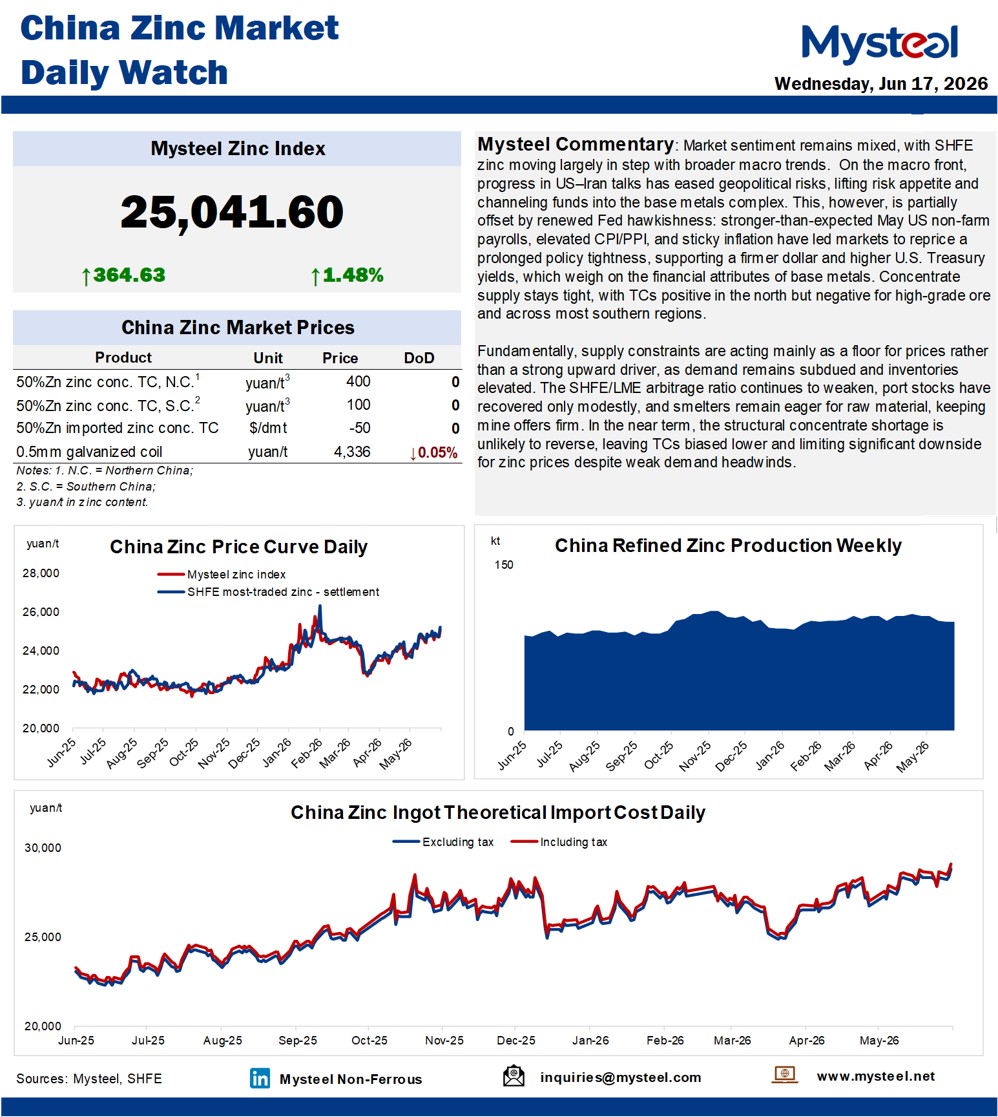

Market sentiment remains mixed, with SHFE zinc moving largely in step with broader macro trends. On the macro front, progress in US–Iran talks has eased geopolitical risks, lifting risk appetite and channeling funds into the base metals complex. This, however, is partially offset by renewed Fed hawkishness: stronger-than-expected May US non-farm payrolls, elevated CPI/PPI, and sticky inflation have led markets to reprice a prolonged policy tightness, supporting a firmer dollar and higher U.S. Treasury yields, which weigh on the financial attributes of base metals. Concentrate supply stays tight, with TCs positive in the north but negative for high-grade ore and across most southern regions.

Fundamentally, supply constraints are acting mainly as a floor for prices rather than a strong upward driver, as demand remains subdued and inventories elevated. The SHFE/LME arbitrage ratio continues to weaken, port stocks have recovered only modestly, and smelters remain eager for raw material, keeping mine offers firm. In the near term, the structural concentrate shortage is unlikely to reverse, leaving TCs biased lower and limiting significant downside for zinc prices despite weak demand headwinds.