensive maintenance. In addition, the stainless steel inventory held by 89 warehouses jumped 19.34% week on week at 1.17 million tonnes as of February 19, including 742,900 tonnes 300-series stainless steel.

As such, the mainstream steel mills' bids were mostly between yuan 940-950/mtu, lower than the sellers' quotations at around yuan 960/mtu.

The follow-up market is still subject to Indonesia's RKAB approval situation.

Written by Aggie Hu, huchenying@mysteel.com