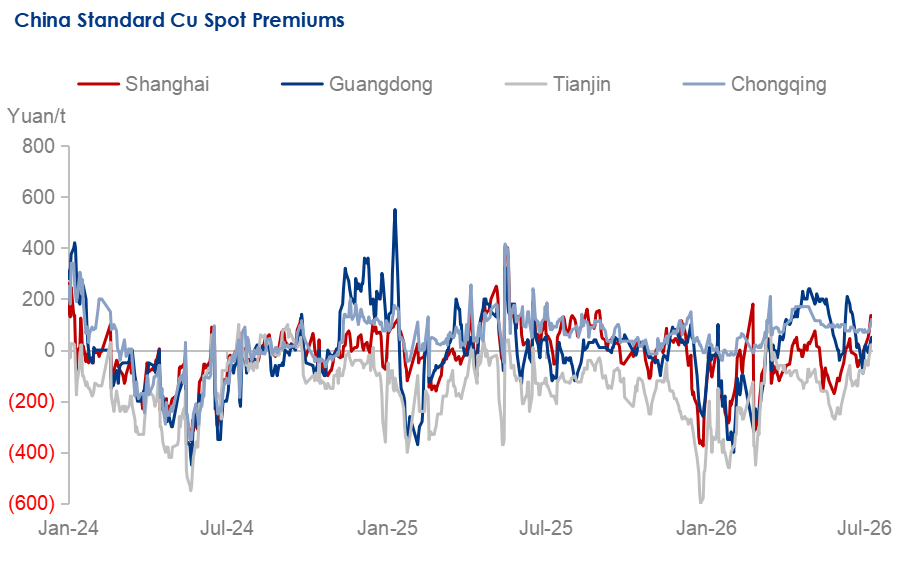

Premium: Tight refined copper supply lifts spot premiums

Due to persistently low domestic refined copper arrivals and limited inflows of imported copper amid typhoon expectations, China's refined copper spot supply was tight last week. Meanwhile, although the weekly average copper price edged higher, downstream enterprises' essential procurement when prices dipped during the week was decent, leading to a slight week-on-week rise in trading volumes. With tight spot availability and resilient consumption, a significant drop in retail inventories lent strong support to spot premiums, while holders' intention to support prices provided an additional boost. As a result, China's refined copper spot premiums hit a year-to-date high last week.

Looking ahead, China's refined copper domestic arrivals are expected to remain limited this week, but imported copper inflows should increase as the import arbitrage window opens. Therefore, even though holders are likely to keep prices firm ahead of futures delivery, the upside for spot premiums is expected to be limited.

Data Source: Mysteel

Supply: China's refined copper spot supply remains tight

China's refined copper spot supply tightness worsened last week. By region, the Southwest market saw a sudden increase in deliveries from local smelters, which significantly improved regional spot circulation. In contrast, deliveries in East, South and North China stayed very limited due to smelter maintenance, with concentrated maintenance outages at several smelters in Shandong notably accentuating regional tightness. In addition, natural disasters such as floods and typhoons also disrupted domestic spot shipments and the arrival of imported copper. Overall, spot supply tightness in China's refined copper market intensified last week. Looking ahead, while imported copper is expected to flow into the domestic market as the import arbitrage window opens, concentrated smelter maintenance is likely to keep spot circulation tight in the near term.

Demand: Consumption stays resilient with spot trading increasing slightly

Trading activity in China's refined copper spot market was mixed. Specifically, some downstream enterprises in Shanghai showed acceptance of slightly fluctuating copper prices, combined with increasing new orders from end-users, and trading increased over the week. In Guangdong and Chongqing, downstream buyers turned more cautious due to higher spot premiums, mainly purchasing based on rigid needs, leaving spot trading volumes rather mediocre. In Tianjin, spot trading was also affected by rising spot premiums, but improved end-user orders when copper prices were low during the week drove increased need-based procurement by downstream enterprises. Overall, consumption in China's refined copper market remained resilient, with spot trading volume edging up slightly week on week. Looking ahead, refined copper spot trading will remain highly price-sensitive in the current consumption off-season. Given that the renewed escalation of U.S.-Iran geopolitical tensions could drive copper prices lower, spot trading in China's refined copper market is expected to improve further this week.

