China's domestic producers of ternary precursors and cathode active materials face margin compression following the cancellation of the 13% VAT export rebates effective April 1, 2026, a policy aimed at driving industrial upgrading. However, the transition toward a healthier and more sustainable global supply chain inevitably requires short-term pain and sustained effort.

Specifically, effective April 1, 2026, the 13% VAT export rebate for ternary precursors and ternary cathode materials has been formally abolished. This policy adjustment is not aimed at increasing fiscal revenue but rather represents a strategic move by the government to steer the new energy materials industry from "scale expansion" toward "quality priority." The goal is to wean companies off their reliance on export subsidies and refocus on healthy competition based on technology, cost efficiency, and service.

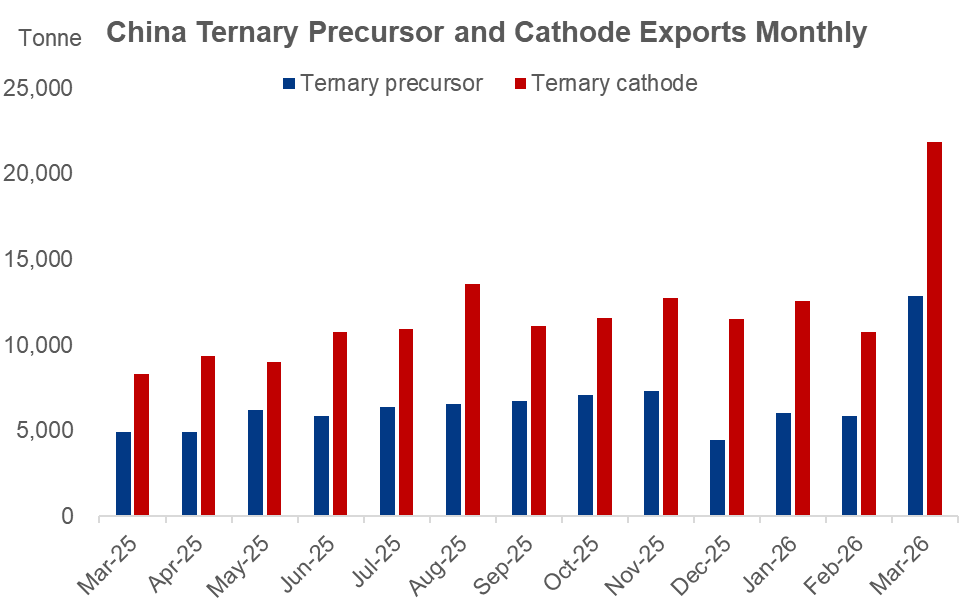

Against this backdrop, China's exports of ternary precursors and cathode materials surged sharply in March, as companies rushed to ship ahead of the policy deadline.

Source: GACC

According to data from the General Administration of Customs of the People's Republic of China (GACC), March 2026 exports of ternary precursors reached 12,871 tonnes, up 7,028 tonnes or 120.3% month-on-month and surging 163.0% year-on-year. Cumulative exports for Q1 2026 stood at 24,729 tonnes, up 45.5% year-on-year.

Ternary cathode exports (NCM + NCA) totaled 21,900 tonnes in March, up 103.1% month-on-month and 163% year-on-year. NCM accounted for 20,900 tonnes, or 96% of the total. South Korea remained the largest destination, importing 8,500 tonnes in March, followed by Poland (3,720 tonnes), Malaysia (2,409 tonnes), and Japan (2,363 tonnes).

The compression of margins triggered by the rebate cancelation is the sole and primary driver behind the export rush. Based on Mysteel's analysis, the removal of the export rebate directly reduces profitability by Yuan 10,000-20,000 per tonne for ternary cathode material. Previously, the export gross margins were typically 10-20 percentage points higher than domestic margins, and together with favorable metal price differentials, overseas customers were a key source of profit. That advantage has now largely evaporated.

What worries the industry more is that Chinese products may lose further ground relative to South Korea's cathode active materials, as Korean producers face no similar rebate cancellation and their products benefit from lower tariffs or subsidy support in some overseas markets.

In response to rising costs, Companies have tried to negotiate price hikes with customers, and while market feedback suggests this is feasible, customer resistance is strong, often citing strict contract terms. How much cost can be passed on depends on bargaining power, with sole-source suppliers having some leverage. However, customers tend to accelerate the development of alternative suppliers, eroding long-term advantages. Ultimately, cathode suppliers in this industry generally have weak pricing power.

Some companies are exploring deep-processing transfers. This refers to processing trade enterprises passing products to downstream battery cell customers, which then export finished goods. This bypasses export rebates entirely, so the rebate cancellation has no direct impact.

However, the bar is high as the battery plants must hold processing trade manuals and final products must be exported. Suppliers may also lose overseas premiums, with pricing reverting to domestic benchmarks. Still, for companies serving battery customers' export orders, this remains a pragmatic way to cut logistics costs and simplify pricing.

Another alternative is toll processing. That is, the overseas customers supply raw materials, domestic firms collect only processing fees, and finished products are returned for export. Imported materials and processing fees are VAT-exempt, and finished exports are also VAT-free, making toll processing completely unaffected by the rebate cancellation.

This model eliminates procurement financing and commodity price risk for nickel, cobalt, and lithium, with profits coming solely from processing fees. However, conditions are strict. The overseas customers must provide materials and bear capital costs, and companies must accept a fee-based profit model. Toll processors also need processing trade qualifications and manuals, while VAT on domestic auxiliary materials is non-deductible and must be absorbed as costs.

For companies with stable, long-term overseas customers that have strong raw material supply capabilities, toll processing is a compliance path worth exploring. But its applicability is limited for those serving domestic customers or purchasing raw materials independently.

Building overseas production capacity remains a viable option for companies with resources and strategic ambition. Industry trends point to capacity builds in Indonesia, Europe, and South Korea, enabling firms to move closer to target markets, sidestep trade barriers, and lower logistics costs.

Still, going overseas is not a universal solution, nor the only path. Companies should decide based on their customer mix, financial position, and technological edge. Those that excel at home through innovation and lean management are equally capable of succeeding on the global stage.

In summary, the export rebate's removal has upended traditional profit models, with March's rush marking the last hurrah. Near term, companies will weigh price negotiations, deep-processing transfers, and toll processing. Medium to long term, overseas production capacity will be a key competitiveness driver.

Choices will vary by customer mix, finances, and technology. Not every firm needs to go overseas, but matching overseas producers on cost, delivery, and compliance is critical for global share and pricing power. The policy's intent is to shift the industry from "rebate profits" to "technology and management profits", building a healthier supply chain. For the industry, this is both painful and a catalyst for upgrading.

Written by Aggie Hu, huchenying@mysteel.com

Join Mysteel's April 30 webinar to explore whether supply disruptions will drive the next leg higher for lithium and nickel markets in Q2 2026.

https://www.mysteel.net/event-listings/100067-q2-2026-lithium-and-nickel-will-supply-disruptions-fuel-further-price-hikes