Key Highlights:

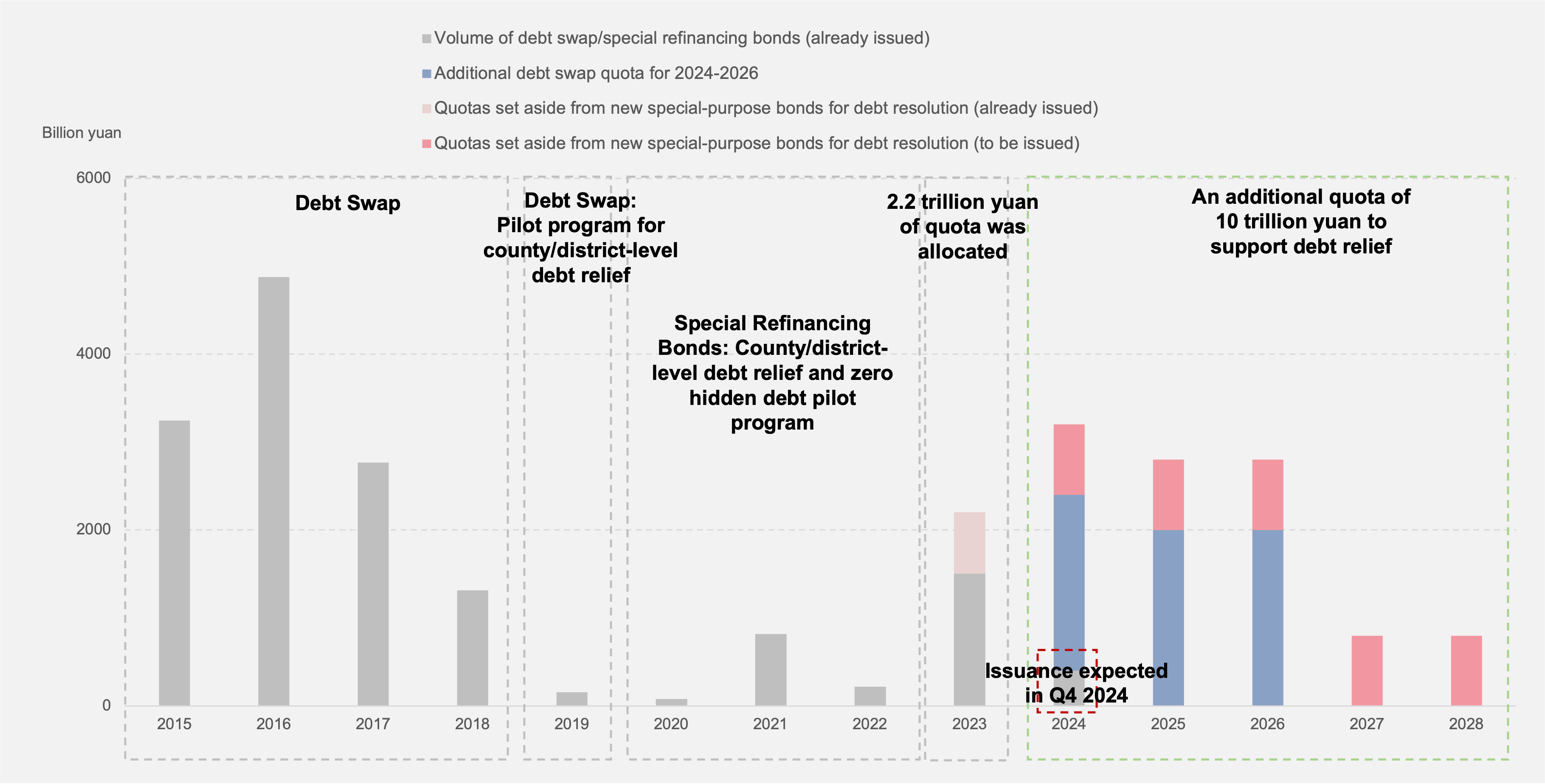

- From 2024 to 2028, China will allocate 10 trillion yuan towards debt relief resources to replace hidden debts, while maintaining its current fiscal deficit levels. This initiative marks the government's most significant effort in recent years to address its debt challenges.

- From 2024 to 2026, a total of 6 trillion yuan of implicit debt will be resolved by raising the ceiling for special local government debt (already approved by the NPC Standing Committee).

- From 2024 to 2028, China will set aside 800 billion yuan from each year's new special-purpose bonds for local governments to swap 4 trillion yuan of implicit debts.

Why Not Allocate the Funds for Direct Investment?

- China's substantial implicit debt levels have constrained local governments' fiscal spending. In the first three quarters of 2024, China' interest expenditure on local government debts surpassed 1 trillion yuan, accounting for 11% of local governments' general public budget revenue.

