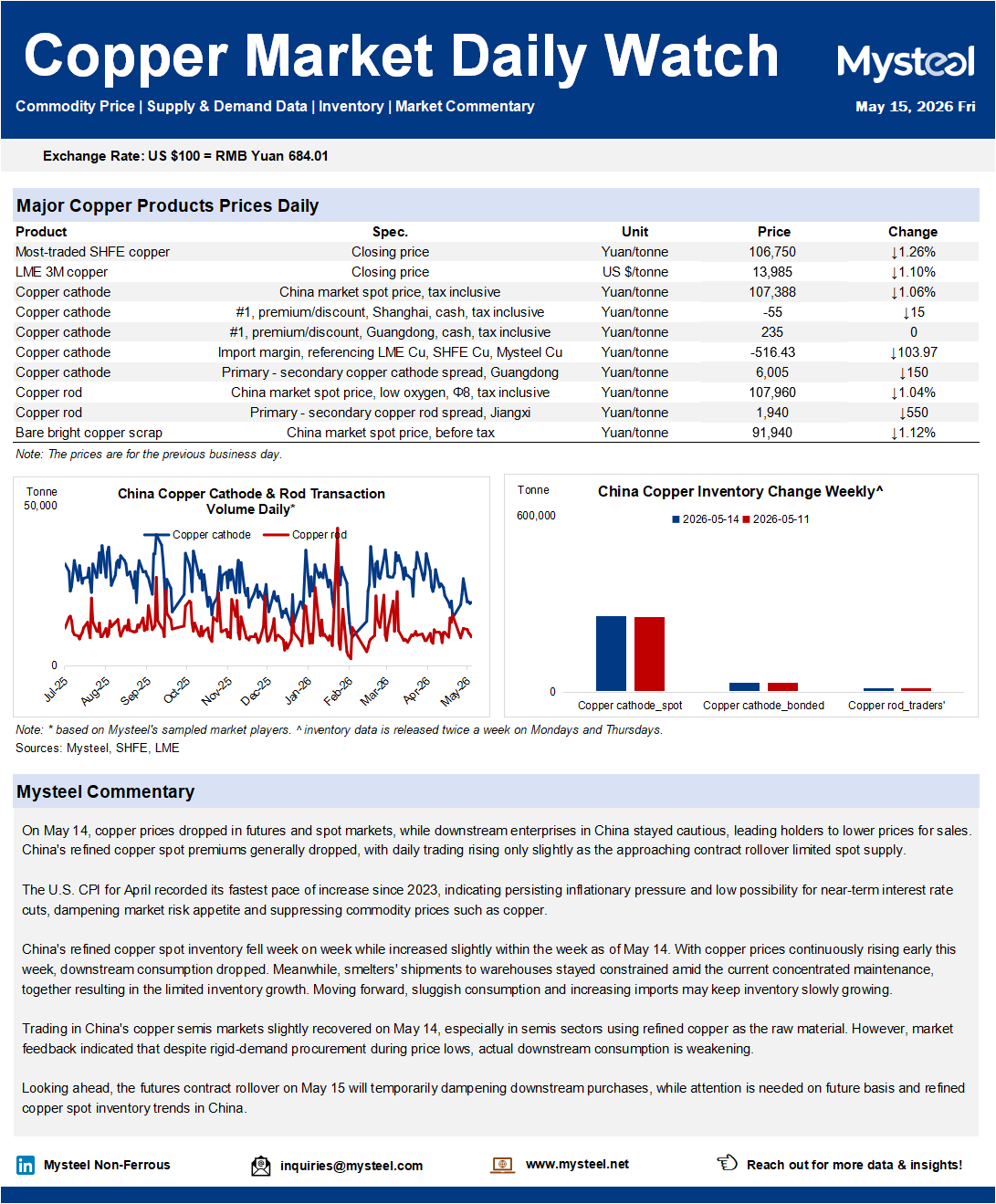

On May 14, copper prices dropped in futures and spot markets, while downstream enterprises in China stayed cautious, leading holders to lower prices for sales. China's refined copper spot premiums generally dropped, with daily trading rising only slightly as the approaching contract rollover limited spot supply.

The U.S. CPI for April recorded its fastest pace of increase since 2023, indicating persisting inflationary pressure and low possibility for near-term interest rate cuts, dampening market risk appetite and suppressing commodity prices such as copper.

China's refined copper spot inventory fell week on week while increased slightly within the week as of May 14. With copper prices continuously rising early this week, downstream consumption dropped. Meanwhile, smelters' shipments to warehouses stayed constrained amid the current concentrated maintenance, together resulting in the limited inventory growth. Moving forward, sluggish consumption and increasing imports may keep inventory slowly growing.

Trading in China's copper semis markets slightly recovered on May 14, especially in semis sectors using refined copper as the raw material. However, market feedback indicated that despite rigid-demand procurement during price lows, actual downstream consumption is weakening.

Looking ahead, the futures contract rollover on May 15 will temporarily dampening downstream purchases, while attention is needed on future basis and refined copper spot inventory trends in China.