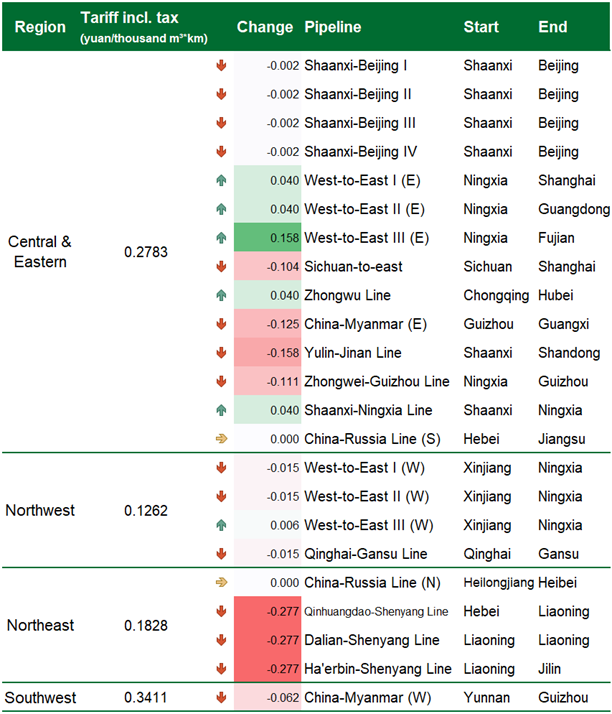

China will implement new transmission tariffs for its gas pipeline network from January 1, 2024. This marks the first time, since China's oil and gas network reform, that the transmission tariffs for cross-provincial gas pipelines are regionally formulated. The number of tariffs is reduced from 20 by pipelines (companies) to just four by regions. The revised tariffs will see most pipeline charges decreasing, with reductions ranging from 0.002 to 0.277 yuan/thousand m3*km. Northeast China will benefit from the steepest tariff cuts.

Previously, the National Development and Reform Commission (NDRC) has divided the cross-provincial gas pipelines operated by PipeChina into four pricing regions – Northwest, Southwest, Northeast, and Central-East – based on key pipeline nodes. Provincial trunk pipelines, branch lines and interconnectors within the region are all subjected to a unified pricing benchmark, facilitating the network interconnectivity and eliminating the previous disputes due to varying local pricing.

Among the four pricing regions, the transmission tariffs for Southwest China are the highest, followed by Central-East China and Northwest China. Subsequent new pipelines and cross-provincial pipelines operated by other entities will follow the benchmark prices within these regions. That means newly built pipelines will no longer have a specific trial tariff during the initial period.

Cross-provincial Gas Pipeline Transmission Tariff

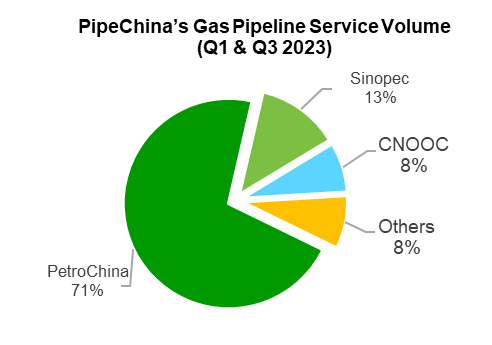

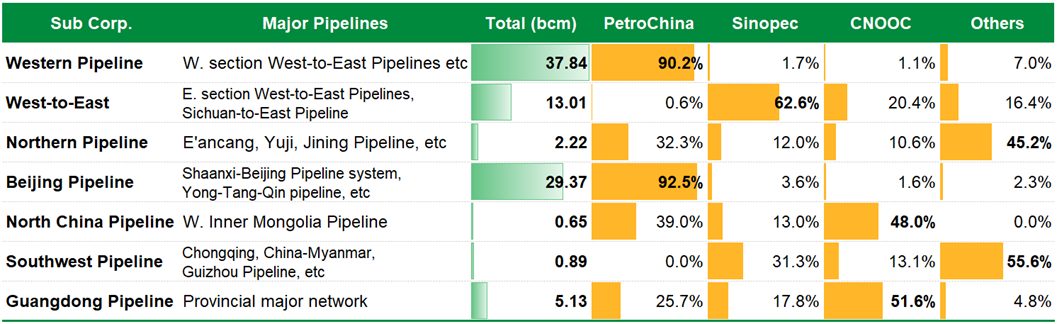

China's three state-owned major oil companies are still main users of the gas transmission service. In particular, the west section of the West-to-east and Shaanxi-Beijing Pipeline systems mainly connect PetroChina's gas fields and imported sources, resulting in high transmission volumes and proportions. However, in the northern pipeline regions and the east section of the West-to-east Pipeline system, where the downstream markets are more active and the interconnection network is well developed, the service volume for companies other than the three majors has begun to take on a significant size.

Source: PipeChina, GL Consulting

In accordance with oil and gas network reform requirements, pipeline infrastructure will be made available to third-party market entities on a fair basis, separating transmission from sales. Future pipelines will take into greater account the distribution of end markets and diversification of resources, allowing more market entities to participate.

Shares of PipeChina's Gas Pipeline Service Volume (Q1 & Q3 2023)

Source: PipeChina, GL Consulting

Written by the GL Consulting team (Mysteel's consultancy arm on energy transition)

To get detailed full text, send an email to glconsulting@mysteel.com

Edited by Navy Liu: liuchuanjun@mysteel.com