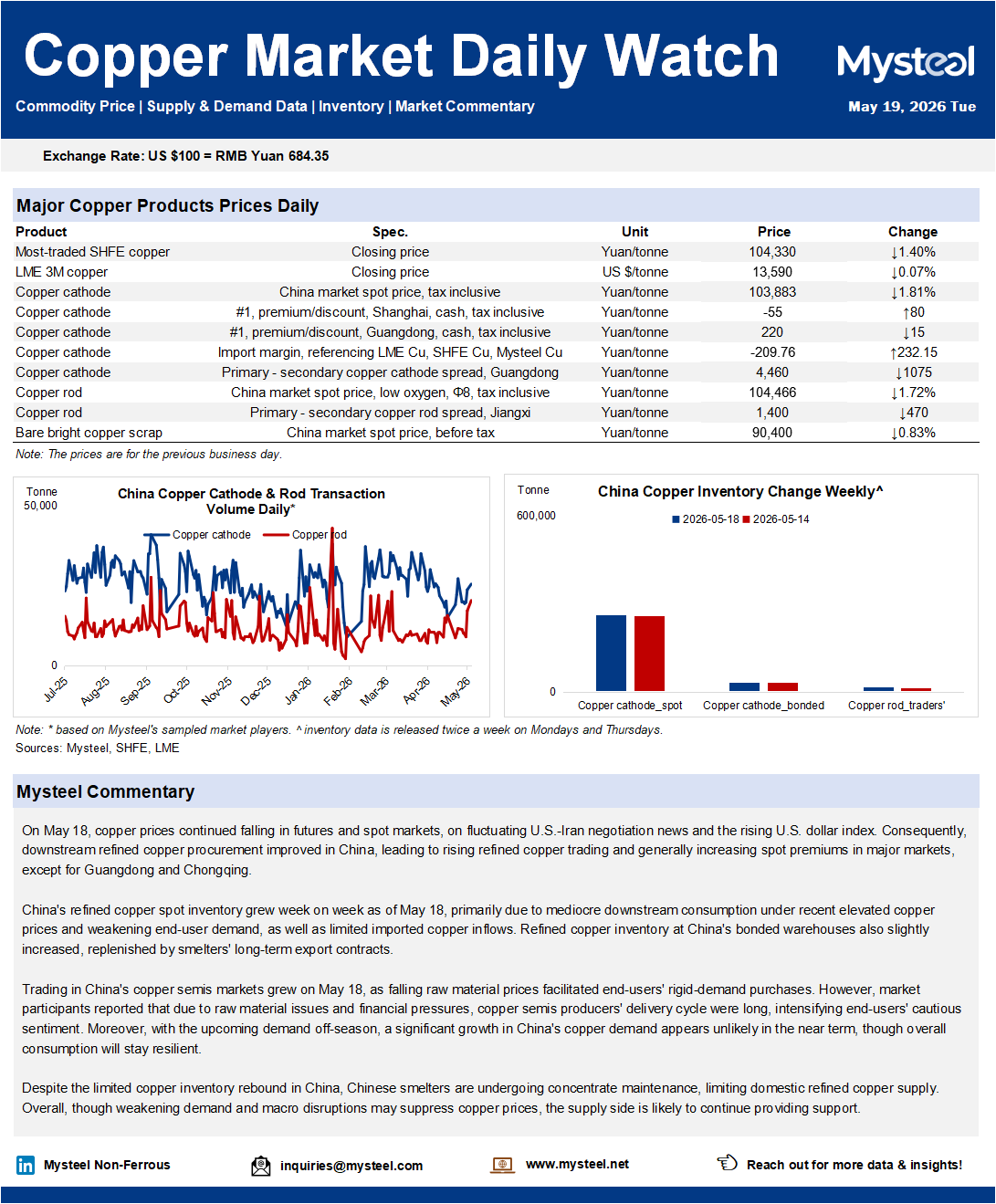

On May 18, copper prices continued falling in futures and spot markets, on fluctuating U.S.-Iran negotiation news and the rising U.S. dollar index. Consequently, downstream refined copper procurement improved in China, leading to rising refined copper trading and generally increasing spot premiums in major markets, except for Guangdong and Chongqing.

China's refined copper spot inventory grew week on week as of May 18, primarily due to mediocre downstream consumption under recent elevated copper prices and weakening end-user demand, as well as limited imported copper inflows. Refined copper inventory at China's bonded warehouses also slightly increased, replenished by smelters' long-term export contracts.

Trading in China's copper semis markets grew on May 18, as falling raw material prices facilitated end-users' rigid-demand purchases. However, market participants reported that due to raw material issues and financial pressures, copper semis producers' delivery cycle were long, intensifying end-users' cautious sentiment. Moreover, with the upcoming demand off-season, a significant growth in China's copper demand appears unlikely in the near term, though overall consumption will stay resilient.

Despite the limited copper inventory rebound in China, Chinese smelters are undergoing concentrate maintenance, limiting domestic refined copper supply. Overall, though weakening demand and macro disruptions may suppress copper prices, the supply side is likely to continue providing support.