- Domestic hidden debts are primarily concentrated in urban infrastructure and public service sectors, placing significant debt pressure and elevating credit risks for urban construction investment firms. While direct investment stimulation can ensure capital flow, it typically focuses on specific projects and doesn't fundamentally address the underlying debt and cash flow challenges these firms encounter. In contrast, debt relief policies provide a more comprehensive solution, effectively tackling these financial issues at their core.

Impact:

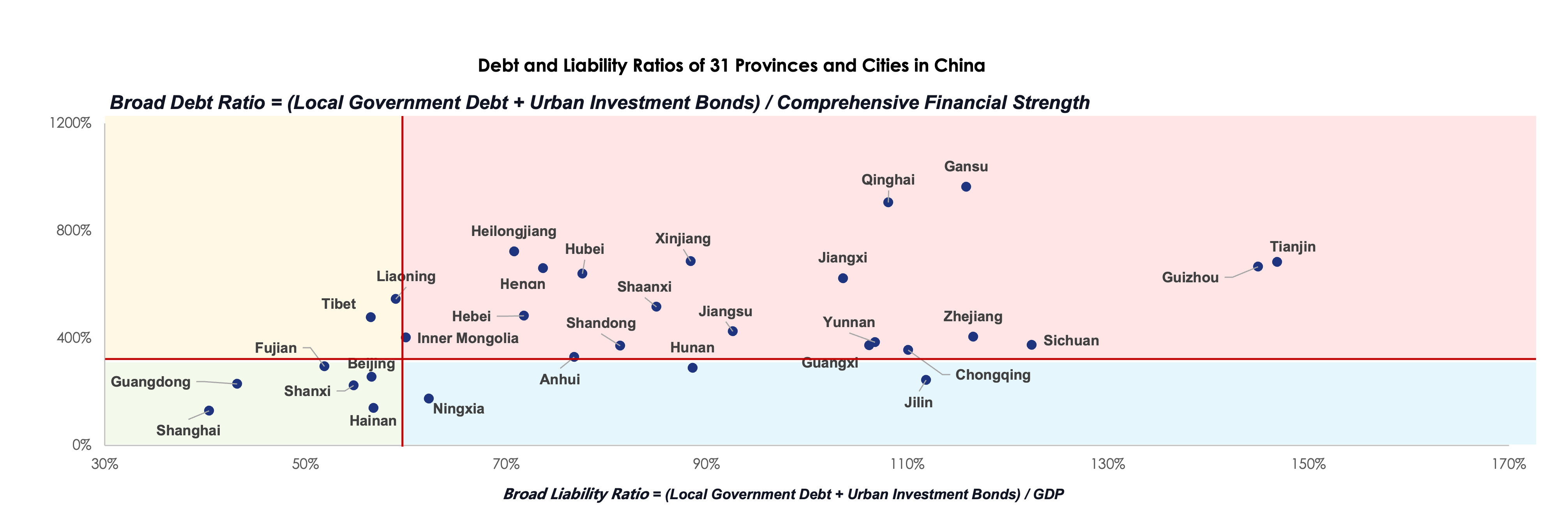

- On Local Governments: The allocation plan for debt restructuring has yet to be finalized, but the current round of debt relief efforts aims to alleviate local debt repayment pressures and create room for development. Provinces with heavier debt burdens or greater development potential are likely to receive more quotas for special-purpose bonds. Central, western, and northeastern regions are likely to gain more resources.

- On Investment: By reducing the annual debt repayment obligations of local governments, an estimated 600 billion yuan in interest payments will be saved over five years, freeing up funds to support economic development. With the industrial backup in the western regions and industrial upgrades in the northeast, there is a significant demand for investment in emerging industries, as well as transportation and logistics infrastructure. Once debt pressures ease, local fiscal investments are likely to focus more on these areas.

- Taking Sichuan as an example, in April 2024, the province released a list of 330 major projects, with a plan to accelerate their initiation within 2-3 years. Infrastructure projects account for nearly 40% of the total, primarily focusing on transportation, energy, and water conservancy, with a total investment of 1.3 trillion yuan. Industrial projects make up about 50%, with an estimated total investment of 781.12 billion yuan.

- The construction of these projects is expected to drive transportation demand, benefiting diesel consumption. Since the beginning of 2024, domestic diesel demand has decreased by 6.9% year-on-year due to energy substitution and slow progress in infrastructure projects, struggling to return to 2021 levels. The economic downturn pressure is likely to persist into 2025, keeping diesel demand on a downward trend. However, considering the declining oil prices, improved cost-effectiveness of diesel, and the positive impact of debt restructuring on local investment, the rate of decline in diesel demand is expected to narrow to 5.6% in 2025.

Source: The Ministry of Finance, China Electronic Local Government Bond Market Access, GL Consulting

Source: Enterprise Early Warning System, GL Consulting

Note: The debt ratio warning line is 300%, while the liability ratio warning line is 60%.

The above content is the major conclusions and highlights extracted from China (Energy Transition) Policy Perspective, a monthly report that focuses on the evolution of China's energy transition through deep analysis into China's volatile yet policy-driven energy market. Click to request for a full version.