The Shanghai Futures Exchange's (SHFE) warehouse warrants for copper futures fell by 249 tonnes to 4,058 tonnes on January 3, leading to a week-on-week increase of 136 tonnes or 3.47%, and an increase of 888 tonnes or 28.01% month on month.

SHFE copper price fell to about Yuan 68,700/tonne today, while premiums of refined copper in East China fell by Yuan 100/tonne.

In December, the Federal Reserve's view on monetary policy suddenly shifted to such dovish, resulting in a concentration of investor optimism. However, the sudden shift was more likely to reflect the failure of the Federal Reserve's expectation management and the dire economic situation.

The US dollar index rebounded to above 102 after optimistic expectations of interest rate cuts waned. The Federal Reserve will release the minutes of its December interest rate meeting later today. Most analysts believe that the Federal Reserve will suppress the overly optimistic expectations in the current market that interest rates will be lowered by as much as 175 basis points in 2024.

According to investment bank Robert A. Stanger & Co., in January-November 2023, the size of non-public traded Real Estate Investment Trusts (REITs) in the US reached $17.4 billion, far exceeding the $12 billion for 2022. It is expected that the data will further rise in 2024, indicating that the US commercial real estate is experiencing its most severe recession since World War II.

The Manufacturing Purchasing Managers' Index (PMI) of the Eurozone in December was 44.4, marking the 18th consecutive month of contraction. This means that the GDP of the Eurozone in the fourth quarter is unlikely to improve, signaling a recession.

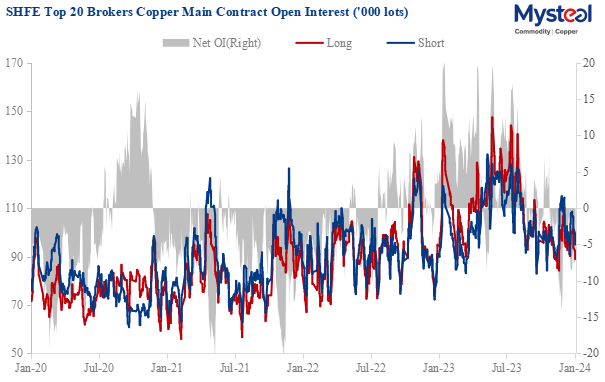

SHFE copper futures positions have not significantly increased during the recent uptrend, but have begun to decline during this week, indicating a bearish sentiment and willingness to settle among the bulls. As macroeconomic risks gradually emerge, investors' optimistic expectations of interest rate cuts will gradually be replaced by a weak economic reality.

The Red Sea shipping routes are still being hindered by geopolitical crises, leading to soaring shipping costs from Europe, partially supporting domestic copper prices, which is reflected in the significant narrowing of the import price ratio loss.

After the current off-season of copper consumption has passed, the main support for copper prices will be a tightening of the supply side. According to Mysteel's survey, it is expected that global copper supply will be reduced by 500,000 tonnes in 2024 due to the shutdown of overseas mines, but its impact will manifest in the long run.

Overall, copper prices, and even most non-ferrous metal prices, are expected to fall in the short term after sustained increases boosted by macroeconomic factors. From a historical perspective, current economic data indicates that the economic cycle is in an early recession, so copper prices face a higher probability of a sharp decline in 2024, followed by a gradual rebound due to supply shortages. Meanwhile, China's economic resilience will support overall demand and enhance the bottom of copper prices.

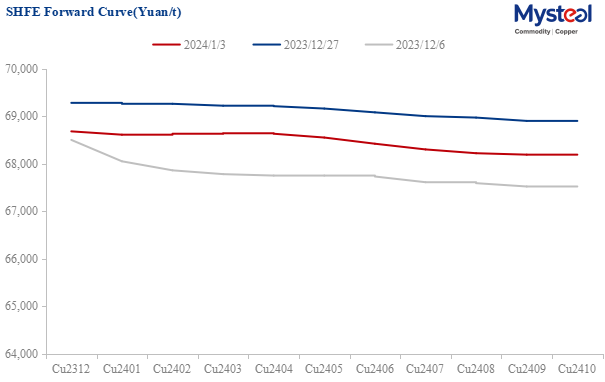

Data Source: SHFE

Data Source: SHFE

Written by Edenlis Huang, huangting@mysteel.com

Edited by Paula Xu, xuzhongping@mysteel.com