The Shanghai Futures Exchange's (SHFE) warehouse warrants for copper futures fell by 599 tonnes to 3,459 tonnes on January 4, leading to a week-on-week decrease of 2,291 tonnes or 39.84%, and an increase of 289 tonnes or 9.12% month on month.

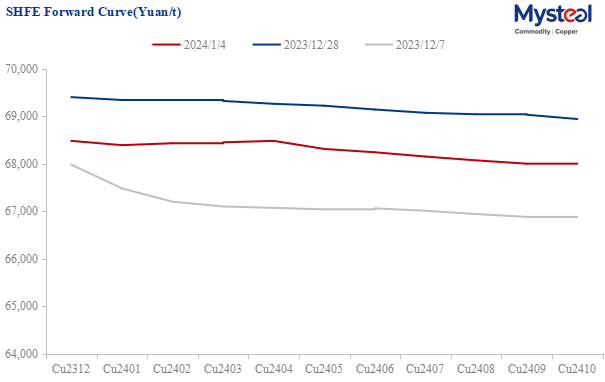

SHFE copper price fell to about Yuan 68,500/tonne today, while premiums of refined copper in East China fell by Yuan 15/tonne.

According to the minutes of the Federal Reserve's December interest rate meeting released yesterday, although the interest rate hike cycle has ended, the timing and path of interest rate cuts remain highly uncertain. Some decision-makers believe that long-term high interest rates will accelerate macroeconomic recession and a tighter labor market. Other officials believe that if inflation remains far above the target of 2%, high interest rates will need to be maintained longer than expected. As the market has overly optimistic expectations of interest rate cuts, commodity prices are under selling pressure in the short term.

According to the Job Openings and Labor Turnover Survey (JOLTS), the number of job vacancies in the US decreased to 8.79 million in November, a two-year low. The voluntary turnover rate has hit a new low in over three years. Tightness in the labor market means an increase in financial pressure on residents, which will lead to a wage-price spiral and greater cost pressure on businesses.

Coupled with the ongoing geopolitical crisis, high commodity prices, especially energy prices, will undoubtedly lead to stagflation of macroeconomic prospects. This is also one of the reasons why copper prices have always fallen sharply in every past interest rate reduction cycle.

According to Mysteel's survey, China's imported copper concentrate TC further plummeted to $54.5/dmt on January 3. The main reason was that the supply shortage caused by various factors is continuing to intensify. The impact of supply shortages caused by the shutdown of overseas copper mines and geopolitical crises on import supply is gradually emerging.

However, owing to the current off-season of copper consumption in China and the continued sluggish demand in real estate and related industries, the supply of refined copper in China remains loose. The continuous contraction of overseas manufacturing will also discount the overall demand for copper in 2024. However, it is expected that China's demand for copper in the fields of new energy and infrastructure will maintain a relatively high growth rate in 2024.

Overall, copper prices, and even most non-ferrous metal prices, are expected to fall in the short term after sustained increases boosted by macroeconomic factors. From a historical perspective, current economic data indicates that the economic cycle is in an early recession, so copper prices face a higher probability of a sharp decline in 2024, followed by a gradual rebound due to supply shortages. Meanwhile, China's economic resilience will support overall demand and enhance the bottom of copper prices.

Data Source: SHFE

Data Source: SHFE

Written by Edenlis Huang, huangting@mysteel.com

Edited by Paula Xu, xuzhongping@mysteel.com