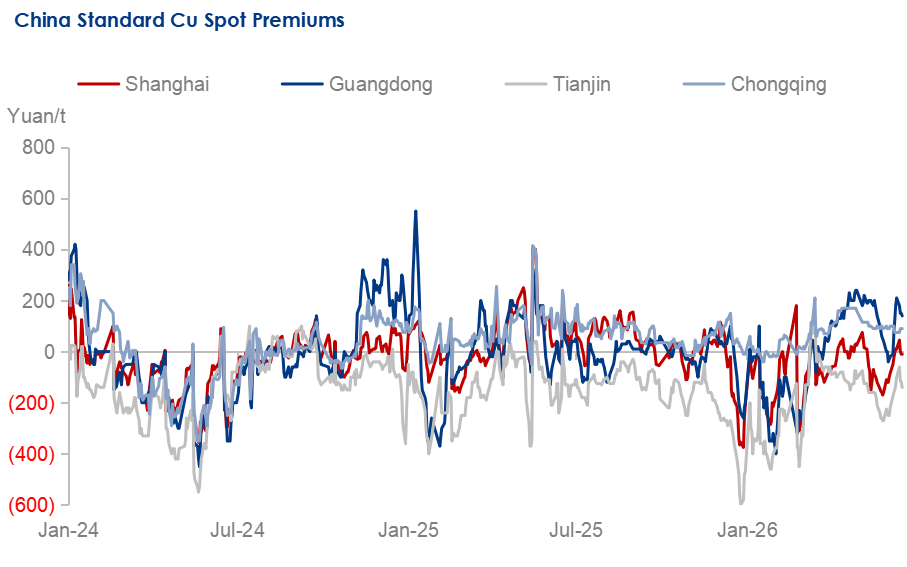

Premium: Falling refined copper inventory supports spot premium gains

China's refined copper prices shifted higher last week, and the spot premium rose initially before falling but still posted an overall increase. On one hand, the approaching Dragon Boat Festival holiday spurred some pre-holiday restocking demand at lower price levels. However, with copper prices fluctuating at elevated levels during the week, downstream users largely remained cautious, which led to a decline in spot trading volumes and weighed on the spot premium. On the other hand, although imported copper arrivals increased as the import ratio improved, domestic arrivals stayed low, keeping spot supply in China's refined copper market relatively tight. Overall, amid weak supply and demand, retail inventories of refined copper in China declined, lending support to the spot premium.

Looking ahead, as the half-year end approaches, some refined copper holders may seek to clear inventories to recover cash. Together with downstream companies' limited acceptance of current relatively high prices, holders are likely to lower spot premiums to facilitate transactions. Consequently, China's refined copper spot premium is expected to decline in the short term. According to Mysteel, refined copper spot premium ranges are forecast with Shanghai at -Yuan 50/tonne to Yuan 30/tonne, Guangdong at Yuan 80/tonne to Yuan 180/tonne, Tianjin at -Yuan 240/tonne to -Yuan 120/tonne, and Chongqing at -Yuan 50/tonne to Yuan 200/tonne this week.

Data Source: Mysteel

Supply: China refined copper spot supply sees limited improvement

The improvement in China's refined copper spot supply was limited last week. In Tianjin, spot supply tightened further due to futures deliveries, southbound shipments for warehouse warranting or long-term contract delivery, and maintenance at some regional smelters. Meanwhile, although some imported copper arrived in Shanghai as the import ratio improved, domestic arrivals remained low, capping the improvement in spot supply. In Guangdong and Chongqing, limited smelter shipments also kept supply relatively subdued. Overall, China's refined copper spot supply stayed tight.

Looking ahead, while refined copper imports are expected to edge higher with further improvement in the import ratio, smelter shipments will likely remain constrained by maintenance, suggesting that a meaningful supply improvement in the near term is unlikely.

