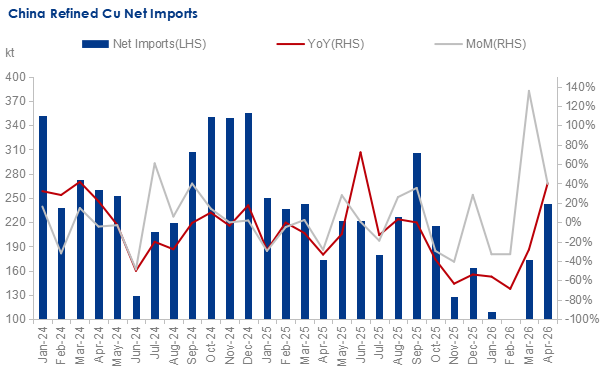

China's refined copper imports increased in April 2026, while exports declined significantly, widening net imports during the month. However, China's refined copper net imports have shown an overall downward trend in recent years, mainly driven by domestic supply expansion, changing global trade flows, and evolving tariff policies. Meanwhile, the structure of China's refined copper trade continues to evolve, with imports from Africa growing and exports generally expanding.

Data Source: GACC, Mysteel

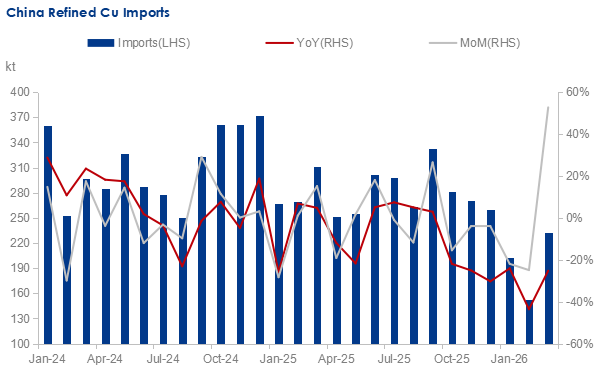

China's refined copper imports reached 268,700 tonnes in April 2026, rising by 6.94% year on year and by 15.62% month on month, according to the General Administration of Customs of China (GACC). Strong refined copper consumption in China supported an increase in April's imports, as downstream copper semis producers maintained active procurement amid resilient end-use demand. In addition, copper prices fell below Yuan 100,000/tonne in early April, further stimulating demand. Meanwhile, Chinese smelters gradually entered a concentrated maintenance period during the month, tightening domestic supply and increasing reliance on imports.

Despite the rebound in April imports, China's refined copper imports have been declining in recent years. Imports totaled 3.363 million tonnes in 2025, down from 3.755 million tonnes in 2024, while January-April 2026 imports also fell year on year. The contraction in imports was driven by several factors.

First, China's refined copper production capacity has been expanding. According to Mysteel's survey of 60 Chinese copper smelters, with a combined annual capacity of 16.98 million tonnes, refined copper output in January-April 2026 increased by 6.85% year on year and by 18.92% compared with the same period in 2024. In contrast, demand growth lagged behind, rising only 0.23% and 10.94%, respectively. As a result, faster supply growth relative to demand has reduced China's dependence on imported refined copper.

Second, U.S. tariff policies have reshaped global copper trade flows. In early July 2025, U.S. President Donald Trump announced a proposed 50% tariff on all copper imports. Although the final policy implemented from August 1, 2025 applied only to semi-finished copper and copper-intensive derivative products, excluding refined copper, significant volumes of refined copper had already been redirected to the U.S. market before policy details were finalized. Supplies from South America, particularly Chile and Peru, as well as African cargoes, were partly redirected to the U.S. market, leading to a decline in refined copper inflows into China.

