On September 27, SHFE Copper futures warehouse receipt was 4,330 tonnes, 474 tonnes less than the previous trading day; the cumulative decrease in the past week was 4,219 tonnes, a decrease of 49.35%; the cumulative decline in the past month was 324 tonnes, a decrease of 6.96%.

The Fed is expected to raise interest rates by more than 100 basis points in the last time this year, which keeps the US dollar strong. Central banks around the world have sharply raised interest rates since the Fed's decision released, reflecting rising concerns about a recession in the market. The preliminary eurozone PMI for manufacturing services hit a new low in nearly one year in September, which widens expectations of a recession in Europe. US jobless claims rebounded slightly, which shows that labor demand remains supportive despite the grim economic outlook.

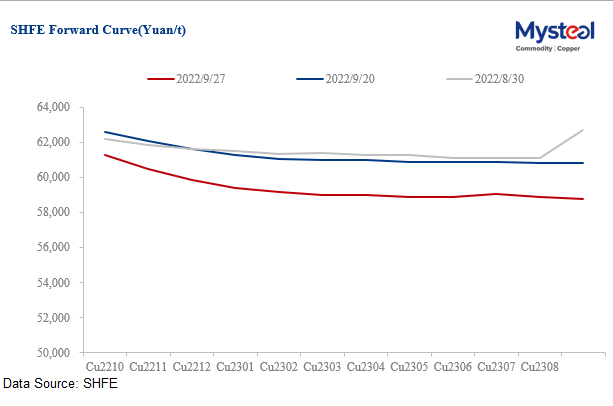

LME copper inventories increase 22,725 tonnes this week. SHFE copper inventories increases 1,032 tonnes. LME inventories climbs to a high in nearly a month. China spot inventories remains low, and the premiums maintains high, which means copper prices are still supported. Overseas miners' strike crisis has not been lifted, and Colombia announced a tightening of mineral environmental requirements.

Overall, the fundamentals are still supported, but the macro pressure increases, copper prices are expected to enter the downward trend in advance.

The current copper price drop range is larger, and the market sentiment is pessimistic. It is recommended to appropriately reduce the short positions. In view of the medium and long term is still in the recession cycle, it is recommended to short at every high point. Avoid too much long positions and pay more attention to risk control.

For queries and more information/data/reports access, please contact Paula Xu at xuzhongping@mysteel.com