Demand: China's refined copper market trading volume declines WoW

China's refined copper spot trading declined week on week last week. In Shanghai, persistently firm copper prices and spot premiums kept downstream purchasing sentiment cautious. Even ahead of the Dragon Boat Festival holiday, overall restocking volumes remained relatively limited. In Guangdong, holders stood firm on offers and were reluctant to sell amid tight spot supply, resulting in low downstream acceptance of high-priced material. The futures delivery during the week further dampened spot market activity. In Tianjin, undigested finished-product inventories and slowing new orders at downstream enterprises led to lackluster raw material procurement demand. Although some concentrated buying emerged when copper prices dipped, overall demand for refined copper remained weak. In Chongqing, downstream users accelerated long-term contract deliveries before the holiday, with spot transactions seeing some increase but lacking sustainability. Overall, spot trading activity in China's refined copper market was modest last week.

Looking ahead, with copper prices fluctuating at elevated levels and end-user order growth slowing, downstream demand is unlikely to improve significantly in the near term. Downstream enterprises will likely maintain a strategy of buying on dips.

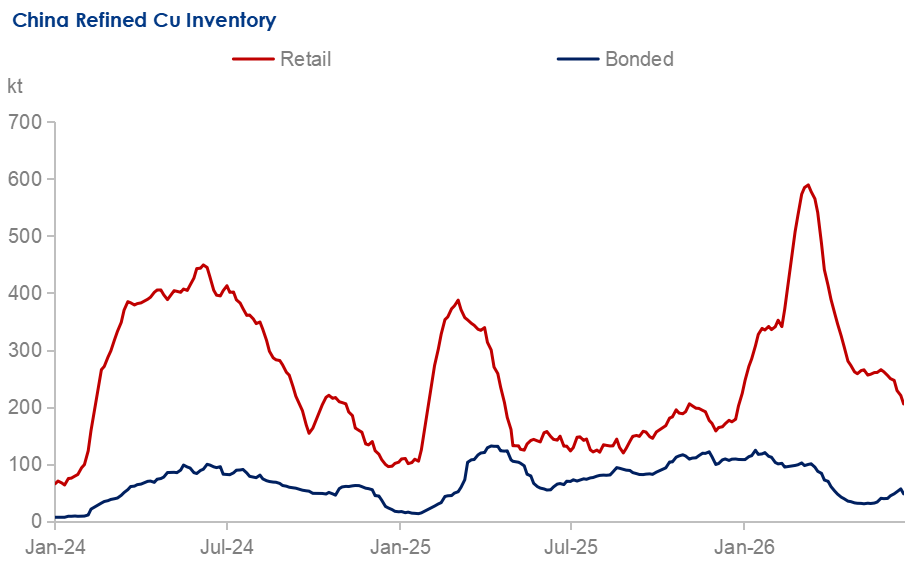

Inventory: China's refined copper retail and bonded inventories both decline

China's refined copper retail inventory declined last week. While imported copper arrivals increased, domestic smelter shipments remained relatively low, keeping overall inflows into retail warehouses limited. Meanwhile, some restocking demand ahead of the Dragon Boat Festival caused decent outflows from certain warehouses, leading to a week-on-week drop in overall retail inventory. Looking ahead to this week, with smelters still in the peak maintenance period, spot supply is unlikely to improve significantly, and retail inventory is expected to continue trending lower. However, given that downstream users remain reluctant to accept current copper prices, the pace of destocking is likely to moderate.

China's refined copper bonded inventory declined week on week last week. Although arrivals from imports and domestic smelters' material intended for export continued to flow into bonded zones, exports and customs clearance drew down the inventory. Looking ahead, some bonded warehouses are expected to continue shipping refined copper overseas, but with smelter shipments still arriving, the bonded inventory is forecast to edge down only slightly week on week.

The weekly average spread between the main COMEX and LME copper contracts was up by $257.03/tonne week on week to $651.56/tonne last week. The average LME cash-3M copper contract settlement spread was -$66.3/tonne last week, down by $28.5/tonne week on week. As COMEX copper traded at a premium, the COMEX-LME refined copper price spread widened further last week, driving an increase in COMEX copper inventory. In contrast, LME copper inventory fell. Looking ahead, as market expectations for the implementation of U.S. tariff policy draw closer, the COMEX copper premium is expected to persist in the near term, keeping its inventory on a modest upward trend. Meanwhile, LME inventory is forecast to continue decreasing.

Data Source: Mysteel

Written by Zhaorui Cui, cuizhaorui@mysteel.com

Edited by Mingyuan Wang, wangmingyuan@mysteel.com