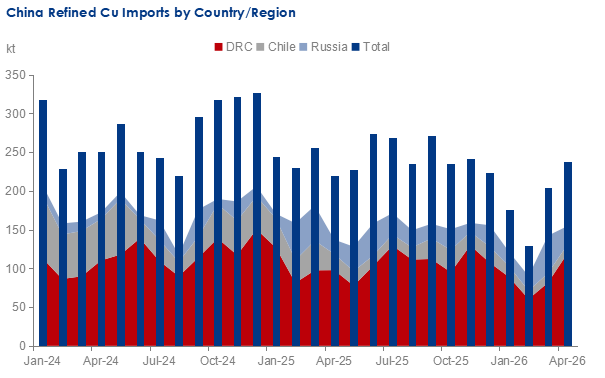

In addition, China's refined copper import structure has changed notably in recent years. In April 2026, the top three suppliers of China's refined copper imports were the Democratic Republic of the Congo (DRC), Russia, and Kazakhstan, accounting for 49.8%, 8.9%, and 6.9% of total imports, respectively. Meanwhile, Chile ranked only sixth, with a share of 4.63%. Chile's share of China's refined copper imports fell to around 10% in 2025, down from 17% in 2024 and 23% in 2023, according to GACC data. The decline was mainly attributed to falling ore grades, rising mining difficulties, and relatively high premiums for South American copper. In contrast, imports from the DRC accounted for approximately 43% of China's total refined copper imports in 2025, compared with 42% in 2024 and 26% in 2023. Growth was supported by the commissioning of Chinese-invested mining projects and the price advantage of non-standard and non-registered copper.

Data Source: GACC, Mysteel

Looking ahead, China's domestic copper consumption is unlikely to record significant growth in the short term. Although Chinese copper smelters are undergoing concentrated maintenance, operating rates remain at historically high levels. In addition, conflict in the Middle East has disrupted African shipments and tightened global sulfuric acid supply, potentially affecting SX-EW copper production in Africa and Chile. Although the import window temporarily opened in May, China's refined copper imports are still expected to decline slightly overall. Over the medium to long term, China's refined copper imports from Africa are expected to continue increasing. However, close attention should be paid to the duration of the global sulfuric acid shortage and its potential impact on SX-EW copper production, as well as potential supply declines from South America caused by disruptions in regional copper mine operations, potential energy risks, and uncertainty surrounding U.S. tariff policies.

Data Source: GACC, Mysteel

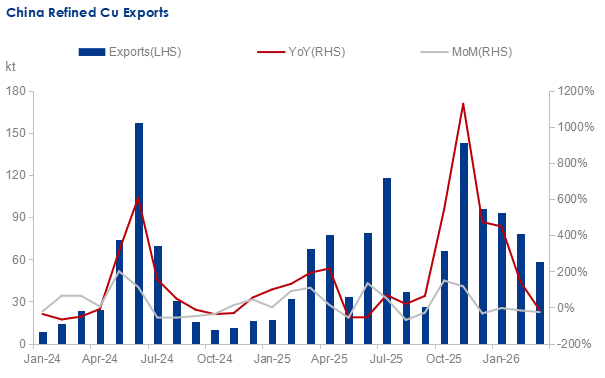

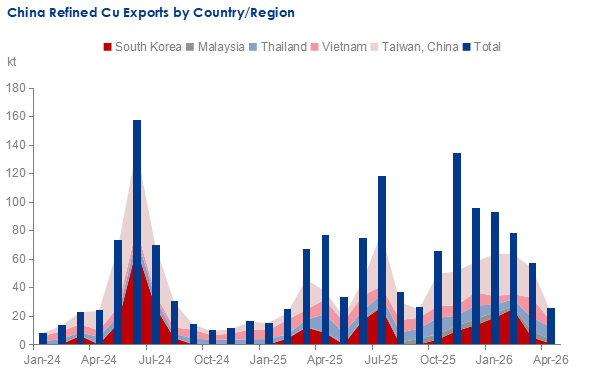

China's refined copper exports reached 256,000 tonnes in April 2026, dropping by 67.05% year on year and by 56.01% month on month, according to the GACC. As many Chinese smelters entered maintenance periods during the month, some prioritized long-term domestic contracts and nearby spot sales, reducing export volumes significantly.

