The Shanghai Futures Exchange's (SHFE) warehouse warrants for copper futures rose by 1,828 tonnes to 5,750 tonnes on December 28, leading to a week-on-week decrease of 3,087 tonnes or 34.93%, and an increase of 2,994 tonnes or 108.64% month on month.

SHFE copper price rose to about Yuan 69,400/tonne today, while premiums of refined copper in East China rose by Yuan 175/tonne.

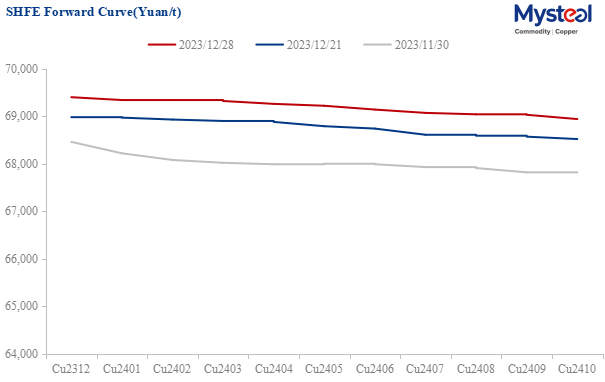

The yield of US treasury bonds and the US dollar index continued to fall, while US stocks have further risen, driving LME copper prices to a new high since August. SHFE copper prices have been relatively weak due to factors such as exchange rates, but have also risen to the top of the current fluctuation range close to Yuan 70,000/tonne.

According to surveys by several regional reserve banks in the US, employers generally expect to reduce recruitment in 2024, mainly because Federal Reserve measures aimed at curbing inflation are dragging down the economy.

Several Chinese banks have successively lowered deposit interest rates. The 800 billion Yuan treasury bond project issued by the Ministry of Finance is expected to be implemented in early 2024, forming stronger support for the economy.

Maersk and CMA-CGM announced that they will gradually resume Red Sea shipping routes, indicating that the current shipping tension is expected to be eased. After this news was released, crude oil prices fell back. The upward momentum of non-ferrous metals has also weakened as a result.

The China Smelters Purchase Team (CSPT) has set the treatment and refining charges (TC/RCs) for copper concentrate processing in the first quarter of 2024 to be $80/dmt and 8 cents/pound, significantly lower than the $95/dmt and 9.5 cents/pound in the fourth quarter of 2023, reflecting the short expectation of copper concentrate supply.

According to Mysteel's survey, China's refined copper inventory increased by 6,400 tonnes to 64,900 tonnes week on week this week. The main reason is that downstream enterprise demand weakens at the end of the year and in the face of high copper prices, while import copper customs clearance volume increases.

The supply of domestic copper smelters is expected to remain stable in January, while downstream enterprise production is being dragged down by factors such as holidays and environmental pollution. The fundamental support for copper prices in China is insufficient in the short term.

Overall, the optimistic expectations of both overseas and domestic macroeconomics still support copper prices in the short term. However, from a historical perspective, current economic data indicates that the economic cycle is in an early recession, so copper prices have a high probability of facing a significant decline in 2024. Meanwhile, China's economic resilience will support overall demand and enhance the bottom of copper prices.

Data Source: SHFE

Data Source: SHFE

Written by Edenlis Huang, huangting@mysteel.com

Edited by Paula Xu, xuzhongping@mysteel.com