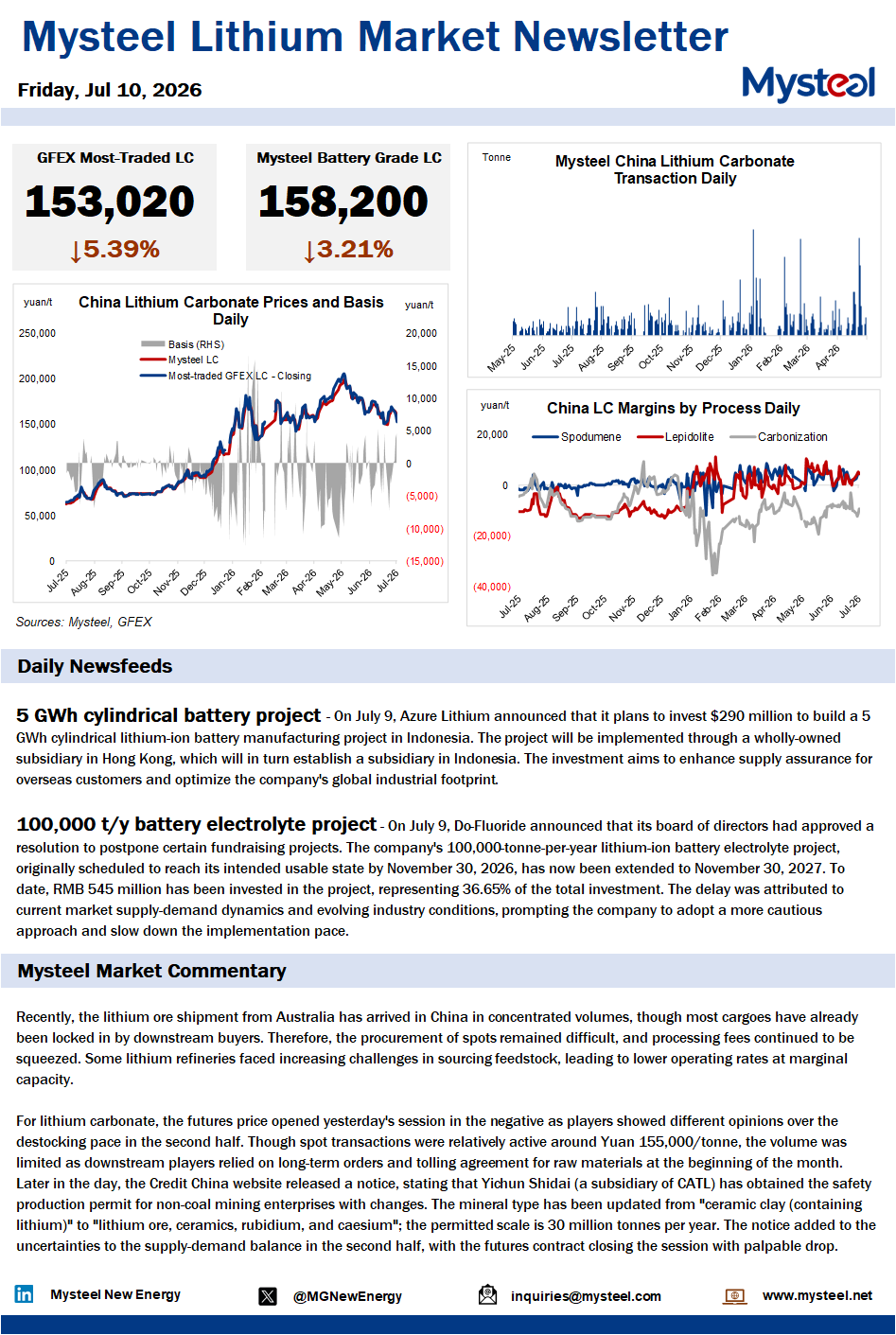

Recently, the lithium ore shipment from Australia has arrived in China in concentrated volumes, though most cargoes have already been locked in by downstream buyers. Therefore, the procurement of spots remained difficult, and processing fees continued to be squeezed. Some lithium refineries faced increasing challenges in sourcing feedstock, leading to lower operating rates at marginal capacity.

For lithium carbonate, the futures price opened yesterday's session in the negative as players showed different opinions over the destocking pace in the second half. Though spot transactions were relatively active around Yuan 155,000/tonne, the volume was limited as downstream players relied on long-term orders and tolling agreement for raw materials at the beginning of the month. Later in the day, the Credit China website released a notice, stating that Yichun Shidai (a subsidiary of CATL) has obtained the safety production permit for non-coal mining enterprises with changes. The mineral type has been updated from "ceramic clay (containing lithium)" to "lithium ore, ceramics, rubidium, and caesium"; the permitted scale is 30 million tonnes per year. The notice added to the uncertainties to the supply-demand balance in the second half, with the futures contract closing the session with palpable drop.