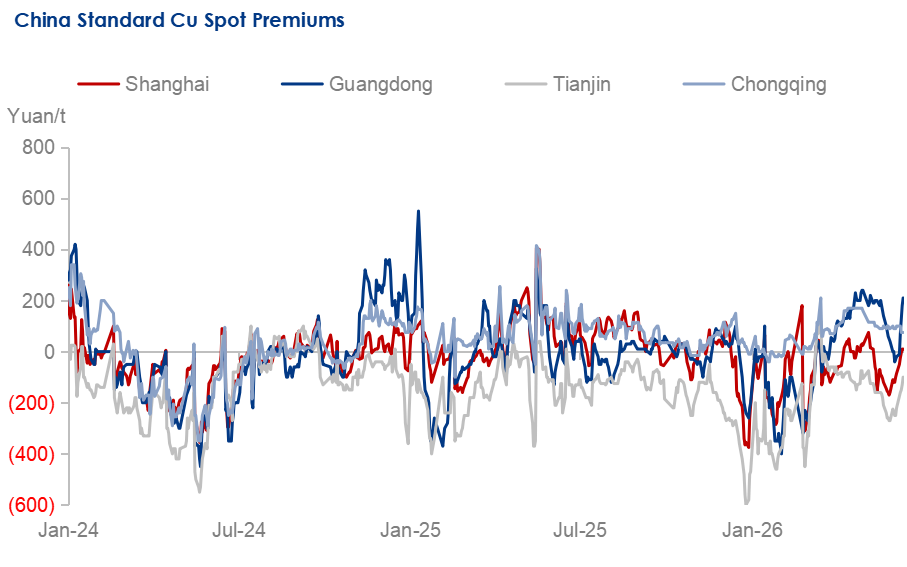

Premium: Improving demand and tight supply drive up refined copper spot premiums

Copper prices moved lower last week. Spot premiums in the refined copper market rose, and the Shanghai-Guangdong refined copper spot price spread widened again. As prices fell during the week, downstream restocking demand on dips was decent. Approaching delivery and contract rollover, the SHFE front-month copper contract held a contango spread. Combined with relatively limited market arrivals, holders were strongly inclined to stand firm on offers and limit sales. As a result, spot premiums in China's refined copper market increased last week.

Looking ahead, given major developments in the Middle East geopolitical situation, copper prices are expected to rebound in the near term. High prices will likely make downstream purchasing sentiment more cautious, capping spot premiums. However, with market arrivals still expected to be limited this week, China's refined copper spot premiums will likely fluctuate within a narrow range. According to Mysteel, refined copper spot premium ranges are forecast with Shanghai at Yuan 0/tonne to Yuan 100/tonne, Guangdong at Yuan 150/tonne to Yuan 250/tonne, Tianjin at -Yuan 150/tonne to -Yuan 50/tonne, and Chongqing at -Yuan 50/tonne to Yuan 150/tonne this week.

Data Source: Mysteel

Supply: Limited domestic and overseas arrivals tighten China's refined copper spot supply

China's refined copper spot supply remained tight last week. Specifically, smelters in Shanghai, undergoing maintenance and prioritizing deliveries against long-term contracts, sent limited spot volumes to the market. Although the import ratio improved, only small amounts of imported copper cleared customs and entered the domestic market. Meanwhile, shipments from smelters in Guangdong and Chongqing were also relatively low. Moreover, as the spot premium spread with southern China widened, spot cargoes in Tianjin largely flowed into southern markets or were used for deliveries, gradually tightening local supply. Overall, refined copper spot supply in China was relatively tight last week. Looking ahead, after futures delivery, the release of warrant inventory may replenish spot supply in the near term. However, given concentrated smelter maintenance, increased exports, and reduced imports, overall refined copper spot supply in China is forecast to remain tight.

Demand: Falling copper prices drive up spot trading

China's refined copper spot trading rose last week. As copper prices moved lower, downstream purchasing appetite improved in Shanghai and Guangdong, lifting trading activity in the spot market. In addition, orders received by some downstream enterprises also increased following the price decline, further supporting refined copper procurement. However, rising spot premiums partially dampened buying sentiment among some firms. Spot trading in Tianjin was relatively subdued, as downstream enterprises had yet to work through finished goods inventories despite price declines, limiting raw material purchasing interest. In Chongqing, downstream buyers showed little willingness to purchase refined copper ahead of contract rollover, mostly restocking on dips, and spot deals remained difficult even when traders lowered their premium offers. However, China's refined copper spot trading still improved last week.