Nevertheless, China's refined copper exports have expanded rapidly in recent years, while export destinations have become increasingly diversified. Refined copper exports reached 794,655 tonnes in 2025, compared with 457,559 tonnes in 2024, while exports during January-April 2026 also increased year on year.

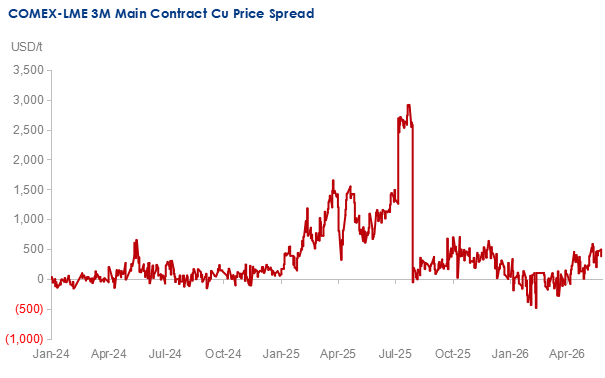

The export growth was mainly driven by two factors. First, domestic demand growth has lagged behind capacity expansion, leading to rising inventory and encouraging smelters to seek overseas markets. According to Mysteel's survey, China's refined copper spot inventory climbed to 589,200 tonnes after the 2026 Chinese New Year holiday, marking the highest level in nearly a decade. Second, as a heavy net importer of refined copper, China's refined copper exports are highly sensitive to arbitrage opportunities. Driven by tariff-related disruptions, the COMEX-LME price spread widened to nearly $3,000/tonne in July 2025, opening profitable export arbitrage opportunities for Chinese smelters. Similarly, the COMEX short squeeze in May 2024 also sharply widened the price spread, and refined copper was redirected to the COMEX market, lifting premiums in the LME market and encouraging Chinese smelters to actively export to nearby Asian LME delivery warehouses in Taiwan and South Korea, for instance.

Data Source: COMEX, LME, Mysteel

In April 2026, the top three destinations for China's refined copper exports were Thailand, Taiwan (China), and Vietnam, accounting for 33.4%, 25.4%, and 15.9% of total exports, respectively. In recent years, China's refined copper exports to emerging Southeast Asian markets have continued to increase. In 2025, combined exports to Thailand, Vietnam, and Malaysia totaled 206,903 tonnes, nearly doubling from 109,082 tonnes in 2024. Exports to these markets also continued to grow during January-April 2026.

Data Source: GACC, Mysteel

Looking ahead, China's refined copper exports still have room to increase in the short term. During May, domestic copper consumption is unlikely to record significant growth, while high prices for by-products such as sulfuric acid continue to support elevated operating rates at Chinese smelters, likely leading inventory pressure to provide further support for exports. Additionally, the U.S. government is expected to decide whether to impose tariffs on refined copper imports by the end of June. If market expectations for U.S. tariffs on refined copper materialize and trigger a widening of the COMEX-LME premium, arbitrage opportunities could once again drive a substantial increase in China's refined copper exports.

Data Source: GACC, Mysteel

Overall, China's declining refined copper net imports reflect both expanding domestic smelting capacity and shifting global trade flows. Meanwhile, high domestic inventory and recurring arbitrage opportunities have supported export growth. However, China remains the world's largest copper consumer, and its position as a net importer is unlikely to change fundamentally. According to ICSG, China's refined copper consumption totaled 16.583 million tonnes in 2025, accounting for 58.9% of global consumption, slightly higher than in 2024. Looking ahead, close attention should be paid to whether U.S. tariffs will be extended to refined copper, whether SX-EW copper production in regions such as the DRC will be actually constrained by sulfuric acid shortages, and further changes in China's refined copper smelting capacity.

Written by Mingyuan Wang, wangmingyuan@mysteel.com

Edited by Zhaorui Cui, cuizhaorui@mysteel.com