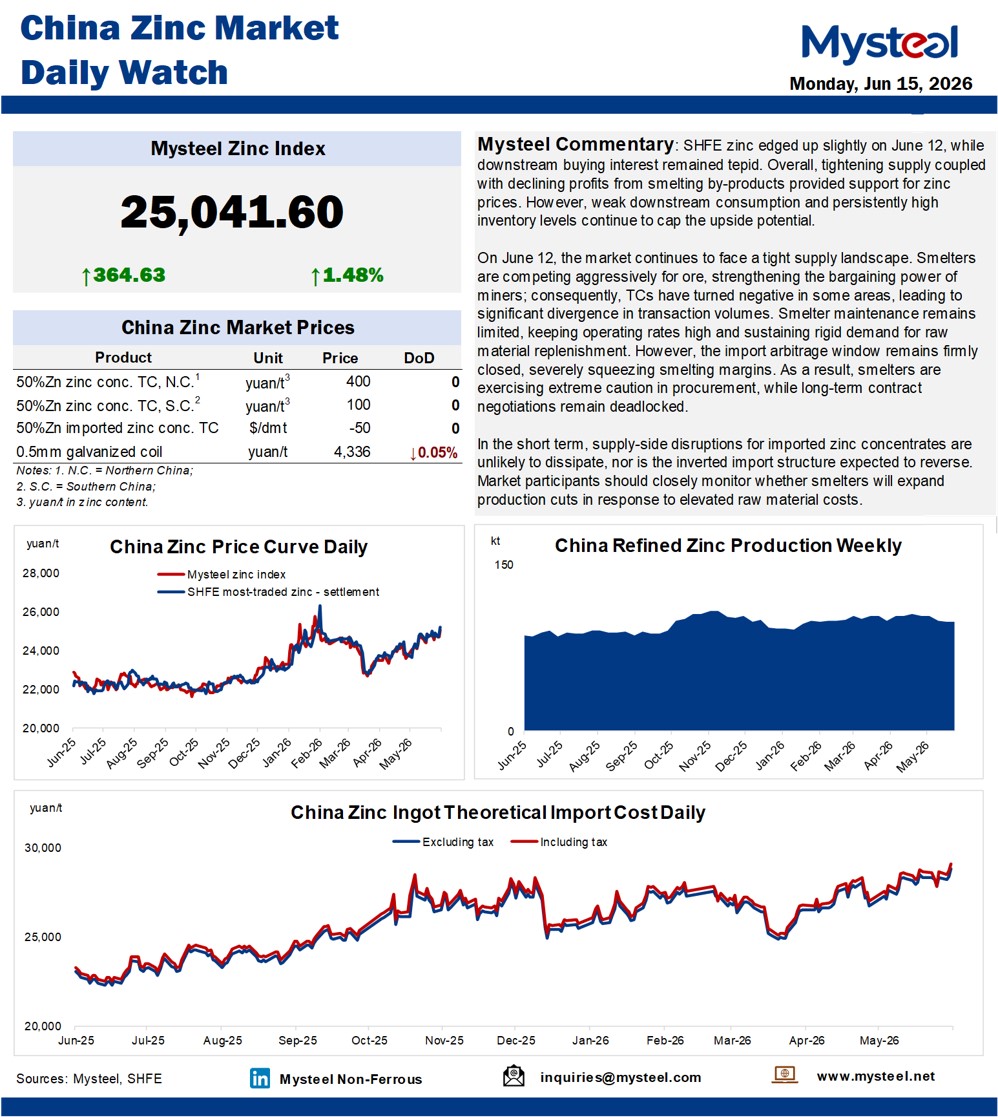

SHFE zinc edged up slightly on June 12, while downstream buying interest remained tepid. Overall, tightening supply coupled with declining profits from smelting by-products provided support for zinc prices. However, weak downstream consumption and persistently high inventory levels continue to cap the upside potential.

On June 12, the market continues to face a tight supply landscape. Smelters are competing aggressively for ore, strengthening the bargaining power of miners; consequently, TCs have turned negative in some areas, leading to significant divergence in transaction volumes. Smelter maintenance remains limited, keeping operating rates high and sustaining rigid demand for raw material replenishment. However, the import arbitrage window remains firmly closed, severely squeezing smelting margins. As a result, smelters are exercising extreme caution in procurement, while long-term contract negotiations remain deadlocked.

In the short term, supply-side disruptions for imported zinc concentrates are unlikely to dissipate, nor is the inverted import structure expected to reverse. Market participants should closely monitor whether smelters will expand production cuts in response to elevated raw material costs.