Artificial Intelligence (AI) has become one of the most closely watched themes in the copper market, fueling expectations of a new wave of demand growth from data centers and related power infrastructure. Despite the attention surrounding such emerging industries, China's copper consumption remains overwhelmingly dependent on traditional sectors such as power grids, with the balance between evolving demand patterns and supply tightness expectations shaping copper price trends.

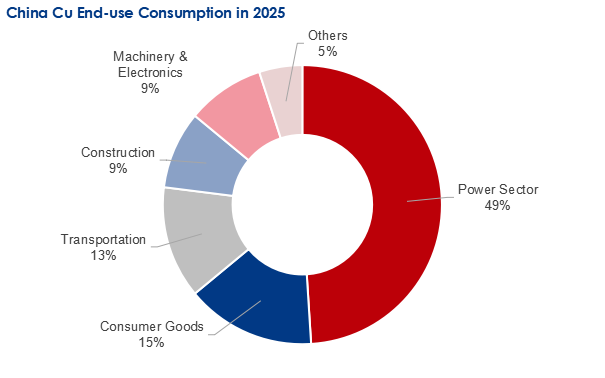

According to Mysteel, China's refined copper consumption reached 15.99 million tonnes in 2025, accounting for 57% of global demand. In terms of consumption structure, the power sector accounted for 49% of total, followed by consumer goods, including household appliances, at 15%, transportation at 13%, construction at 9%, and machinery and electronics at 9%.

Source: Mysteel

AI as strong future growth driver with high uncertainty

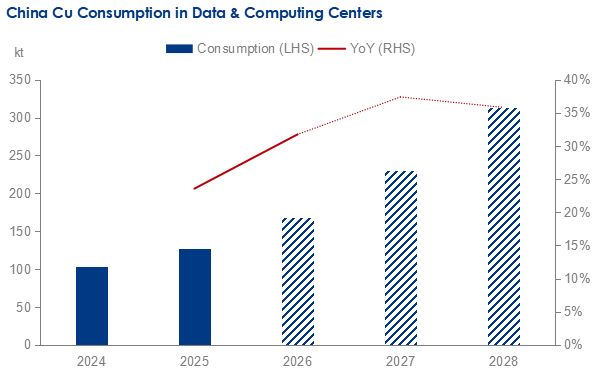

AI-driven expansion of data center capacity is creating a new source of copper demand through related power distribution systems, PCB circuitry, and liquid-cooling networks. Based on Mysteel's calculations, copper consumption from China's data centers and computing centers is estimated at 127,300 tonnes in 2025, representing year-on-year growth of 23.56%. Future growth is expected to be robust, implying a compound annual growth rate of 34.99% over 2026-2028. Meanwhile, due to the highly electricity-intensive AI development, additional investment may be required in power generation, transmission networks, substations, transformers, and grid modernization projects to support computing capacity, also boosting relevant copper consumption.

Source: Mysteel

Although AI-related demand is expected to become increasingly important, the sector still accounts for a relatively small share of total copper consumption. Moreover, factors including power supply constraints, project implementation, and technological evolution may limit the pace at which demand materializes. Consequently, AI is likely to exert a greater influence on copper market expectations and sentiment than on physical demand in the near term. The gap between projected demand growth and realized consumption will remain a key factor shaping future copper price performance.

Power grid remains the primary copper demand pillar

Despite growing attention on AI and other emerging industries, the power sector remains by far China's largest source of copper consumption, accounting for nearly half of total demand in 2025.

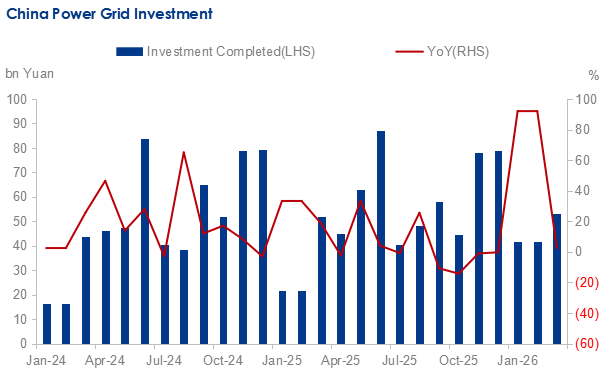

China's power grid investment reached Yuan 186.447 billion in January-April 2026, up 32.42% year on year, while investment in power engineering construction rose 16.88% year on year to Yuan 225.928 billion. Power grid investment has remained strong in 2026, with completed monthly investment in the first four months exceeding the levels recorded during the same period in recent years. This robust investment growth has provided solid support for China's copper consumption.

