On June 1, LME copper prices grew, while China's futures and spot markets saw prices slightly fall. The U.S. is expected to decide whether to impose import tariffs on refined copper by late June, with the market beginning to worry that refined copper will continue flowing into the U.S. market, reducing supply elsewhere and pushing copper prices even higher.

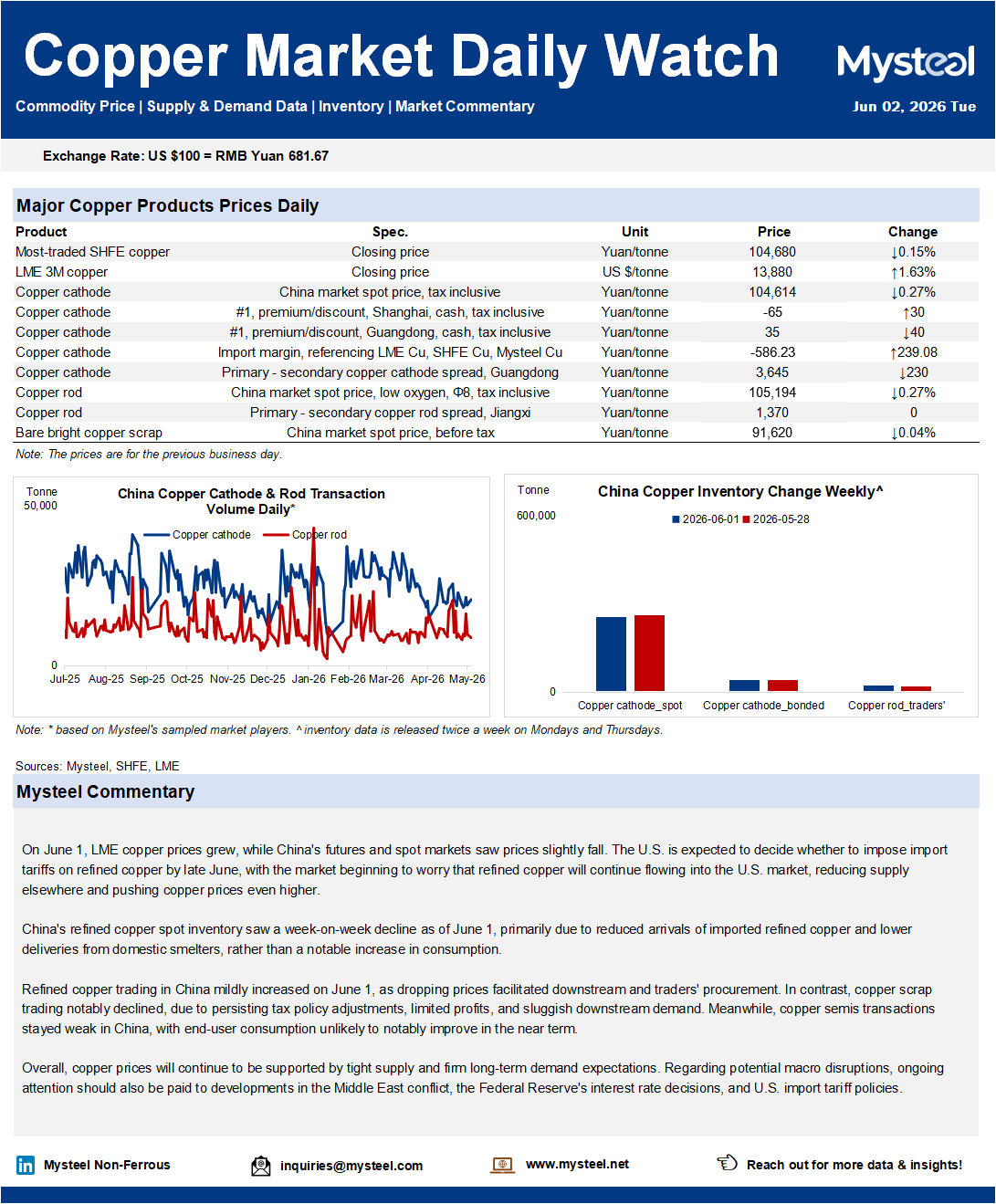

China's refined copper spot inventory saw a week-on-week decline as of June 1, primarily due to reduced arrivals of imported refined copper and lower deliveries from domestic smelters, rather than a notable increase in consumption.

Refined copper trading in China mildly increased on June 1, as dropping prices facilitated downstream and traders' procurement. In contrast, copper scrap trading notably declined, due to persisting tax policy adjustments, limited profits, and sluggish downstream demand. Meanwhile, copper semis transactions stayed weak in China, with end-user consumption unlikely to notably improve in the near term.

Overall, copper prices will continue to be supported by tight supply and firm long-term demand expectations. Regarding potential macro disruptions, ongoing attention should also be paid to developments in the Middle East conflict, the Federal Reserve's interest rate decisions, and U.S. import tariff policies.