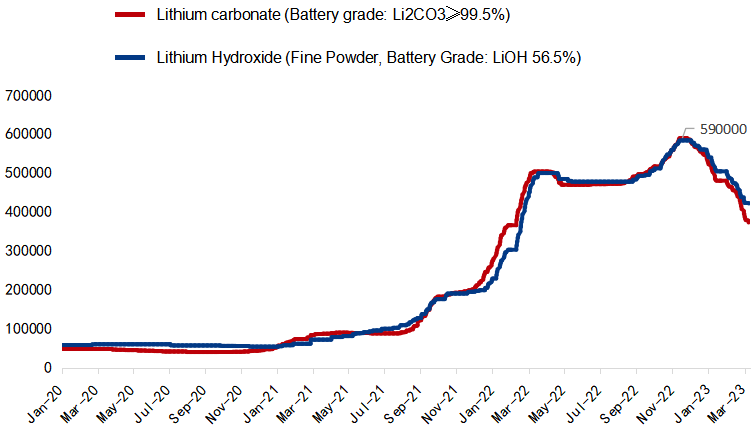

Chinese prices of battery-grade lithium carbonate have dropped to Yuan 362,000/tonne as of March 10, down by a large 38.64% after peaking at Yuan 590,000/tonne in late November last year; while the average price of battery-grade lithium hydroxide also slumped 29.11% from its peak of Yuan 584,000 to settle at Yuan 414,000/t by the same day.

Compared to lithium carbonate, the retail prices of lithium hydroxide are less affected by market mood swings and the price changes in lithium hydroxide offers are also smaller, mainly because lithium hydroxide factories could secure more long-term orders from downstream plants. But the price difference between the two types of lithium-based compounds may not be significant as they can be made into each other.

Figure 1-1: Price trend of lithium carbonate and lithium hydroxide in China (Unit: Yuan/tonne)

Source: Mysteel

In its earlier weekly report Have Lithium Prices Hit the Peak posted on November 25 last year, Mysteel New Energy Research Center clearly stated that the lithium compound prices were near the inflection point, and the price of lithium carbonate could peak at Yuan 600,000/t, indicating potential risks of price declines. Another weekly report China's Lithium Prices to Remain Weak until February 2023 on December 23 2022 predicted that the price of battery-grade lithium carbonate may drop to Yuan 430,000/tonne by the end of February this year. However, this price prediction has been revised to Yuan 400,000/tonne afterward due to the impact of the lithium rebate program proposed by CATL, the world's largest electric vehicle battery maker.

According to the same analytical framework, this report will further discuss at what level the lithium carbonate price will stabilize in the future based on the data from Mysteel's New Energy Business Unit.

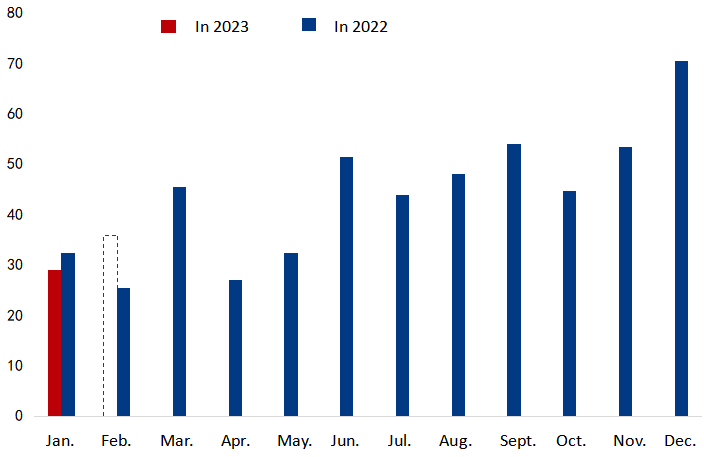

First, the current decline in lithium carbonate prices is mainly driven by the slowdown of end-users' demand for new energy vehicles (NEVs). In January, there were only 291,000 NEVs insured (a key indicator for China NEV sales) in China, posting a negative year-on-year growth rate of 10.19% - a surprisingly low result as compared with the average year-on-year growth of 80.31% for the whole of 2022, mainly due to the absence of fierce scramble for car assembly last December, the widely circulating COVID infections over the end of last year to the beginning of this year as well as the impact of the Chinese New Year (CNY) holiday break in this January. Besides, the cumulative insured NEVs in January-February only grew 12.6% year on year, when the impact of the Chinese New Year holiday was removed, raising concerns among market participants about whether China's new energy vehicle (NEV) market could maintain a fast growth when the country has phased out the subsidies for NEV purchases and its NEV penetration rate is approaching 30%.