Source: Mysteel, NEA

Stable grid investment and rising electricity demand from Electric Vehicle (EV) charging infrastructure and data centers are expected to support continued copper consumption growth. According to data from China's National Energy Administration (NEA), electricity consumption in the EV charging and battery swapping services sector and the internet data services sector during January-April reached 51.3 billion kWh and 31.2 billion kWh, respectively, representing year-on-year growth of 55.9% and 44.4%. Looking ahead, the power and grid sector is expected to remain a key driver of China's copper consumption growth, providing a solid foundation for overall demand.

Long-term PV potential persists

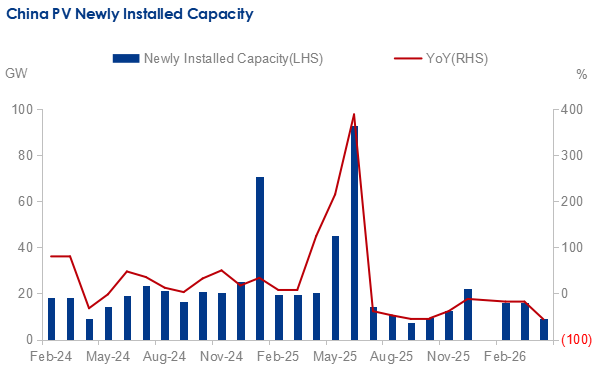

Among emerging copper end-use sectors, renewable energy has been one of the fastest-growing source of copper consumption. However, China's cumulative newly installed photovoltaic (PV) capacity declined sharply by 51.48% year on year to 50.91 GW from January to April 2026, according to NEA. Affected by electricity market reforms and the seasonal slowdown in the photovoltaic sector, weak end-user demand has weighed on installation activity recently.

Source: Mysteel, NEA

Looking ahead, weaker production schedules across the PV industry chain in June suggest that copper consumption from the sector is unlikely to increase significantly in the near term. Over the medium to long term, however, installation targets under China's ongoing energy transition remain intact, and the photovoltaic sector will continue to offer significant growth potential.

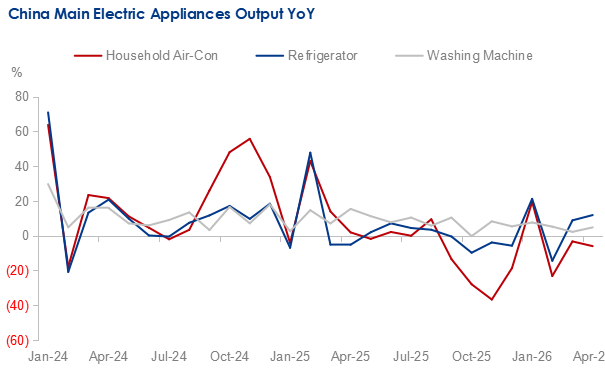

Weakening air conditioner consumption limits demand for copper

Beyond the power and energy sectors, household appliances represent another major source of copper consumption, particularly through the use of copper tubes, wires, and components in air conditioners, refrigerators, and washing machines. China's major home appliance market delivered mixed performance in April, with total output reaching 39.099 million units. Refrigerators and washing machines maintained year-on-year growth in production, while air conditioner output declined. As the largest segment among the three major white goods, the weakness in air conditioner production weighed on overall industry performance.

Source: Mysteel, ChinaIOL

Looking ahead to June 2026, total production schedules for air conditioners, refrigerators, and washing machines are set at 29.96 million units, marking a decrease of 13.71% over the actual output for the same period last year, according to ChinaIOL. Although the refrigerator and washing machine markets are still expected to achieve year-on-year growth, performance in the air conditioner market is likely to lag the level seen in the same period of 2025, due to earlier subsidy-driven demand releases, elevated inventories, and high raw material costs. The home appliance sector may remain a modest drag on copper demand growth.

