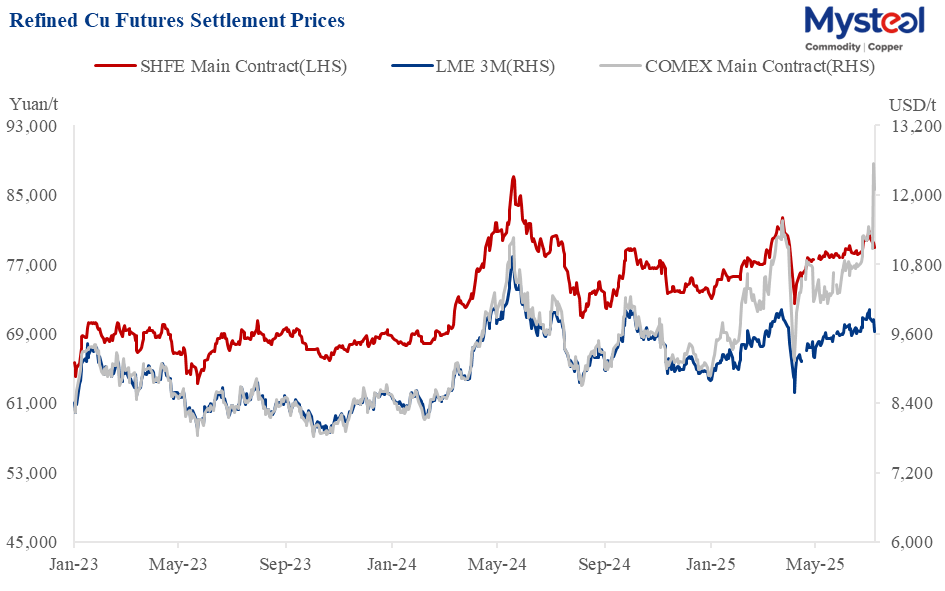

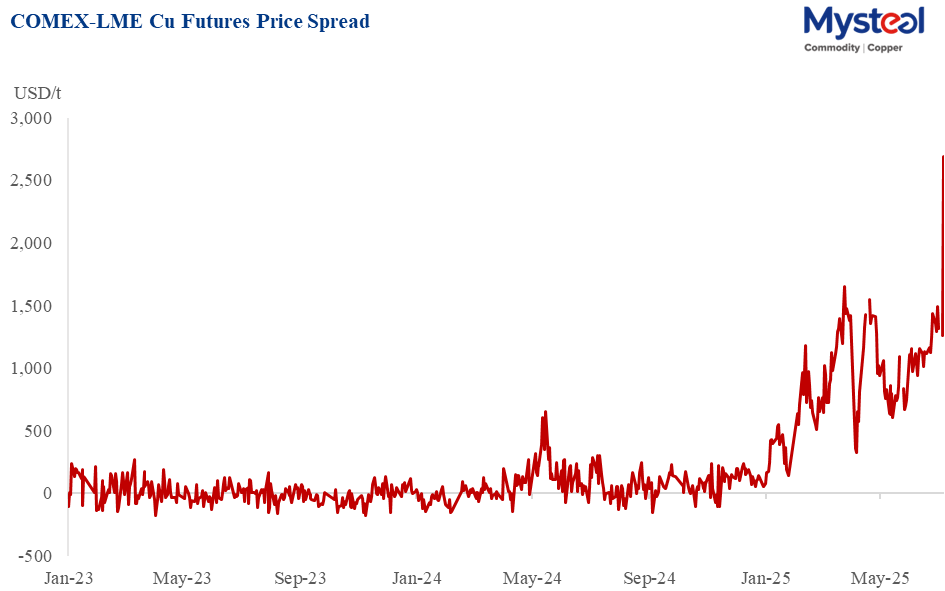

The proposed 50% U.S. copper tariff sharply fragmented the global copper pricing last week: the New York Commodity Exchange (COMEX) showed significant premiums, while the London Metal Exchange (LME) and the Shanghai Futures Exchange (SHFE) prices declined, amplifying macro volatility.

Data Source: Mysteel, SHFE, LME, COMEX

Mysteel's China refined copper average spot price declined by 1.6% or Yuan 1,285/tonne week on week to Yuan 79,168/tonne last week. The LME three-month (3M) average settlement price retreated by 1.94% or $193/tonne to $9,738/tonne. Conversely, the COMEX copper main contract average settlement price was up further by 6.8% week on week, with the COMEX-LME spread surging to $2,711/tonne on July 11.

Data Source: Mysteel, LME, COMEX

Spot premiums decreased further last week, with Mysteel's Shanghai standard refined copper spot premium falling to -Yuan 55/tonne on Friday (July 11) and the LME Cash-3M settlement price spread dropping to -$7.5/tonne.

Refined copper supply in China remained stable as most of the smelters kept normal production, with week-on-week increasing shipments to warehouses. China's June refined output rose by 17.14% year on year, with further increases expected in July-August as maintenance eases.

Price declines stimulated downstream restocking. Orders improved week on week, with copper rod inventories falling by 600 tonnes week on week to 14,800 tonnes and mid-week orders hitting a monthly high. However, absolute demand remained subdued seasonally, with persistent price competition. Pickup activity was stable, with some reports of accelerated deliveries.

Production at China's copper semis enterprises diverged last week, with output of refined copper rod and copper plate/strip increasing by 21.73% and 4.2% week on week, respectively, but secondary copper rod, copper tube and copper bar falling by 6.81%, 3.5% and 1.0%, respectively, according to Mysteel's survey of 27 refined copper rod, 27 secondary copper rod, 12 copper plate/strip, 31 copper tube, and 30 copper bar fabricators.

As a result, China's refined copper social inventory rose by 18,700 tonnes compared with July 3 to 148,100 tonnes on July 10, driven by increased refineries' production and shipments but overall softer demand. Bonded zone inventories dipped slightly to 72,500 tonnes, with a weekly decrease of 500 tonnes.

LME inventory rose further by 14.6% or 13,775 tonnes compared with July 3 to 108,100 tonnes on July 10. On the same day, COMEX inventories rose by 5% week on week to 209,647 tonnes, reflecting continuous material shifting toward North America.

Macro factors, especially tariffs, have had a greater impact on copper prices. Besides, other key data to watch this week are China's aggregate financing, money supply, and the second quarter GDP figures; US June inflation and retail sales data, among others.

Fundamentally, Chinese demand improved sequentially on price dips but remains volume-constrained. China's refined copper output continues expanding during peak production season, though visible inventory builds may be limited by spot market pressure. The export potential has narrowed as SHFE-LME spreads have compressed, pointing to lower July exports.

While tariffs disproportionately impact global trade flows over outright prices, weakening China's domestic fundamentals reduce upside momentum. Bottom-end support from physical buying should contain losses, leading to range-bound consolidation this week.

China's domestic will rangebound at Yuan 77,800-79,500 tonnes, and the LME copper core range is expected to be $9,480-9,790/tonne. Driven by material shifts and policy expectations, COMEX copper is projected at highs of $5.45-5.72/lb. COMEX premiums are expected to hold above $2,500/tonne amid continued market fragmentation.

For more in-depth insights, long-term outlook, and comprehensive data on China's copper market, contact us via <xuzhongping@mysteel.com> to subscribe to Mysteel Copper Weekly/Monthly, and Mysteel Copper Database.

FREE Webinar: 2025 Mysteel China Base Metals Semi-annual Review & Outlook

Join us to meet our senior non-ferrous analysts and gain the latest intelligence to stay ahead in the market. Register now to secure your spot!

Written by Paula Xu, xuzhongping@mysteel.com