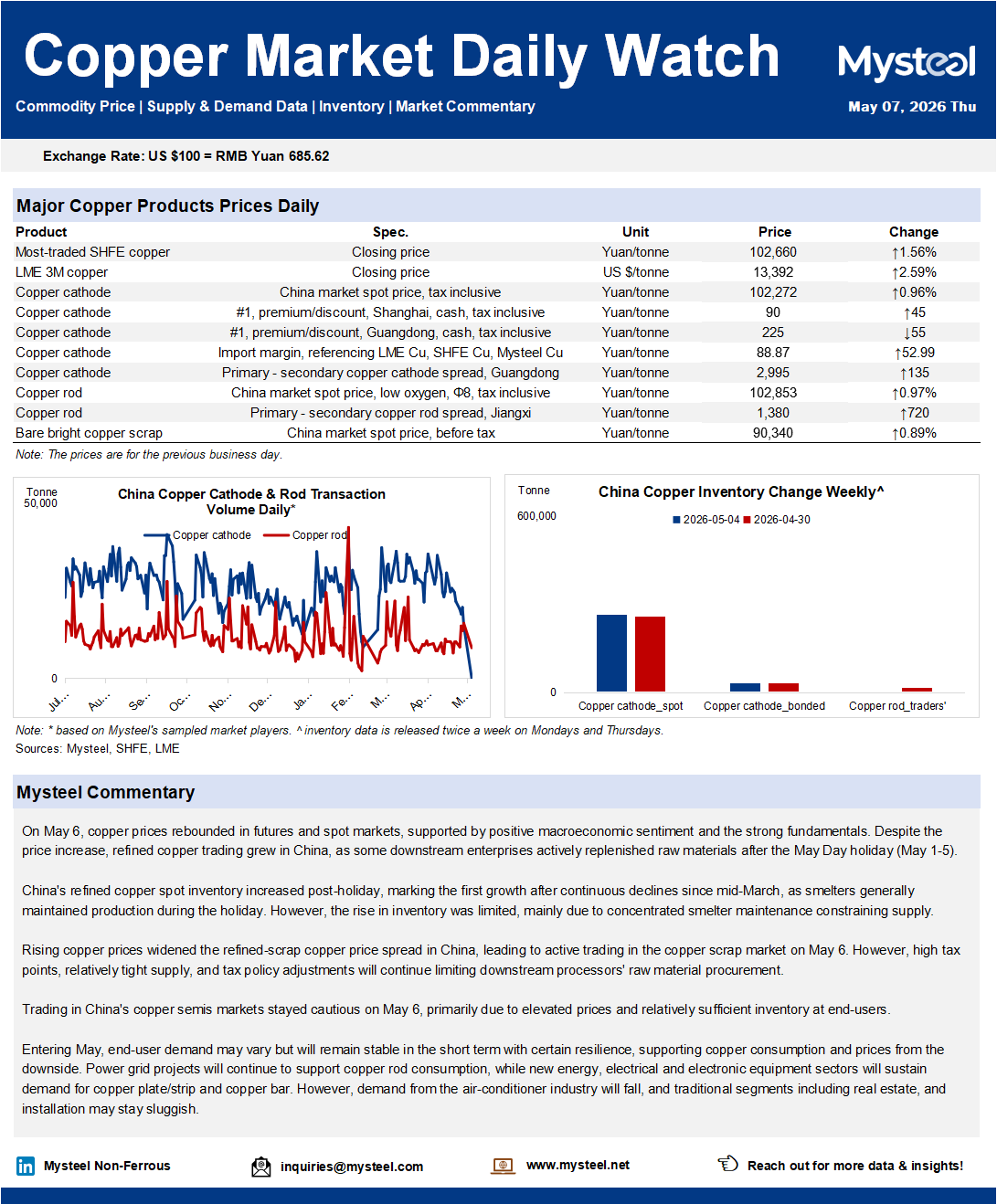

On May 6, copper prices rebounded in futures and spot markets, supported by positive macroeconomic sentiment and the strong fundamentals. Despite the price increase, refined copper trading grew in China, as some downstream enterprises actively replenished raw materials after the May Day holiday (May 1-5).

China's refined copper spot inventory increased post-holiday, marking the first growth after continuous declines since mid-March, as smelters generally maintained production during the holiday. However, the rise in inventory was limited, mainly due to the concentrated smelter maintenance constraining supply.

Rising copper prices widened the refined-scrap copper price spread in China, leading to active trading in the copper scrap market on May 6. However, high tax points, relatively tight supply, and tax policy adjustments will continue limiting downstream processors' raw material procurement.

Trading in China's copper semis markets stayed cautious on May 6, primarily due to elevated prices and relatively sufficient inventory at end-users.

Entering May, end-user demand may vary, but will remain stable in the short term with certain resilience, supporting copper consumption and prices from the downside. Power grid projects will continue to support copper rod consumption, while new energy, electrical and electronic equipment sectors will sustain demand for copper plate/strip and copper bar. However, demand from the air-conditioner industry will fall, and traditional segments including real estate, and installation may stay sluggish.