Looking ahead, near-term expectations of a copper price rebound are likely to curb downstream procurement volumes. Combined with limited growth in end-user orders, rigid demand from enterprises will also ease. Consequently, spot trading volume in China's refined copper market is expected to decline in the short run.

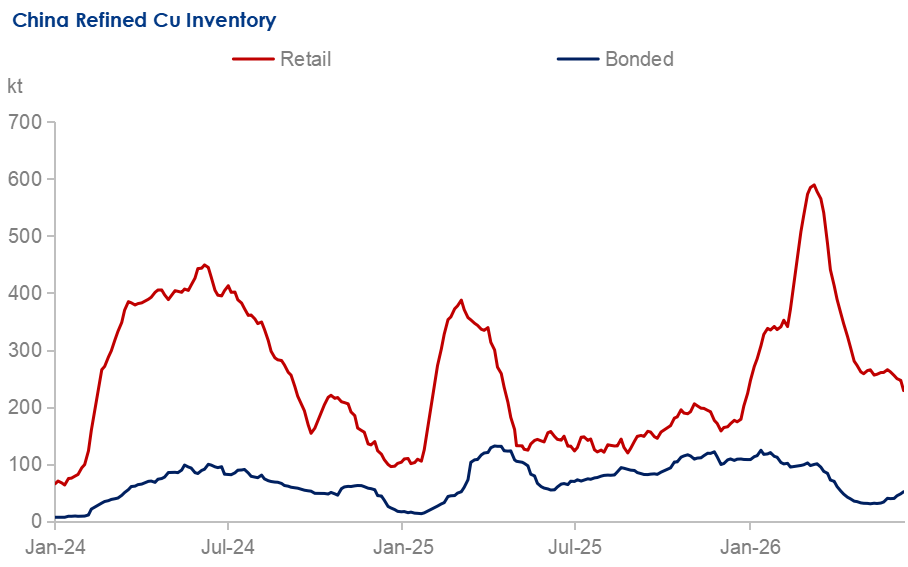

Inventory: China refined copper retail inventory declines but bonded inventory rises

China's refined copper retail inventory continued to decline last week. On the inflow side, warehouse arrivals were limited, as smelter maintenance remained at a seasonal peak and a weak refined copper import ratio led to lower imports. On the outflow side, falling copper prices boosted new orders at downstream enterprises, supporting decent dip-buying restocking and lifting warehouse departures. As a result, China's refined copper retail inventory fell last week. Looking ahead, the market is likely to face a weak supply-demand balance in the near term, so refined copper retail inventory in China is expected to show only limited changes this week.

China's refined copper bonded inventory rose week on week last week, mainly driven by increased shipments from domestic smelters as export profits improved. Gradual import arrivals at some bonded warehouses and low customs-clearance willingness among domestic import traders also contributed to the build. Looking ahead, smelters' planned export cargoes are expected to continue flowing into bonded zones, so China's refined copper bonded inventory may keep rising in the near term.

The weekly average spread between the main COMEX and LME copper contracts was down by $77.19/tonne week on week to $394.53/tonne last week. The average LME cash-3M copper contract settlement spread was -$37.8/tonne last week, down by $16.5/tonne week on week. Last week, although the weekly average COMEX-LME copper spread narrowed, COMEX copper remained at a premium, with the premium briefly surging to $689.36/tonne during the week. As a result, COMEX refined copper inventory maintained their upward trend, while LME inventory continued to decline. In addition, the narrowing contango on LME copper likely boosted enterprises' deliveries, driving LME inventory further down. Looking ahead, as market expectations for the implementation of U.S. tariff policy draw closer, the COMEX copper premium is expected to persist in the near term, keeping its inventory on a modest upward trend. Meanwhile, LME inventory is forecast to continue decreasing.

Data Source: Mysteel

Written by Zhaorui Cui, cuizhaorui@mysteel.com

Edited by Mingyuan Wang, wangmingyuan@mysteel.com