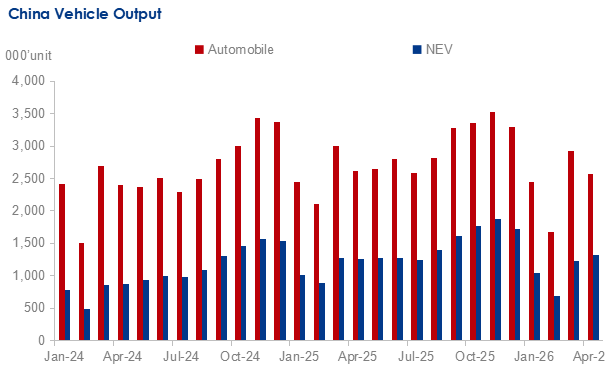

Demand from NEVs to see slowing growth

The structural shift toward vehicle electrification has boosted copper demand in recent years, as new energy vehicles (NEVs) require significantly more copper than conventional vehicles. However, demand growth from the automobile sector has slowed entering 2026, yet stayed generally supportive.

China's vehicle output increased by 1.60% month on month but decreased by 1.23% year on year to 2.629 million units in May 2026. Wherein, the output and sales of NEVs were 1.554 million and 1.496 million units in May 2026, with month-on-month increases of 17.73% and 11.31%, respectively, according to China Association of Automobile Manufacturers (CAAM).

Source: Mysteel, CAAM

In May, China's vehicle market remained weaker year on year, as part of the demand was brought forward following the strong stimulus measures implemented in 2025. Based on data from CAAM and Mysteel, China's automobile output saw year-on-year growth of 3.77% in 2024 and 10.32% in 2025, which is expected to slow in 2026. Looking ahead, a wave of new model launches and mid-year sales campaigns may support further limited month-on-month recoveries in production and sales. However, given the weaker policy environment and the relatively long replacement cycle of automobiles, a significant acceleration in domestic demand appears unlikely in the short term.

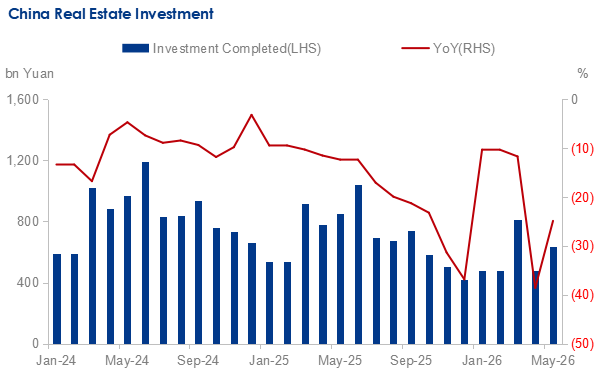

Downside risks ease in copper demand from real estate

The construction sector remains another key component of China's copper consumption, primarily through demand for electrical wiring, cables, air-conditioning systems, and building infrastructure. Although its share of total copper demand has declined over recent years, developments in the property market continue to influence overall consumption expectations.

China's real estate development investment totaled Yuan 2,396.9 billion from January to April 2026, a year-on-year decrease of 13.7%, according to the National Bureau of Statistics of China (NBS).

Source: Mysteel, NBS

Since the fourth quarter of 2025, China's policy support has helped stabilize housing transactions and prices in major cities, reducing downside risks to copper demand. Looking ahead, the housing market is expected to remain supported primarily by rigid demand and activity in the existing home market, while demand for upgraded housing will likely require further policy support. The sector will remain in transition and is unlikely to become a significant source of copper demand growth in the near term.

Summary

Taken together, China's traditional copper-consuming sectors continue to provide major demand support, although growth momentum has become increasingly uneven across industries. Meanwhile, emerging sectors such as AI data centers are beginning to create new demand expectations, despite a relatively low base and high uncertainties going forward.

Amid expected AI-driven development, power sector expansion, and continued investment in clean energy infrastructure, underlying copper demand in China is expected to remain well supported, providing a solid floor for copper prices. Looking ahead, the balance between resilient traditional demand and the expansion of new consumption drivers will be a key determinant of China's copper consumption growth and the sustainability of copper price support from the demand side.

Written by Mingyuan Wang, wangmingyuan@mysteel.com

Edited by Zhaorui Cui, cuizhaorui@mysteel.com