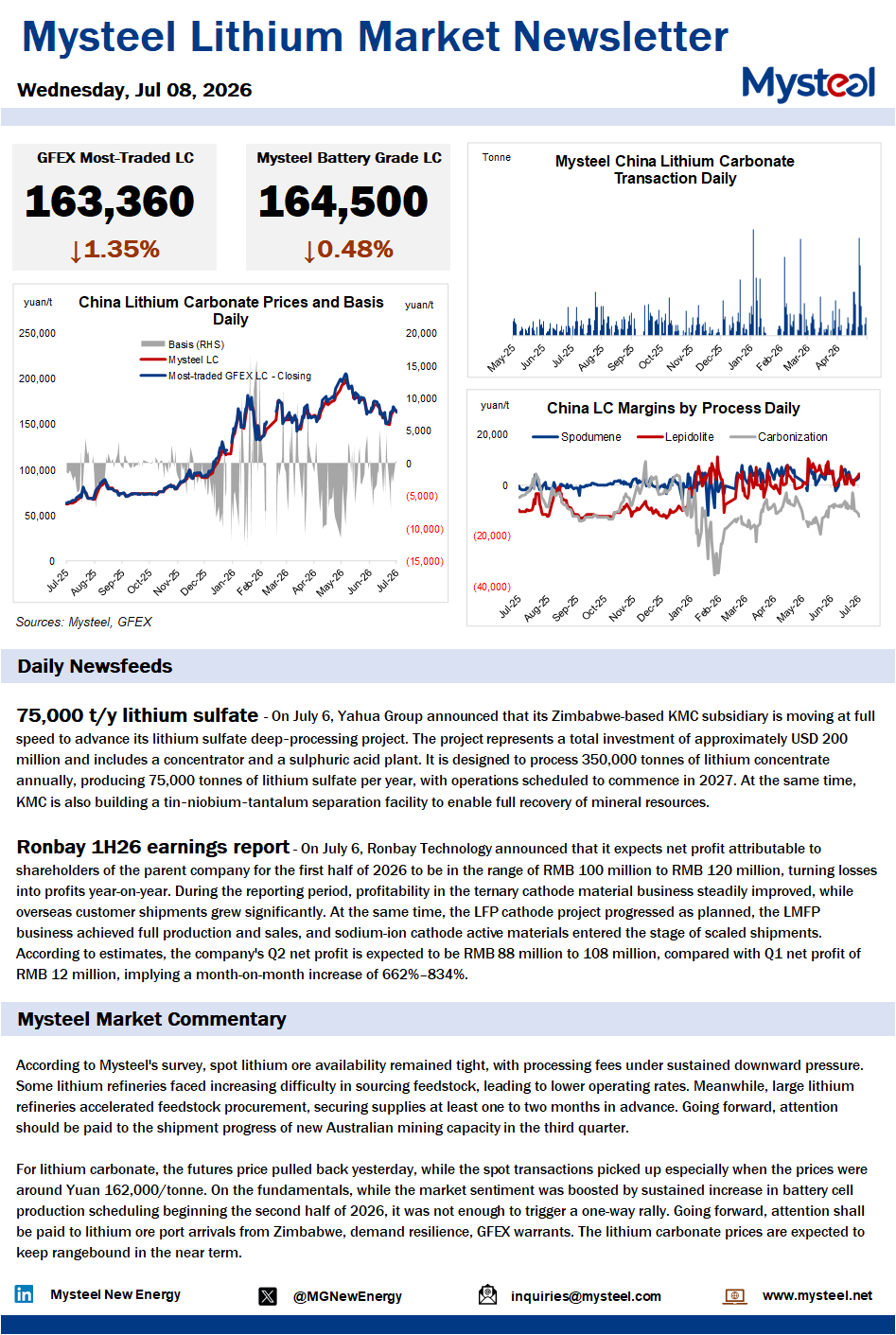

According to Mysteel's survey, spot lithium ore availability remained tight, with processing fees under sustained downward pressure. Some lithium refineries faced increasing difficulty in sourcing feedstock, leading to lower operating rates. Meanwhile, large lithium refineries accelerated feedstock procurement, securing supplies at least one to two months in advance. Going forward, attention should be paid to the shipment progress of new Australian mining capacity in the third quarter.

For lithium carbonate, the futures price pulled back yesterday, while the spot transactions picked up especially when the prices were around Yuan 162,000/tonne. On the fundamentals, while the market sentiment was boosted by sustained increase in battery cell production scheduling beginning the second half of 2026, it was not enough to trigger a one-way rally. Going forward, attention shall be paid to lithium ore port arrivals from Zimbabwe, demand resilience, GFEX warrants. The lithium carbonate prices are expected to keep rangebound in the near term.