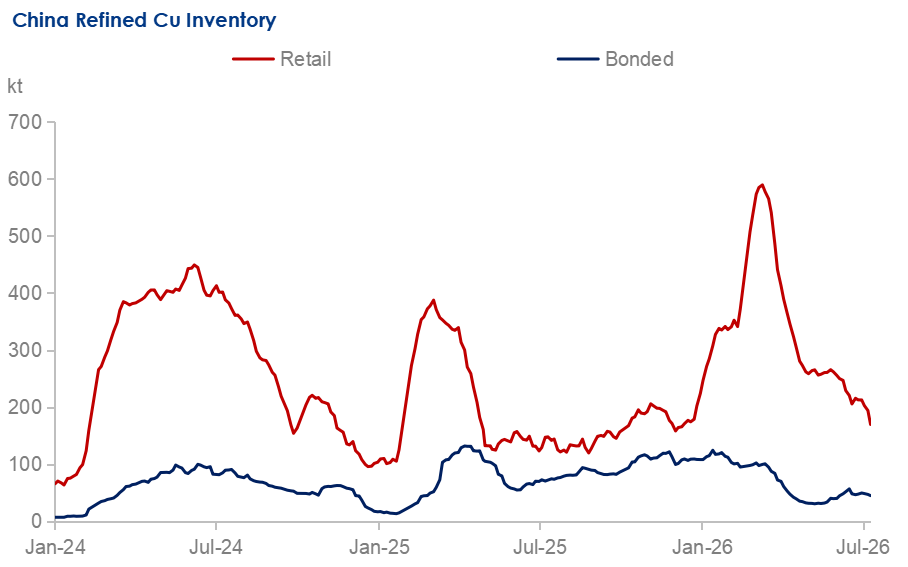

Inventory: China's refined copper retail and bonded inventory both decline

China's refined copper retail inventory fell sharply last week. On one hand, deliveries from domestic smelters stayed low due to maintenance outages, and typhoon weather reduced inflows of imported copper into the domestic market, limiting arrivals at retail warehouses. On the other hand, a slight increase in China's refined copper spot trading volumes led to higher outflows from retail warehouses. Therefore, China's refined copper retail inventory decreased last week. Looking ahead, with smelters still affected by maintenance and import arrivals delaying, spot supply is expected to remain tight, keeping refined copper retail inventory on a downward trend in the near term.

With the import arbitrage window opening, some bonded-zone material was cleared through customs and entered China's domestic market. Combined with limited arrivals and low domestic shipments into bonded zones, China's refined copper bonded inventory declined week on week last week. Looking ahead, as more bonded material is scheduled for customs clearance into the domestic market, refined copper bonded inventory in China is expected to decrease further.

The weekly average spread between the main COMEX and LME copper contracts was up by $4.41/tonne week on week to $365.57/tonne last week. The average LME cash-3M copper contract settlement spread was -$58.1/tonne last week, down by $20.9/tonne week on week. As COMEX copper traded still at a premium and above $200/tonne, COMEX copper inventory kept increasing last week and LME copper inventory fell further. Looking ahead, as the U.S. refined copper tariff policy remains uncertain, COMEX refined copper premiums are expected to persist in the near term, sustaining the trend of rising COMEX inventory and falling LME inventory. Additionally, the persistent contango between LME cash and three-month copper contracts is likely to continue dampening the willingness to deliver into LME warehouses.

Data Source: Mysteel

More regular analysis and comprehensive data on China's copper industry are available in Mysteel Copper Weekly, Mysteel Copper Monthly, and Mysteel Copper Database. Reach out to us via Mysteel's official website: Latest & Reliable Copper Market Price in China | Mysteel, and follow Mysteel Non-Ferrous for more insights!

Don't miss Mysteel's H1 2026 Copper Market FREE Webinar! Check the link below to learn more, and register to secure your spots:

https://www.mysteel.net/event-listings/100073-h1-2026-saw-intertwined-contradictions-in-chinas-copper-market-whats-next-for-h2

Written by Zhaorui Cui, cuizhaorui@mysteel.com

Edited by Mingyuan Wang, wangmingyuan@mysteel.com