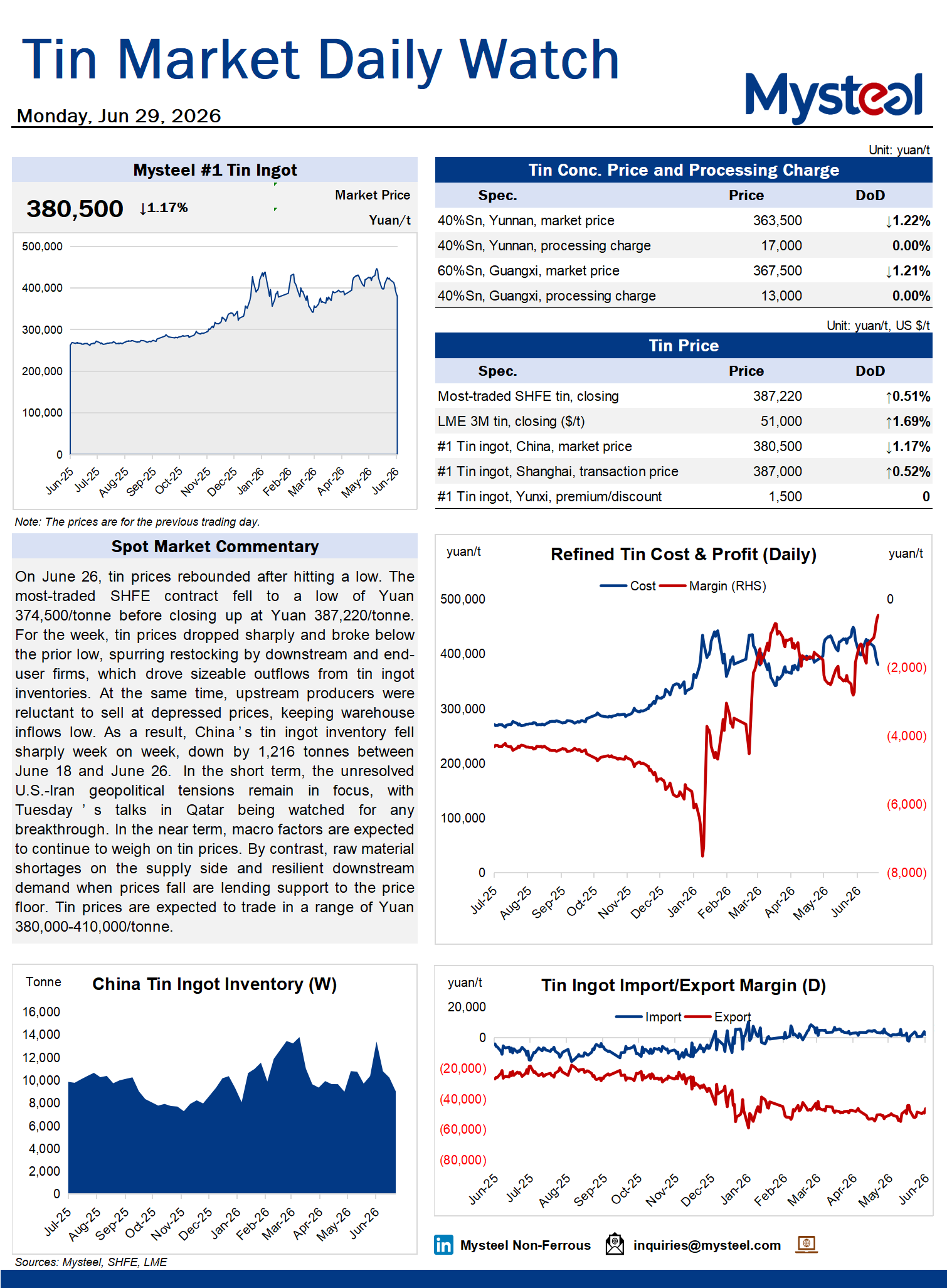

On June 26, tin prices rebounded after hitting a low. The most-traded SHFE contract fell to a low of Yuan 374,500/tonne before closing up at Yuan 387,220/tonne. For the week, tin prices dropped sharply and broke below the prior low, spurring restocking by downstream and end-user firms, which drove sizeable outflows from tin ingot inventories. At the same time, upstream producers were reluctant to sell at depressed prices, keeping warehouse inflows low. As a result, China's tin ingot inventory fell sharply week on week, down by 1,216 tonnes between June 18 and June 26. In the short term, the unresolved U.S.-Iran geopolitical tensions remain in focus, with Tuesday's talks in Qatar being watched for any breakthrough. In the near term, macro factors are expected to continue to weigh on tin prices. By contrast, raw material shortages on the supply side and resilient downstream demand when prices fall are lending support to the price floor. Tin prices are expected to trade in a range of Yuan 380,000-410,000/tonne.