Figure 1-2: New energy passenger vehicle sales in China (Unit: '0000 units)

Source: Mysteel

Given the pessimistic outlook in the downstream market, the total output of power batteries in January-February only rose by 13.33% year on year, while the production of cathode materials also logged a moderate year-on-year growth of 16.2%.

Table 1-1: The output of power batteries and cathode materials in China (Unit: GWh; '0000 tonnes)

|

Year |

Jan. |

Feb. |

Jan.-Feb. |

|

|

Power battery (GWh) |

2023 |

28.2 |

41.5 |

69.7 |

|

2022 |

29.7 |

31.8 |

61.5 |

|

|

YoY |

-5.05% |

30.50% |

13.33% |

|

|

Cathode material ('0000 tonnes) |

2023 |

10.0 |

12. 2 |

22. 2 |

|

2022 |

9.9 |

9.79 |

19.1 |

|

|

YoY |

1.03% |

24.6% |

16. 2% |

Source: Mysteel

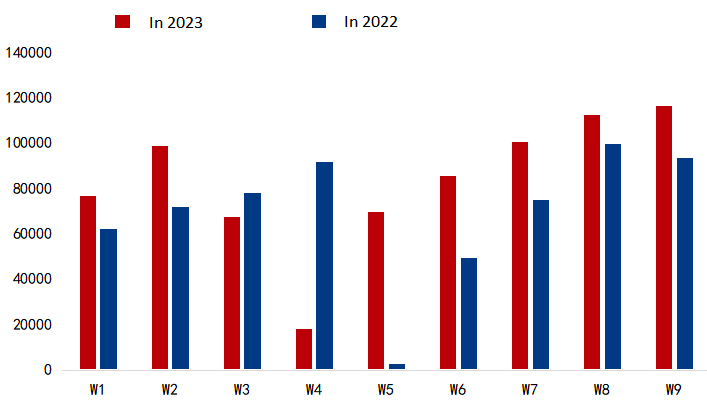

However, according to the compulsory traffic insurance data, the volume of insured NEVs in China has maintained a week-on-week rising trend from February, mostly due to the fact that Tesla and other automakers had cut their prices to promote sales. The data also proved that automakers could still boost sales via price cuts after NEV subsidies ended in China. In addition, automakers are likely to offer some discounts to customers after the decline in lithium carbonate prices. Therefore, the volume of insured NEVs in China is anticipated to rise 10% year on year and 38% month on month to reach 480,000-500,000 units in March, which may drive the power battery output up by 15% month on month to 48 GWh. Also, the output of cathode materials is expected to increase by 8.8% month on month to 131,600 tonnes, based on the production schedule data compiled by Mysteel New Energy Business Unit.

Figure 1-3: China's insured NEV passenger vehicles based on collected data of compulsory traffic insurance by week (Unit: unit)

Sources: Compulsory traffic insurance and Mysteel

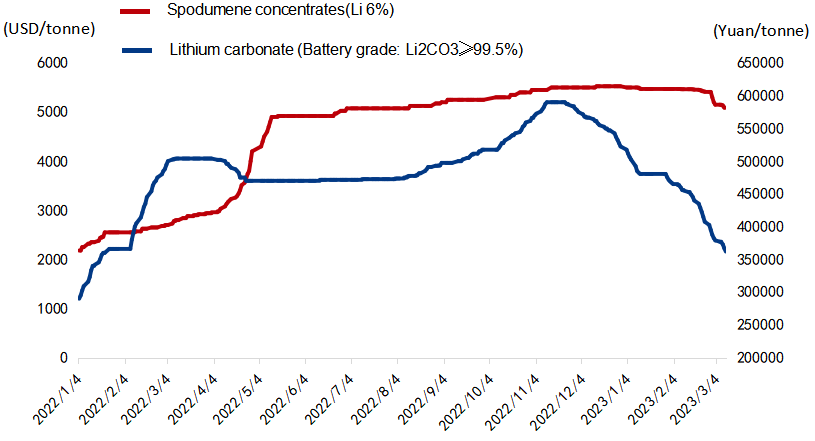

Along with the sharp drop in domestic lithium carbonate prices, the prices of lithium compounds fell much faster and steeper than those of lithium concentrate (CIF, grade 6%). When the lithium concentrate price stands at $5,070/tonne, lithium compound plants' costs on producing lithium carbonate by using outsourced lithium ore are Yuan 323,000/tonne, including material costs of soda ash, sulfuric acid, electricity and thermal coal in, as well as costs of depreciation, labor and processing.

Figure 1-4: Price gap between lithium carbonate and lithium concentrate

Source: Mysteel

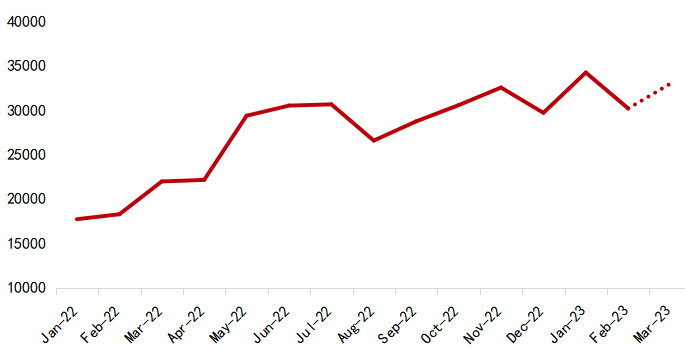

According to the data, the output of lithium carbonate totaled 34,200 tonnes and the overall operating rate was 61.4% in January 2023. Despite a significant month-on-month decrease in production among battery plants and cathode producers in January, the operating rate of lithium carbonate producers remained high, mostly as they could still earn some profits when the battery-grade lithium carbonate price was Yuan 480,000/t. In January, lithium carbonate producers' output increased by 4,500 tonnes from December last year. However, with battery-grade lithium carbonate prices dropping to near the cost price of outsourced lithium concentrates in February, the operating rate of lithium carbonate producers fell to 55.86%, and their output decreased by 4,000 tonnes month on month to 30,200 tonnes accordingly.

If the price of lithium compounds continues to fall faster than that of lithium concentrates, it will affect the cash cost of manufacturers using outsourced lithium ore to produce lithium compounds and force them to rein in production, which will in turn have a negative impact on the market supply of lithium carbonate to some extent. But as the weather gets warmer, the gradual thawing of icy salt lakes will lead to a gradual rise in lithium carbonate production. Lithium carbonate production in March is expected to reach 33,000 tonnes, an increase of 9.27% from the previous month, according to data from Mysteel New Energy Business Unit.

Figure 1-5: Lithium carbonate output in China (Unit: tonne)

Source: Mysteel

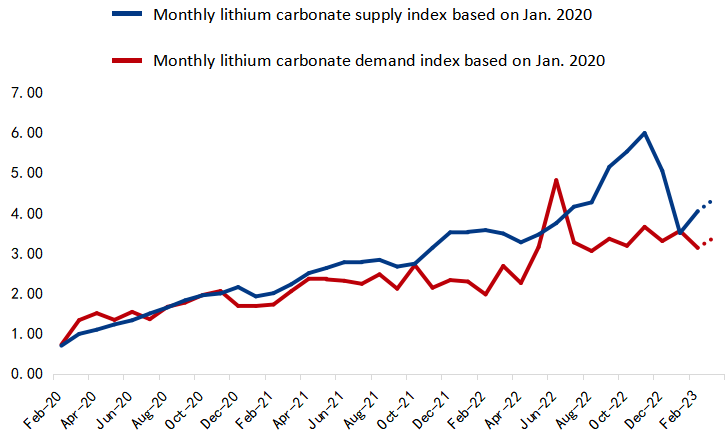

According to the lithium carbonate supply and demand gap model, although the decline in demand for power batteries has led to a sharp drop in lithium carbonate demand in the short term, the demand curve is still above the supply curve. This indicates that lithium carbonate will keep a supply and demand imbalance in the long run, despite currently showing a transient match between supply and demand. It is expected that the price of lithium carbonate may see some support when it approaches the cost price.

Figure 1-6: Lithium carbonate supply and demand gap model

Source: Mysteel

Meanwhile, the cathode manufacturers mostly purchased lithium carbonate to meet their immediate production needs rather than making any large-scale procurement after the lithium carbonate price dropped swiftly from its peak. It can be estimated that the lithium carbonate inventories of the cathode manufacturers remain at a low level at present. Based on the above analysis, the downstream demand has shown signs of strengthening in March, and the widening price gap between lithium carbonate and lithium concentrate will lead lithium compounds producers to lower their operating rates. It is expected that the price of lithium carbonate will gradually stabilize in the range of Yuan 320-350,000/tonne by the end of March, with little chance of rebounding.

Written by Mysteel Nonferrous Metal & New Energy Research Center

Edited by Ruby Zhang, zhangjiajing@mysteel.com; Alyssa Ren, rentingting@mysteel.com